Commodity traders crave volatile markets, and they’ve had their fair share of them recently:

- A snowstorm spurred dramatic price spikes in electricity in Texas in February, with clearing prices up to $9,000 per megawatt-hour (MWh) for three days, more than 300 times the average February price of $21 to $27 per MWh.

- The grounding of a giant container ship in the Suez Canal produced a 6 percent jump in daily oil prices. The cost of renting tankers from the Middle East to Asia also rose by up to 47 percent within three days, with ships immobilized or taking longer trade routes.

- In Asia, liquefied natural gas (LNG) prices reached about $20 per million British thermal units (MMBTU) in January 2021, a record, compared with a 2020 average of about $6 per MMBTU, prompting large Asian buyers to explore new long-term contracts to avoid overexposure to the volatile spot market.

- In Germany, increasing supply of prioritized renewable energy has led to a surge in hours of power supply at extremely low prices, from about 200 hours with prices below €5 per MWh in 2016 to about 600 hours in 2020.

Volatility is normal in commodities markets. But energy and commodities companies, including utilities, industrial firms, and trading houses, are now dealing with higher frequency of extreme events. They face four big fundamental changes in the markets.

First, energy markets in particular are becoming more globally interconnected. For example, LNG prices are increasingly connecting major global gas markets to each other1. Similarly, European power and gas trading hubs are increasingly correlated from north to south and west to east, progressively transforming what used to be to a collection of local trading hubs into a more regional market.

Second, markets are trading in real time more than ever; for example, power and gas can now trade in slots of only 10 minutes in a number countries compared with daily a few years ago. As a result, companies are rolling out new intraday trading teams and algorithmic models to cope with this new market structure.

Third, markets are more and more automated; day-ahead and intraday power and gas trades are increasingly the result of automated algorithms rather than human intervention, employing similar techniques used in equity and fixed-income markets.

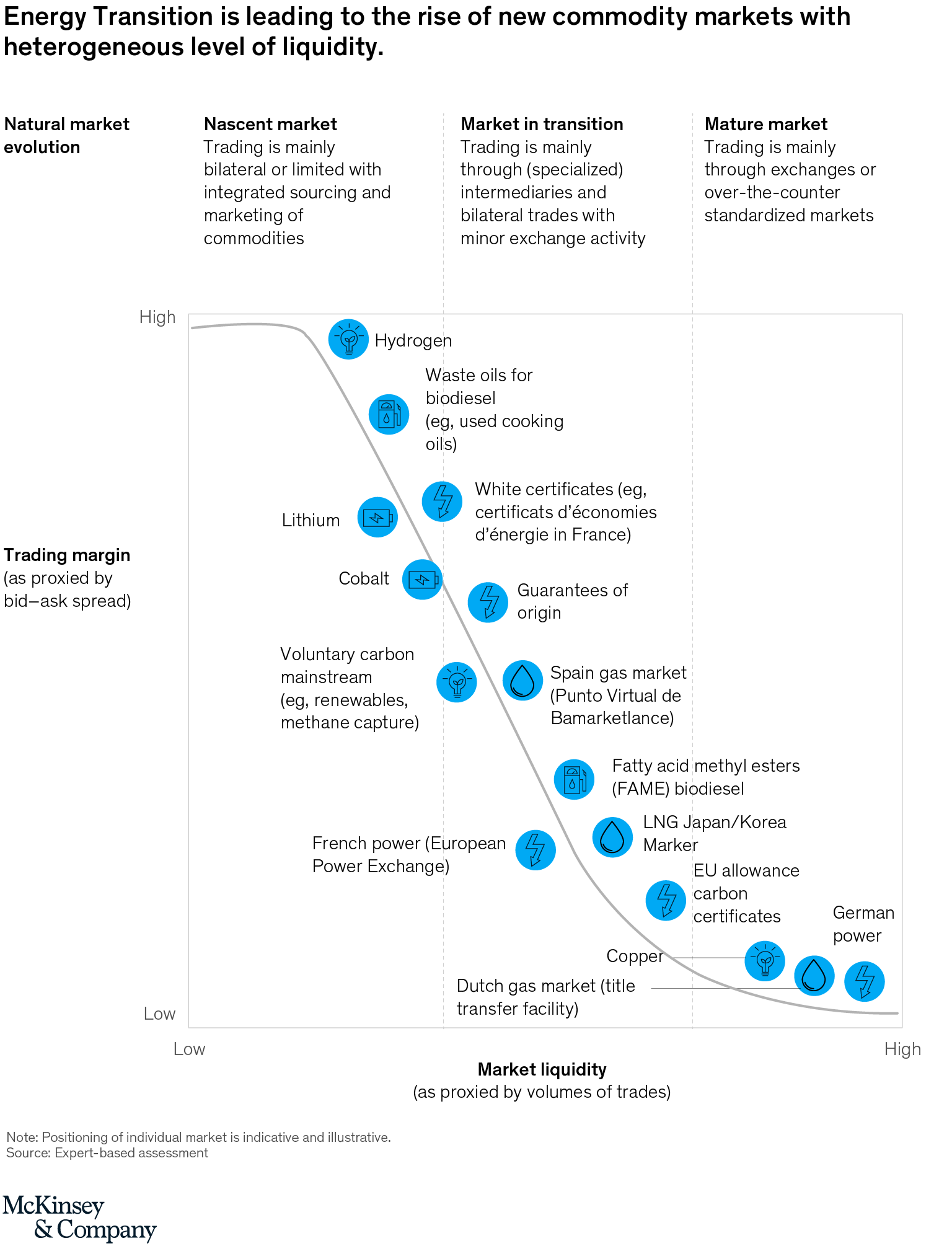

Fourth, the energy and wider environmental transition is giving rise to new commodities (for example, biofuels, renewables guarantees of origin certificates, lithium, and cobalt). These commodities, while initially traded on a bilateral basis, very quickly evolve into over-the-counter (OTC) trading markets with limited liquidity that require strong price risk management.

At the same time, commodity trading has become much more competitive. For example, big industrial companies that purchase large volumes of power and gas are setting up trading desks to procure these products directly on wholesale markets. Energy companies are also expanding across multiple commodities. Oil and gas companies are developing power and carbon emissions trading desks, increasing competition with utilities. New, independent companies are trading power and gas as a service for smaller-scale producers or buyers. Other niche players are also trading new commodities such as biofuels and carbon certificates.

What can energy and commodities firms do to stay ahead of the competition? Five developments are allowing industry leaders to create new sources of value:

- expanding into rapidly growing niche commodity markets

- launching trading-as-a-service offerings

- deploying advanced analytics to automate short-term intraday trading

- rolling out the next level of performance management to optimize risk capital allocation

- adopting best-in-class trade-to-cash processes

The first three levers focus on promoting growth in trading; the last two describe fresh approaches to drive efficiency. Heads of trading business units and chief commercial officers should actively pursue these levers to sustain margin growth in light of strong competition and rapidly evolving markets.

How to spur growth in trading

We have identified three new strategies to promote trading income growth.

Understanding commodity markets fundamentals and targeting new niche markets

During the past 10 years, a significant number of commodity markets have come onstream, often linked with the transition to renewable energy, and the rise of new sources of energy. Examples include European Union emission allowances (EUAs); guarantees of origin (GoOs); first-generation biofuels known as fatty acid methyl esters (FAMEs); used cooking oils (UCOs) acting as a feedstock for second- generation biofuels; white certificates such as certificats d'économies d'énergie (CEE) in France, reflecting energy efficiency credits; and cobalt and lithium for batteries, and many more.

Energy and commodities firms’ trading-desk operations could benefit from a more active presence in these markets, given higher margins than in more mature markets. However, limited liquidity will trigger a need for strong risk management practices. It’s critical for companies to continuously adapt their strategies as markets evolve along the maturity curve. (Exhibit 1)

A number of companies have recently accelerated development of trading desks focused on these commodities, which offer higher trading margins. Also, a direct presence in the market can help industrial companies gain a better grasp of the price discovery process. For example, a number of major global and niche trading firms have recently announced the creation of carbon renewable certificates and biofuel-ticket trading desks. Oil and gas companies have developed biofuels trading desks dedicated to feedstocks such as vegetable oils, UCOs, and other waste oils, as well as products such as FAMEs and hydrotreated vegetable oils (HVOs).

Launching trading-as-a-service offers

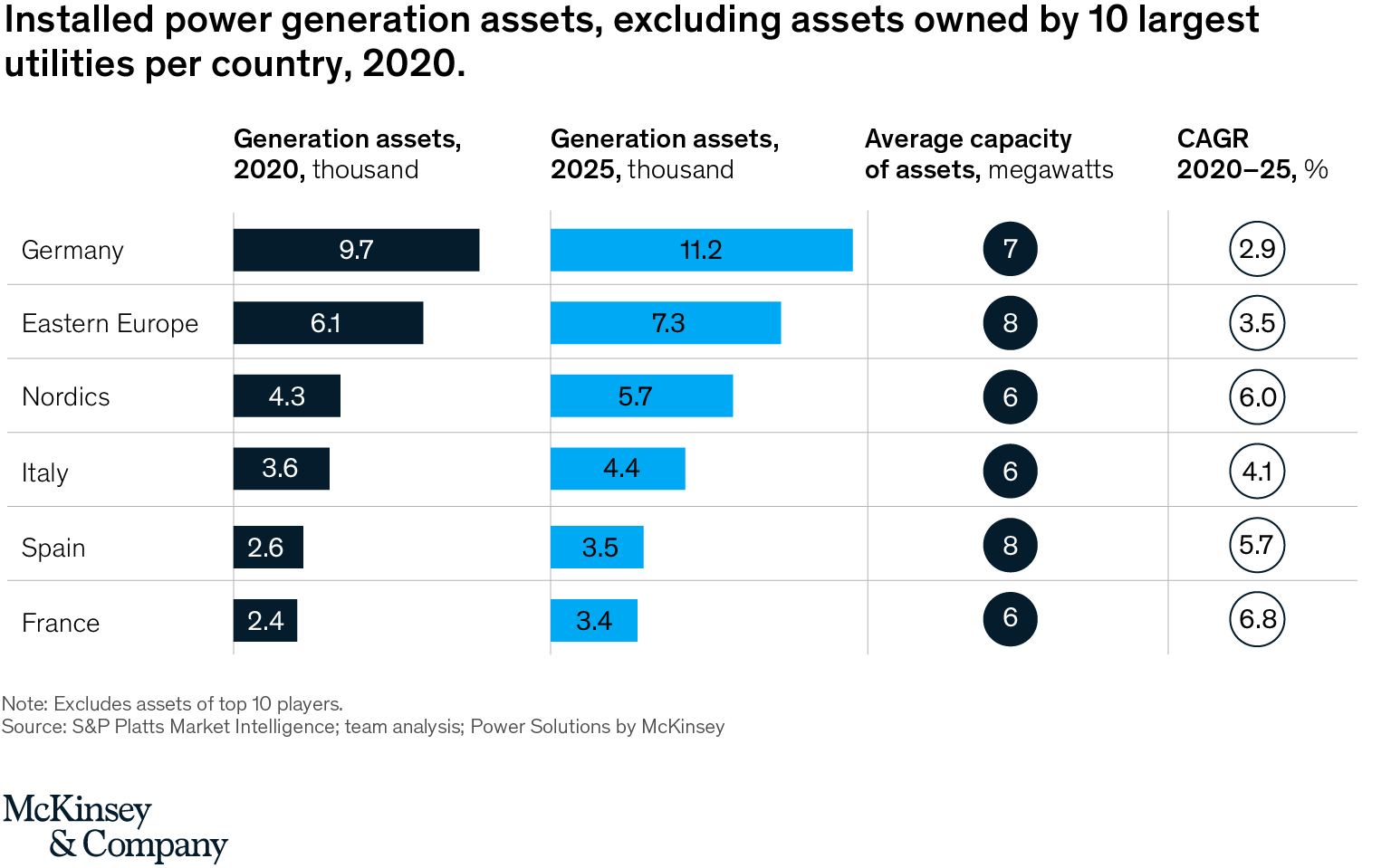

Energy systems are becoming more decentralized, with large-scale power plants replaced by small-scale renewable energy producers (Exhibit 2). Most smaller-scale companies lack the financial means, risk appetite, and capabilities to manage the marketing of their production, exposure to volatile power prices, and the hedging of future production. As a result, they often look for external partners to provide these kind of services. This is a key opportunity for energy companies with trading desks that can scale their activities to offer power purchase agreements, risk management solutions, and market access services to third parties. Many utilities are rapidly expanding into this area.

Harnessing the power of advanced analytics

Advanced analytics are transforming the trading landscape. Traders are deploying these tools as markets become more real time to keep a competitive edge and to maintain or increase trading margins. They are able to do so because of increasing availability of market data as well as satellite, vessel tracking, and weather data; talent skilled in machine learning and statistical algorithms; and computing power, including the cloud, that runs predictive analytics fast enough to identify market signals and then triggers trades.

In our experience, using advanced analytics, especially in volatile short-term markets such as intraday power trading, can make the difference between profitability and risk to exposure of significant income shortfalls. That’s because humans cannot process data fast enough to make rational decisions, especially when large amounts of data must be dealt with and interpreted rapidly.

For example, deployment of advanced analytics can lead to a reduction of more than 30 percent in costs by optimizing bidding of renewable assets in day-ahead and intraday markets. At the same time, we found a productivity gain in intraday trading of 90 percent as a result of employing an end-to-end automated process using advanced analytics engines. As part of the transformation, the role of traders progressively shifted from taking decisions and executing trades toward focusing on market analysis and improving advanced analytics models on a continual basis.

A successful analytics transformation in trading includes:

- Achieving early momentum with a successful use case. Try to self-finance the transformation; early success will contribute to a positive mindset and encourage the rest of the organization to get behind analytics.

- Making business value explicit for each use case and clarifying performance expectations. Companies that start with IT infrastructure and data enrichment tend to invest a lot but not capture the value.

- Changing the way companies recruit new talent and different trader profiles are needed, and creating an attractive workplace for digital and analytics talent is key.

Finding new sources of efficiency

Finding new sources of growth is important, but so is making a continuous effort to improve performance management in trading and to ensure scale and development are not pursued at the expense of efficiency. Traders can look to the following two approaches for additional sources of value.

Rolling out the next level of trading performance management

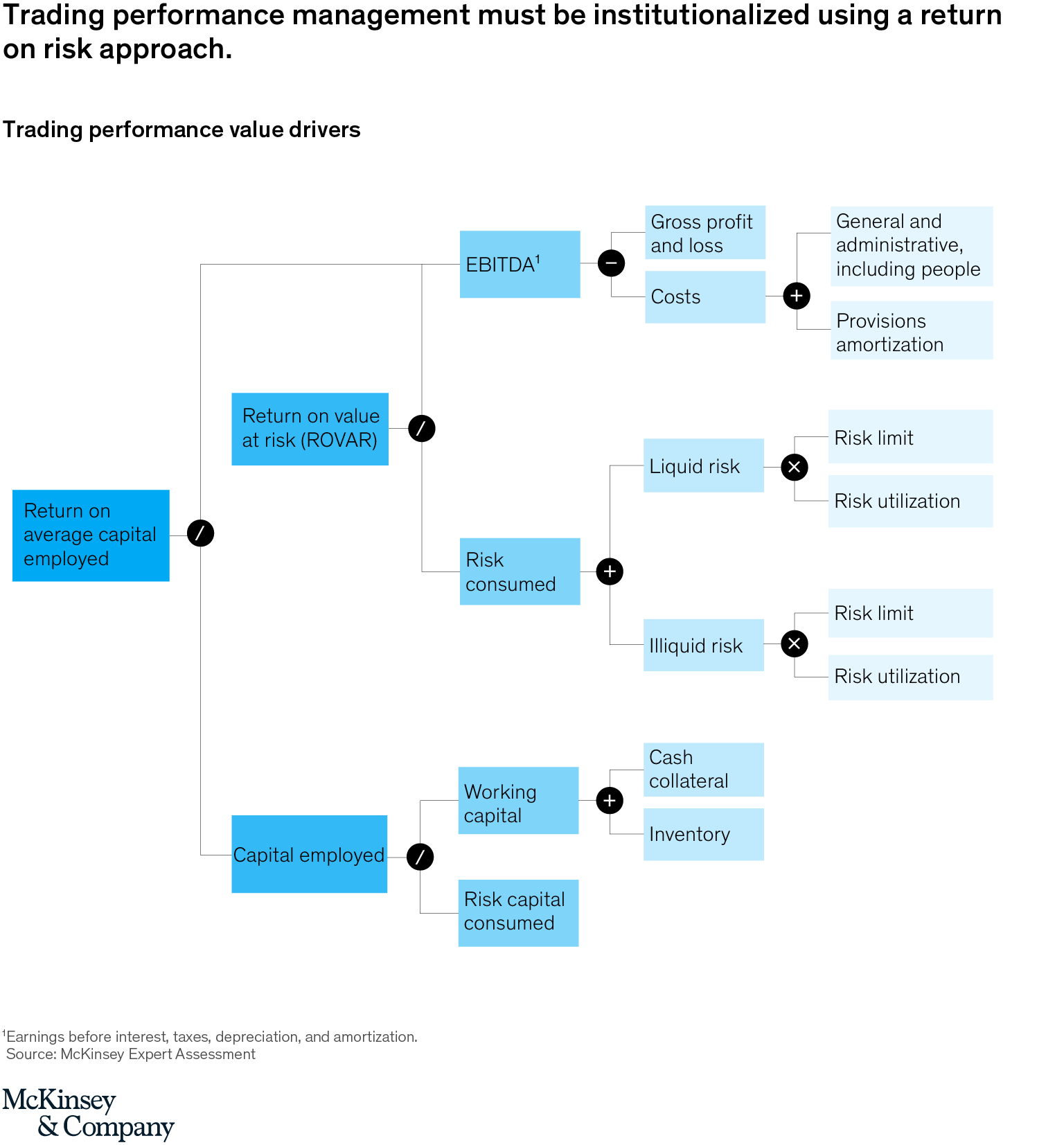

In this new age of commodity trading, the leaders will be those that allocate working and risk capital more efficiently to attractive trading activities and ensure decision transparency. Continuous performance management is critical to optimize risk capital allocation between trading desks and structure incentive schemes that truly reflect risk-adjusted P&L contributions. Optimizing trading performance must be underpinned by a set of key efficiency ratios such as return on value at risk (VaR), risk utilization percentage, trading P&L incorporating cost of capital, and front-office to mid-office and back-office support (Exhibit 3).

Adopting a best-in-class operating model

Traders should strive to adopt a best-in-class operating model and associated processes to maximize economies of scale and synergies as they scale into higher volume of transactions and branch into new commodities. Four key tools to achieve such efficiency include:

- creating a lean front-to-back operating model optimizing the so-called trade-to-cash processes that follow the trading transaction cycle from the time a trade is made through its final settlement

- merging middle-office activities across desks as much as possible to create synergies in daily P&L and risk analytics production

- Developing the right interface with production and marketing assets (for example, power generation plants or B2B sales portfolios) for trading to be able to best optimize the overall company portfolio and monetize optionalities embedded in assets

- Adopting a lean trading IT backbone (from trade execution to settlements) that embraces the latest digital and analytics innovation (for example, transactional data available in a data lake and connection of a commodity/energy trading and risk management (CTRM/ETRM) system to portfolio simulation engines).

***

It’s imperative for trading executives to stay on top of the large structural changes taking place in commodities markets. Pursuing these five levers can best position them for growth: entering new commodities markets to avoid being a price taker but rather a market maker;, launching trading-as-a-service offerings; investing in developing and scaling up trading analytics; institutionalizing a strong performance management framework; and optimizing the trading operating model and associated IT landscape.

Joscha Schabram is an associate partner in McKinsey’s Zurich office, and Xavier Veillard is a partner in the Paris office.

1 For example, the Dutch title transfer facility (TTF) gas market is increasingly connected to the Asian LNG Japan/Korea Marker (JKM) spot gas market.