The long-awaited inflection point in US digital wallet adoption may finally be upon us. This finding is among the key takeaways of McKinsey’s most recent Digital Payments Consumer Survey, an annual study of US consumers conducted since 2015.

Other survey insights challenge the conventional wisdom surrounding digital payments behavior, and point to unexpected shifts in segmentation that financial services providers—both traditional and non-traditional—are already acting upon. In this article we share some of the key insights as well as the implications for financial services providers of all stripes.

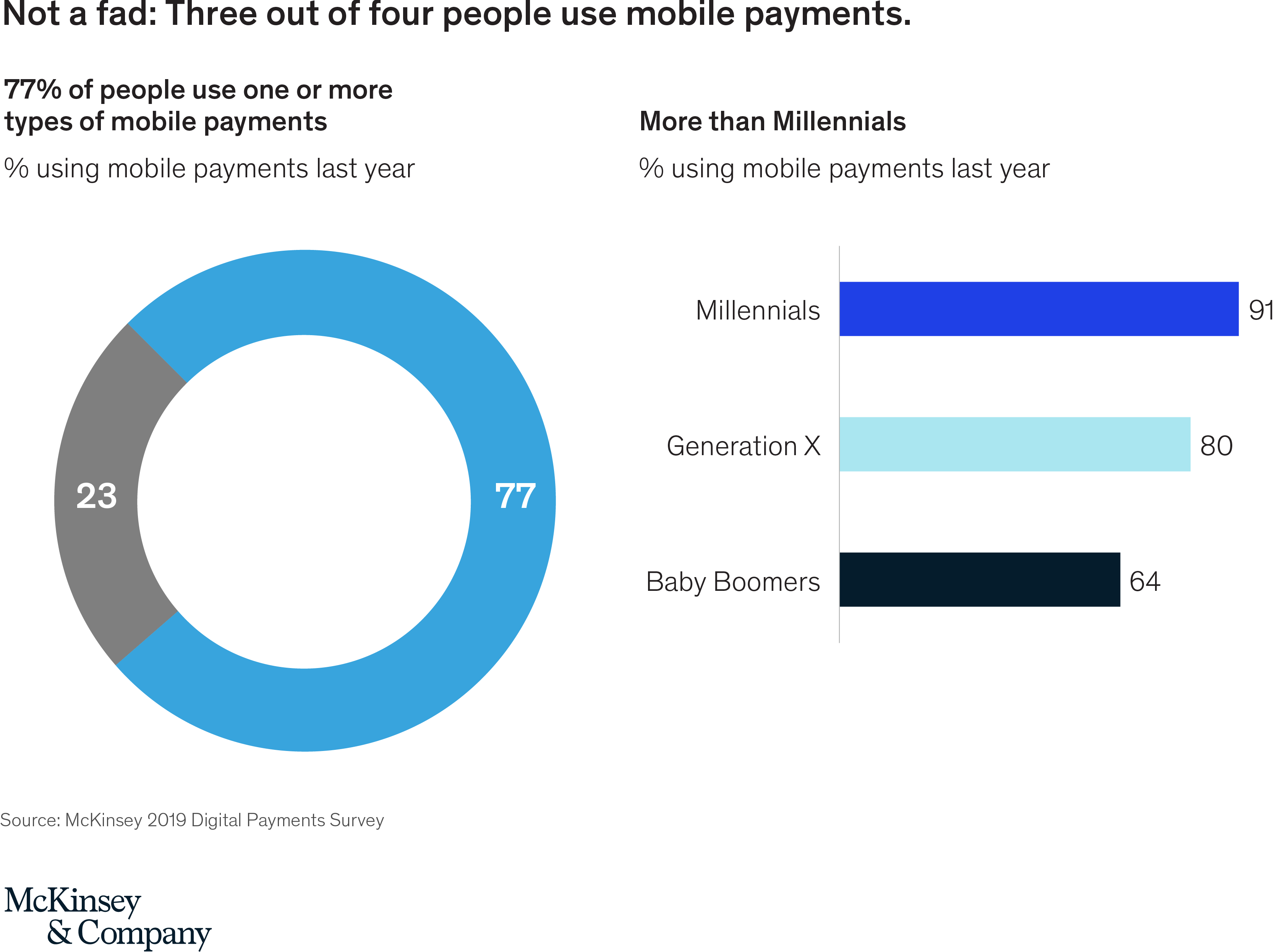

McKinsey’s research reveals that over three-quarters of US consumers made a mobile payment of some type (whether online, in store, or in-app) in the twelve months ending August 2019 (Exhibit 1). The most meaningful increase is in the use of digital wallets, which are defined here as an app or solution that can be used to store card or bank information to make purchases, pay for services, or make online payments to family or friends—that is, peer-to-peer (P2P). Close to half of consumers are now using in-app digital wallets, a 7 percent uptick from one year earlier. In-store usage remains lighter, however (around one-fifth of respondents).

Another critical takeaway from the survey is that digital behavior is not confined to the Millennial cohort most commonly associated with digital transactions. Although Millennials do lead the way, all groups show significant uptake—including 64 percent of Baby Boomers participating in mobile payments in some form.

A top-of-wallet paradigm shift

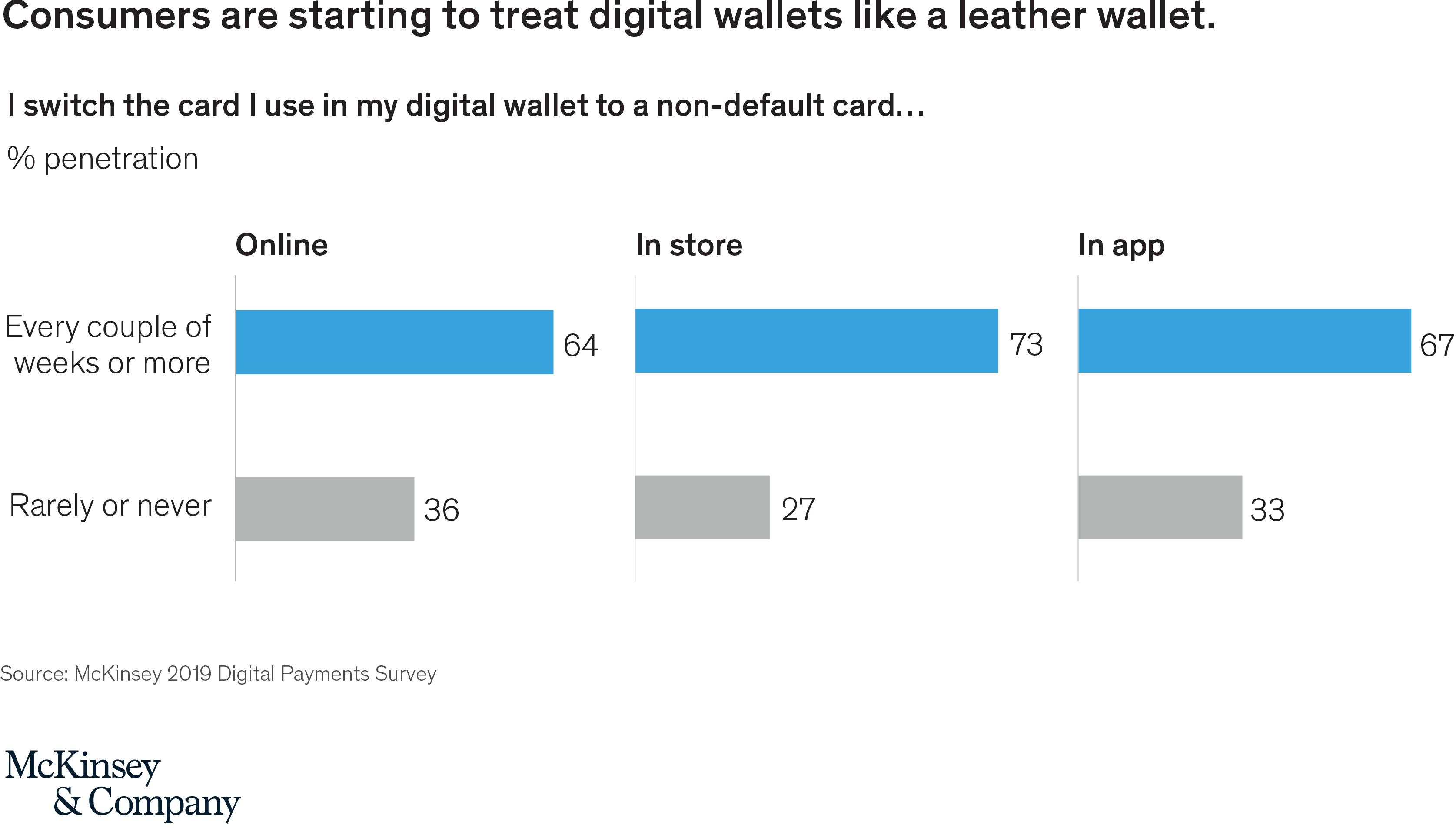

One significant surprise is that consumers are beginning to treat digital wallets more like their legacy analogs. The inception of these digital credential containers was thought to exacerbate the “top of wallet” paradigm that long governed payments card preference. Major issuers have engaged in a “land rush,” striving to establish their card credentials as the default payments option in a variety of apps—witness American Express offering $200 in annual Uber credits to its Platinum cardholders, and Citibank and others touting statement credits for users using their card to settle recurring charges with iTunes, Netflix, and others.

The prevailing wisdom has been that most consumers would take a “set it and forget it” approach, making top-of-wallet status in the digital world far stickier and more lucrative than in the physical setting. This tide has shifted, however; a majority of in-store and in-app wallet users now report switching to a non-default card at least every couple of weeks (Exhibit 2). This may be attributable to added functionality from segment leaders like Amazon and ride-sharing companies simplifying the process of toggling between cards.

Four distinct segments, three digital plays

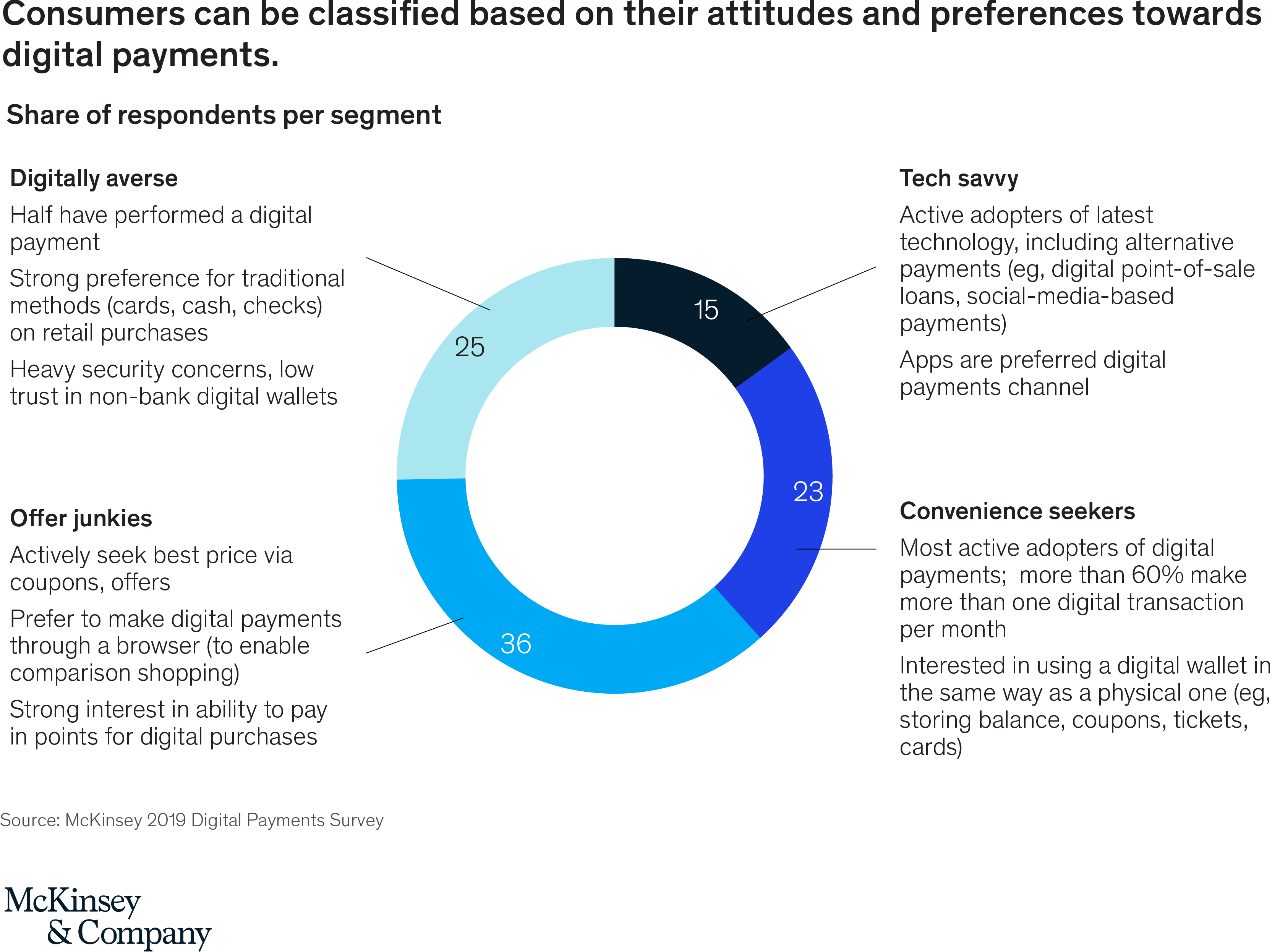

Behavior also varies across segments defined by factors other than age as well (Exhibit 3). Our 2018 research identified four basic archetypes: The digitally averse cohort comprises a quarter of the US adult population. Only half of this group has so much as completed a digital payment, and until their trust/channel security hurdles can be overcome, they are unlikely to migrate from traditional payments methods. Two groups—tech savvy and offer junkies—represent a combined half of shoppers and are certainly candidates for the type of card-toggling described above. Notably, however, offer junkies prefer to shop via browser rather than in-app, in order to facilitate deal comparisons—giving rise to market solutions like Rakuten (Ebates) and Wikibuy.

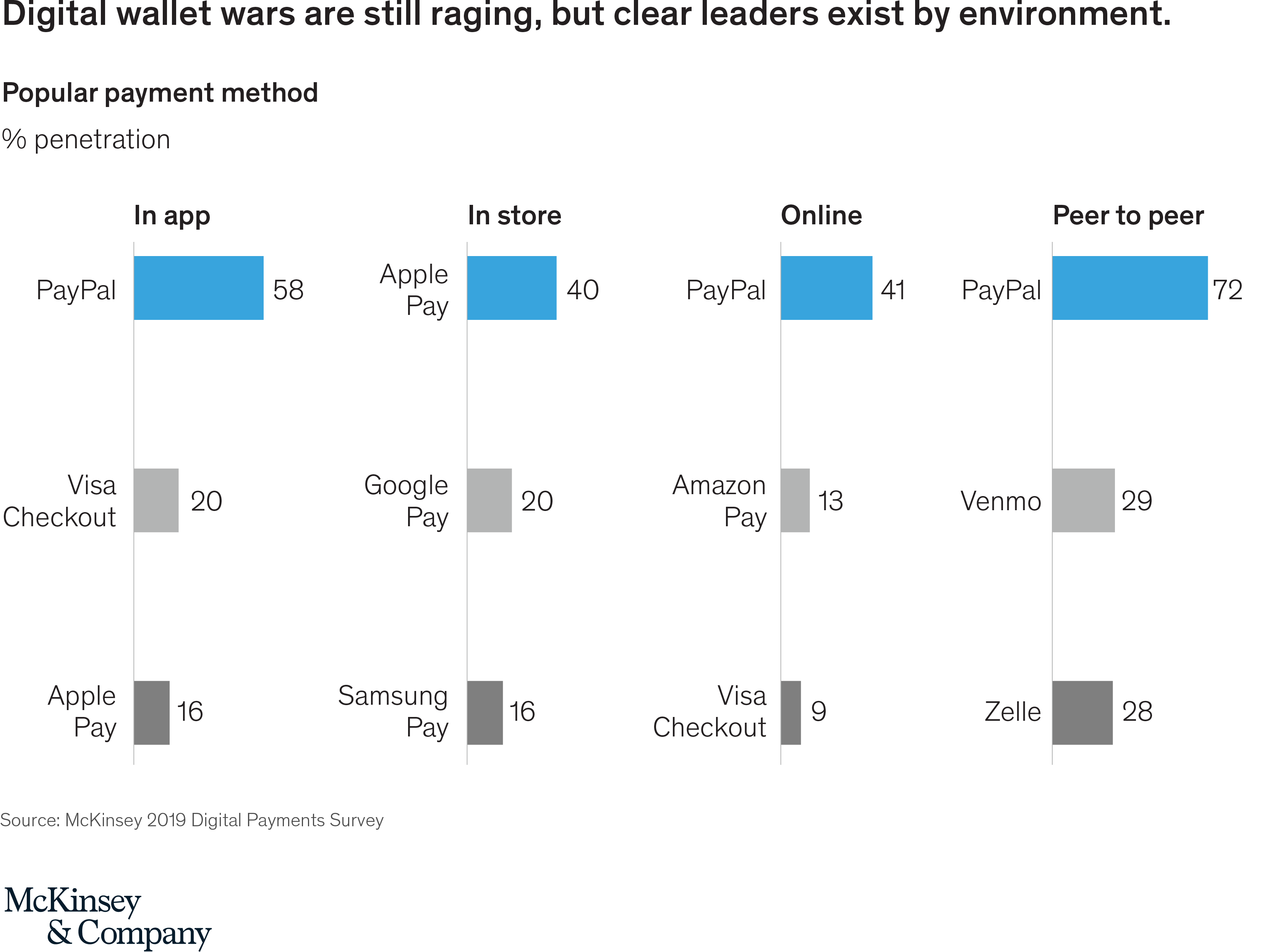

Convenience seekers, the final group, comprise the strongest digital adopters to date—surprisingly even more so than the tech savvy group. Consistent with its name, this group also shows the greatest interest in embracing features beyond payments that mirror those of physical wallets—storage of coupons and tickets, for instance. They also show willingness to toggle between cards to realize those benefits; two-thirds of this group regularly makes payments with a non-default card. Even among the leading digital wallet players, consumer preferences vary markedly by use case, implying that users are not averse to maintaining multiple wallets, at least at this stage of market evolution (Exhibit 4). Early mover PayPal holds a leading share for in-app and online purchases whereas Apple Pay, an early mover for in-store purchases, in the channel, enjoys a wide advantage in that channel.

The rapidly evolving P2P space is even more complex. Although PayPal again holds a lead, the gap to number-two player Venmo is narrower. Venmo is a subsidiary of PayPal, reinforcing the notion that variations on functionality and branding appeal to different segments. Close behind is Zelle, the fast-growing bank-owned alternative which is riding the network effect of its large-financial institution reach as well as a stated preference across all cohorts for banks as the provider of digital wallet services.

Zelle’s significantly higher average transaction size is again a sign of a markedly different core user or use case. Both Zelle and Venmo have also moved beyond P2P. Zelle offers business-to-consumer (B2C) payments, such as rebates, rewards, or other disbursements. Venmo is now available as a consumer-to-business (C2B) payments method on millions of websites through PayPal. This could mirror the experience of MobilePay in the Nordics, which began as a P2P solution before gaining traction as a more all-purpose wallet.

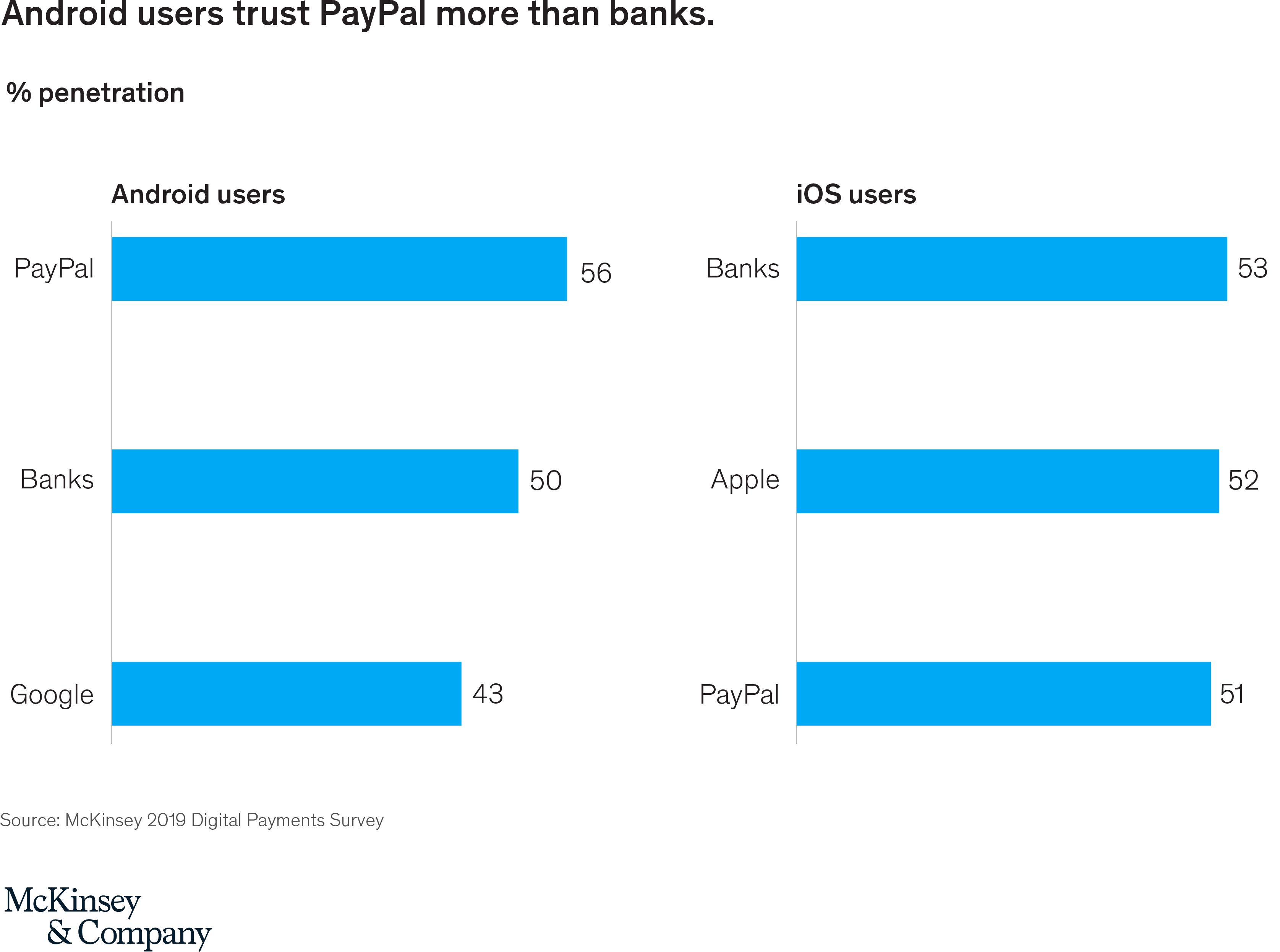

The handset as segmentation device

Another interesting attitudinal disparity exists between users of iOS and Android handsets. iOS users indicate a similar level of trust in Apple than in financial institutions (Exhibit 5). This is perhaps unsurprising given the intense brand loyalty Apple enjoys. It is nonetheless an important factor to consider given the long-discussed notion of a non-bank entering the US payments equation in a customer-facing role.

The majority of US smartphones are Android-based, however. Among these users, PayPal is the most trusted entity for financial services in 2019, surpassing banks as the top choice in 2018; Android’s parent Google ranks a distant third.

Digital wallet adoption has been strongest in areas where the new solution addresses substantive existing pain points. Some have suggested that outside of e-commerce settings, digital payments are a “solution in search of a problem.” While we wouldn’t go that far, evidence indicates that consumers are reasonably satisfied with existing physical payments methods and require an enticing incremental benefit in order to alter established behavior.

Such a reading would not bode well for the prospects of US contactless adoption unless it is paired with a compelling proposition, such as the public transit rollouts pending in several metropolitan areas. Apple’s new credit card, launched in conjunction with Goldman Sachs, offers richer rewards for Apple Pay in-store transactions, which could provide a boost to wallet use, and advance the contactless mindset overall.

Avenues for advancement

As consumers’ trust in technology companies increases, traditional institutions will need to step up their offerings to protect share and prevent disintermediation. Apple’s recently launched credit card venture with Goldman Sachs can be viewed as an attempt to address this trust gap, although the natural audience of Apple enthusiasts has already overcome that objection. Banks can emphasize the security of financial institutions, as Zelle does with its P2P messaging.

More broadly, banks’ efforts tend to target the convenience seeker segment, leveraging wallet features as a way to acquire attractive customers. American Express’ Plan-It installment feature has captured an additional $1 billion in card spending, almost half coming from traditional transactors in addition to revolvers. Chase is introducing convenient digital features such as simplified bill payment and P2P quickpay. Chase also aims to broaden the appeal of its Sapphire credit card by extending the branding to checking accounts and offering rewards tie-in for mortgage originations.

Given clear opportunities across three distinct segments, players should also look to tailor offerings to appeal to particular subgroups. Capital One has been particularly aggressive in its outreach to the tech savvy—theone cohort that has shown receptivity to wallet-based lending offers. Capital One has extended its digital suite to include Paribus (which automatically tracks purchases and issues refunds when lower prices are found), Eno (establishes a virtual card as a browser plug-in for each purchase), Resy, and Wikibuy in an effort to increase spend and cement top-of-wallet status. Meanwhile, Wells Fargo heavily promotes the convenience and cost savings of Control Tower, which monitors recurring charges for unneeded expenses.

Although the focus has been on open networks, nonbanks continue to experiment with closed-loop ecosystems as well. T-Mobile has offered a deposit account with above-market rates (on limited balances), a degree of overdraft protection, as well as a $10 credit for Lyft rides. Although not a digital wallet per se, it is a sign that mobile carriers have not yet relinquished their long-held designs on a consumer-facing role in payments via the smartphone.

While not technically closed loop, the significant balances maintained in Venmo accounts leads to similar behavior. Venmo’s Uber partnership points to a robust potential ecosystem encompassing transit, dining (UberEats), and PayPal merchants.

The success in Asia of Alipay and WeChat are inevitably cited as potential models for the US. Although these players may not pose huge threats themselves—US expansion plans appear to be limited to serving Asian tourists—they may serve as a cautionary tale of potential outcomes when technology-forward players enter the payments space and dictate the innovation agenda. Amazon is arguably positioned to achieve something similar if it expands digital wallet acceptance (the Whole Foods acquisition provides an opening on this front) and aggressively promotes Amazon Cash. Seamless experiences address the need to deliver clear incremental benefit over the status quo, and also defend top-of-wallet status.

Later this fall, McKinsey will release broader results from the survey tracking US consumers’ digital payments behavior through mid-2019. It will be interesting to see the extent to which the additional promotion of products like Zelle for P2P and Rakuten for reward shopping has altered existing digital adoption trends. At the same time, major developments like Apple’s credit card rollout and contactless payments enablement for leading public transit systems will not yet have had time to impact the numbers—reinforcing the “long game” aspect of the adoption curve. In any event, financial services providers of all stripes have stepped up their efforts to establish presence and influence the trajectory of a market that shows clear signs of realizing its promise.

Click here to download a PDF (326K) of this article.