E-mobility has reached a tipping point. More than 250 new models of battery electric vehicles (BEV) and plug-in hybrid electric vehicles (PHEV) will be introduced over the next two years alone, and as many as 130 million EVs could be sharing roads the world over by 2030.1 To support these numbers, significantly expanded charging is required—and it will not be cheap. In fact, an estimated $110 billion to $180 billion must be invested from 2020 to 2030 to satisfy global demand for EV charging stations, both in public spaces and within homes.

While EV charging stations in private residences are quite common today, on-site commercial charging will need to become a standard building feature in the next ten years to meet consumer demand. Across the three most advanced EV markets—China, the EU-27 plus the United Kingdom, and the United States—charging in residential and commercial buildings is the dominant charging location for the foreseeable future and will remain key to scaling the industry. Yet without upgrading buildings’ electrical infrastructure, there simply will not be enough accessible EV chargers to satisfy demand. Further complicating matters, EV charging at scale requires careful planning of a building’s electrical distribution system as well as local electric-grid infrastructure.

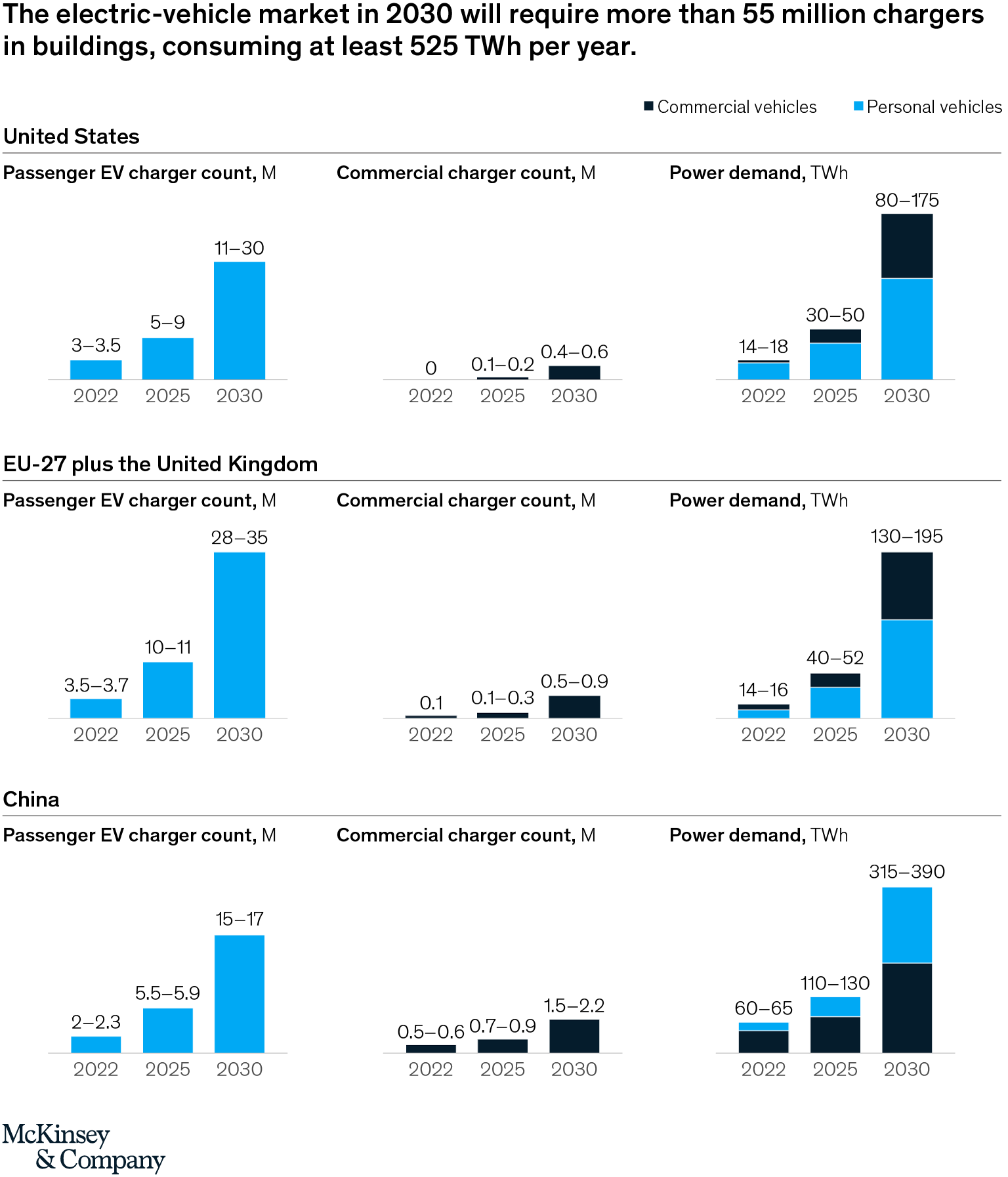

Over the next five years, EV sales are expected to at least quadruple in the EU-27 plus the United Kingdom and more than double in the United States, resulting in the introduction of more than 50 million new passenger vehicles and more than four million new commercial vehicles in China, the EU-27 plus the United Kingdom, and the United States combined. As EV prices decrease and more models become available, EV ownership will reach a broader swath of the vehicle-owning population, encompassing more than 10 percent of sales by 2025 and between 20 and 30 percent of sales by 2030.

We estimate 22 million to 27 million combined charge-point units will be needed in China, EU-27 plus the United Kingdom, and the United States by 2025 and upward of 55 million charge points will be needed by 2030 (exhibit).

Given the challenges and costs, as well as the need to integrate chargers with existing building and grid infrastructure, installing the number of stations needed to scale EV adoption will require the coordination and involvement of entities that may have conflicting interests, such as building developers and owners; urban planners and regulators; electrical consultants, engineers, and architects; charge-point operators; distribution operators and utility companies; and charging-equipment providers.

Shortsighted decisions made today over electrical and civil infrastructure and the capacity and technology of charging solutions could cause EV infrastructure costs to compound to hundreds of billions of dollars. Added to the already-severe costs of peak-demand charges and grid upgrades, the impact of this additional investment could stall the progress of fleet electrification as well as affordable, unhindered access to EV charging.

Market participants—including property owners and building operators, grid operators or integrated utilities, and charging-solution providers and operators—will need to adhere to a number of best practices to enable productive collaboration.

* * *

EV charging infrastructure will operate at the nexus of three different sectors with distinct but interdependent roles in the energy transition: electric power, buildings, and transportation. There is an opportunity today to shape EV-charging strategy to benefit each of these sectors independently, accelerate the progress of the energy transition, and reduce costs for consumers, EV owners, and non-owners alike.

Zealan Hoover is a consultant in McKinsey’s Washington, DC, office; Florian Nägele is a partner in the Zurich office; Evan Polymeneas is an associate partner in the Atlanta office; Shivika Sahdev is a partner in the New York office.

1 Global EV outlook 2018, International Energy Agency, May 2018, iea.org.