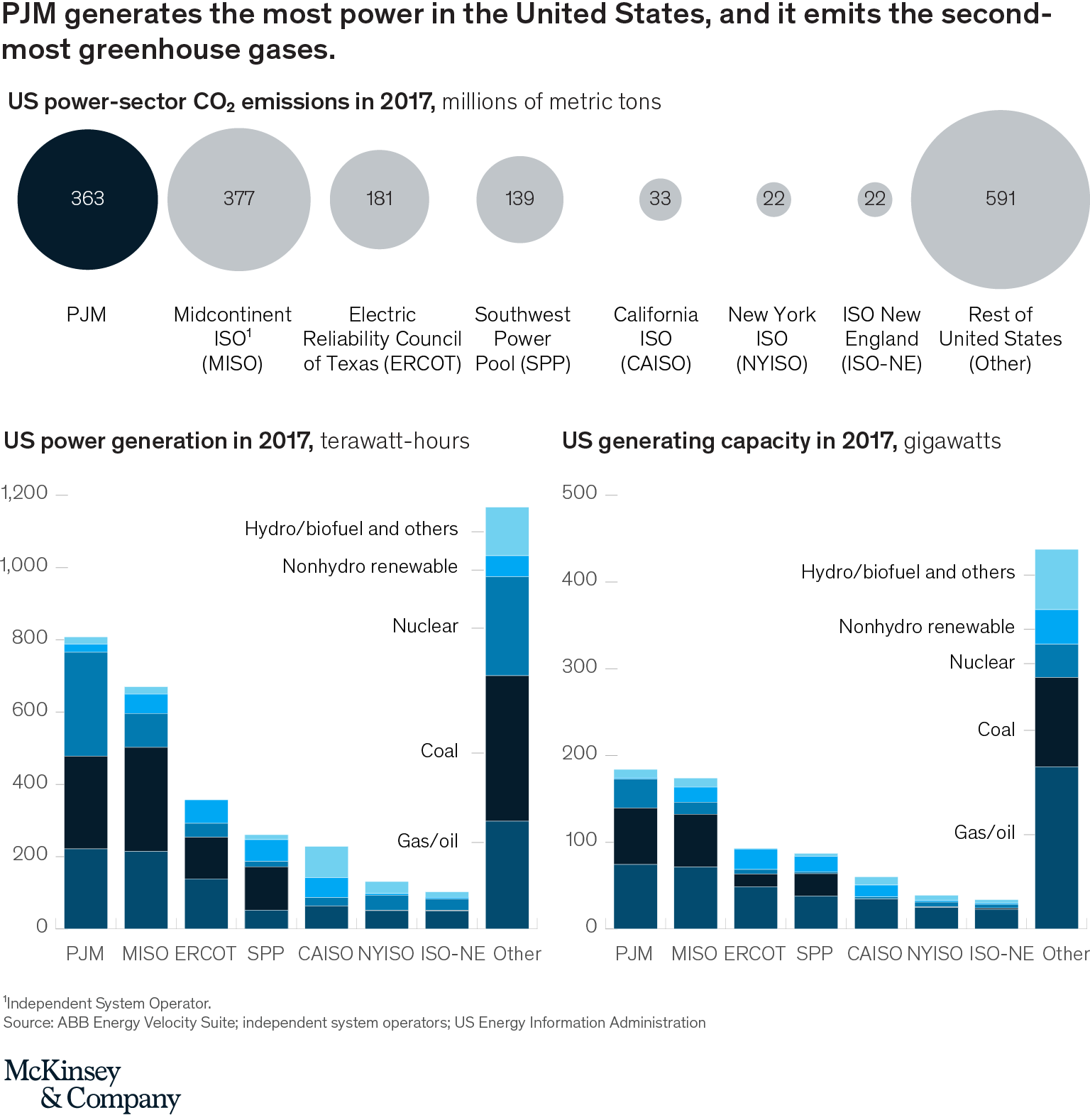

California and New York win the headlines in terms of state action on climate change, but these two states account for only about 3.2 percent of CO2 emissions in the US power sector. By contrast, the PJM Interconnection, a 13-state market,1 accounts for 21 percent;2 it is the country’s largest single power system3 in generation (Exhibit 1), and second-largest in terms of greenhouse-gas emissions. To put it another way, only five countries produce and consume more power than PJM, which serves 65 million people.4

Two scenarios for PJM

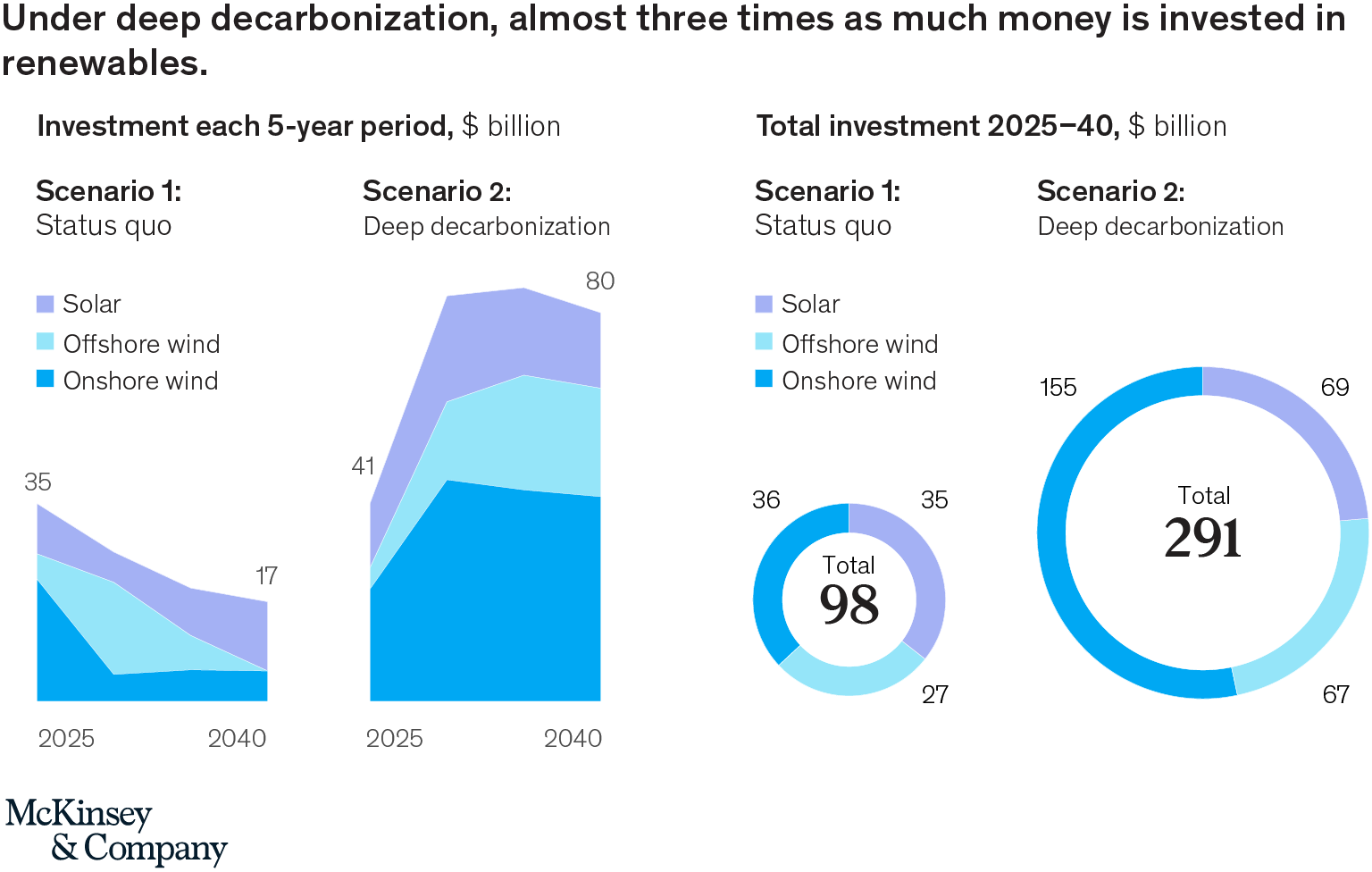

A number of PJM states have announced decarbonization policies. These could reduce PJM’s emissions by 49 percent by 2040 (relative to 2017) and economy-wide emissions in these same markets by 26 percent. We call this the status quo scenario. We also devised a hypothetical, “deep decarbonization” scenario that envisions PJM markets reducing emissions by 95 percent by 2040, and economy-wide emissions by 80 percent.

The difference between the two is stark. Under the status quo scenario, renewable power grows relatively slowly, and the overall capacity of fossil fuel–fired power doesn’t change much, though lower-cost natural gas displaces coal to a large degree. Under the deep-decarbonization scenario, the grid shifts much more quickly toward renewable power, particularly the use of onshore wind Exhibit 2). By 2040, emissions from the power sector decline 95 percent. The transition is costly, however, requiring an estimated additional $193 billion in investment over 20 years.

In both scenarios, power companies build new gas-fired power plants But in deep decarbonization, much less new capacity is installed (38 gigawatts compared with 68 gigawatts), and average utilization—the percentage of time the power plant is actually in use—falls from roughly 50 percent to 25 percent. At such low utilization, revenues would fall, impairing the economic sustainability of much of the natural-gas industry. New market structures may need to be devised to pay the industry for its role in load balancing, even as its contribution to power generation declines.

In terms of its generation profile, connectivity, per capita emissions and the price of delivered power, PJM is broadly similar to the rest of the United States, and its decisions will have a profound effect on how fast and far the country decarbonizes. If PJM charts a feasible path to power-sector decarbonization, the rest of the United States is more likely to do so. If PJM cannot, then the prospects diminish. In a sense, as PJM goes, so goes the country.

Rory Clune is a partner in McKinsey’s Boston office, where Ksenia Kaladiouk is an associate partner; Jesse Noffsinger is an associate partner in the Seattle office, and Humayun Tai is a senior partner in the New York office.

The authors wish to thank Andrea Grass and Chad Powers for their contributions to this article.

1. PJM serves some or all of Delaware; Illinois; Indiana; Kentucky; Maryland; Michigan; New Jersey; North Carolina; Ohio; Pennsylvania; Tennessee; Virginia; Washington, DC; and West Virginia.

2. Although MISO and PJM are, strictly speaking, the names of the organizations that run power markets in these regions, we use the terms to refer to the regions themselves.

3. The term “system” is used to refer to the country’s seven competitive wholesale power markets. Each is run by an independent system operator (ISO) or a regional transmission organization (RTO). CAISO is the California independent system operator and NYISO is the New York independent system operator.

4. International Energy Agency, energyatlas.iea.org.