Although Africa’s growth prospects are bright, they differ not only country by country but also sector by sector. In these articles, we examine the possibilities for seven of them: agriculture, banking, consumer goods, infrastructure, mining, oil and gas, and telecommunications. Perhaps the most fundamental point is that Africa’s growth story is hardly limited to the extractive industries. As many as 200 million Africans will enter the consumer goods market by 2015. Banking and telecommunications are growing rapidly too, and infrastructure expenditures are rising significantly faster in Africa than in the world as a whole. Not that the growth of the extractive industries won’t be impressive. The continent has more than one-quarter of the world’s arable land. Eleven of its countries rank among the top ten sources for at least one major mineral. Africa will produce 13 percent of global oil by 2015, up from 9 percent in 1998. For many companies, this is a future worth investing in.

Agriculture: Abundant opportunities

Kartik Jayaram, Jens Riese, and Sunil Sanghvi

Agriculture is Africa’s largest economic sector, representing 15 percent of the continent’s total GDP, or more than $100 billion annually. It is highly concentrated, with Egypt and Nigeria alone accounting for one-third of total agricultural output and the top ten countries generating 75 percent.

Africa’s agro-ecological potential is massively larger than its current output, however—and so are its food requirements. While more than one-quarter of the world’s arable land lies in this continent, it generates only 10 percent of global agricultural output. So there is huge potential for growth in a sector now expanding only moderately, at a rate of 2 to 5 percent a year. Four main challenges inhibit the faster growth of agricultural output in Africa.

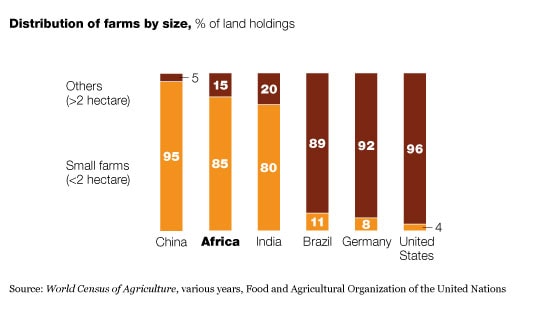

Fragmentation. With 85 percent of Africa’s farms occupying less than two hectares, production is highly fragmented. In Brazil, Germany, and the United States, for example, only 11 percent or less of farms operate on this scale. Therefore, new industry models that allow small farms to gain some of the benefits of scale are required.

Interdependence and complexity. A successful agricultural system requires reliable access to financing, as well as high-quality seeds, fertilizer, and water. Other essentials include access to robust markets that could absorb the higher level of agricultural output, a solid postharvest value chain for the output of farmers, and programs to train them in best practices so that they can raise productivity. Africa has diverse agro-ecological conditions, so countries need to adopt many different farming models to create an African green revolution.

Underinvestment. To make the agricultural system work better, experts estimate, sub-Saharan Africa alone requires additional annual investments of as much as $50 billion. African agriculture therefore needs business models that can significantly increase the level of investment from the private and public sectors, as well as donors.

Enabling conditions. A successful agricultural transformation requires some basics to be in place—transportation and other kinds of infrastructure, stable business and economic conditions, and trained business and scientific talent. Many African countries are making great strides in laying the groundwork, but others are lagging behind.

The small African farm

Over the past five years, the world has reenergized its efforts to improve African agriculture. Africa’s countries have committed themselves to increasing agriculture’s share of their budgets to 10 percent, donors are making significantly increased commitments, and private-sector players and investment funds are pouring serious money into the area.

These increased investments flow toward three general opportunities. The first is developing technological breakthroughs, such as drought-tolerant maize, that would have high returns on investment and could sustainably raise small farmers from poverty. Second, new value chain approaches aim to improve access to markets and help groups of farmers raise their productivity. The third opportunity is the development of selected large tracts of high-potential agricultural land.

New models for large-scale change led by the public or private sectors also have a lot of potential. They include plans rolled out under the Comprehensive Africa Agriculture Development Program, an initiative to help African countries increase their economic growth through agriculture-led expansion. In our work in Africa, several approaches have seemed promising. One is a new kind of industry structure—nucleus farms—to accelerate the productivity of small-holders. These 50-hectare farms are operated by sophisticated farmers who also help small farmers in their areas to become more productive and to market through the nucleus farm. Other approaches include warehouse aggregators (entrepreneurs who own warehouses used to distribute fertilizer and seed and to store crops) and more efficiently run farming cooperatives. Similarly, our work with food manufacturers and retailers shows that end-to-end supply chains that can effectively source produce from African farmers have great potential.

Fifty years after the start of the Asian green revolution, Africa too is poised for one. This will be a complex and difficult undertaking, but the continent seems to be on the right path.

Banking: Building on success

Hilary De Grandis and Gary Pinshaw

Africa’s banking sector has grown rapidly in the last decade. Sub-Saharan Africa has become a substantial player in emerging-market banking, with total 2008 assets of $669 billion, while North Africa’s asset base has grown substantially, to $497 billion. Africa’s banking assets thus compare favorably with those in other emerging markets, such as Russia (with $995 billion).

Almost 50 percent of the growth at Africa’s largest banks came from portfolio momentum—the market’s natural increase—compared with only about 17 percent from inorganic (or M&A-driven) sources. Underpinning this portfolio momentum is strong overall market expansion: the financial sector is outgrowing GDP in most of the continent’s main markets. Between 2000 and 2008, for example, Kenya’s GDP grew by 4.4 percent annually, its financial sector by 8.5 percent. The only significant exception is Egypt, where regulatory restrictions have limited the sector’s growth to only 2.3 percent annually, compared with 4.8 percent for GDP.

Financial reforms have largely enabled this growth. Nigerian banking reform promoted a swift consolidation (from 89 to 25 banks between 2004 and 2006) that unlocked the sector’s potential—bigger banks with better capabilities could drive down their costs, allowing them to penetrate a larger portion of the unbanked population and to ride on the back of rapid economic growth. As a result, total banking assets grew by more than 59 percent annually from 2004 to 2008. In August 2009, the newly appointed central-bank governor initiated reforms to increase accountability and transparency.

M&A activity has also improved productivity, as smaller, less-efficient institutions are being acquired by larger ones. From 2004 to 2009, some 430 M&A deals involved financial institutions in Africa, and about 40 percent were cross-border, with the acquirer originating elsewhere in Africa or outside it. Banks in South Africa are especially active in gaining footholds outside their home market. Further market consolidation is taking place within countries.

New entrants are also gaining share in countries where governments are allowing private banks to enter. Algeria, for example, has been opening up to private players since 1990. From 1990 to 2006, 12 new private-sector banks entered this market.

Although lower growth is expected in the African banking sector in the next few years, attractive opportunities remain—expanding current product offerings, increasing product penetration, bringing the unbanked into the financial system, and capitalizing on the rise of a new consumer class by developing innovative service and channel offerings. Banks have employed several strategies to capture this growth.

A major player

Geographic expansion. The pan-African Ecobank Transnational has more than 11,000 employees in more than 750 branches in 30 African countries. The key to the success of this strategy is the interconnection between the independent subsidiaries, which can tailor offerings to the local market and still benefit from regional connections, such as shared financial and personnel resources.

Entering new segments. South Africa’s Capitec Bank leverages a technology-driven, low-cost banking model attractive to formerly unbanked customers. Its business model has four pillars: affordability, accessibility, simplicity, and personal service.

Product innovation. African Bank, a niche South African institution, emerged in the early 2000s to fill the gap between traditional banks and microlenders. It offers innovative credit and savings products to salaried low- and middle-income customers. Loan applications are assessed in minutes thanks to sophisticated credit-scoring engines and a simplified application process that employs the latest technology, such as biometric scanners.

Improved penetration. As the financial sophistication of existing customers increases, African banks are selling additional products to meet their clients’ evolving needs. In addition to basic transactional products, for example, many banks now offer a credit card or overdraft facility.

Channel innovation. New entrants without established branch networks can adopt a game-changing strategy: using only electronic channels. The mobile-payment service of Kenya’s M-Pesa, for example, has helped formerly unbanked customers by filling a gap in the market.

Expanding along the value chain. Nigerian banks such as Guaranty Trust Bank (GTBank) are expanding, as well as building in-house capabilities in areas that were traditionally the preserve of foreign players—for instance, corporate and investment banks. In doing so, the Nigerian institutions have exploited synergies across their business units.

Consumer goods: Two hundred million new customers

Reinaldo Fiorini and Bill Russo

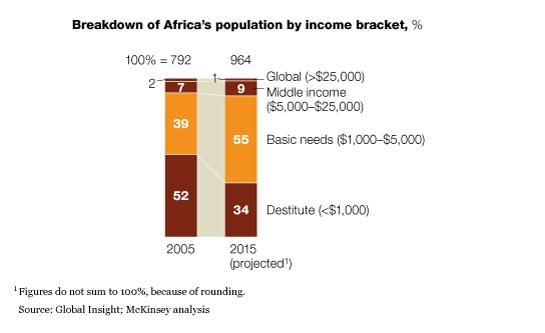

Resources are not Africa’s only driver of growth. Underlying it, the African consumer is on the rise. From 2005 to 2008, consumer spending across the continent increased at a compound annual rate of 16 percent, more than twice the GDP growth rate. GDP per capita rose in all but two countries. Many consumers have moved from the destitute level of income (less than $1,000 a year) to the basic-needs ($1,000 to $5,000) or middle-income (up to $25,000) levels.

In Nigeria, for example, the collective buying power of households earning $1,000 to $5,000 a year doubled from 2000 to 2007, reaching $20 billion. Nearly seven million additional households have enough discretionary income to take their place as consumers.

This evolution is critically important to consumer-facing businesses, from fast-moving consumer goods manufacturers to banks to telecommunications companies: when people begin earning money at the basic-needs level, they start buying and consuming goods and services. Additionally, we have observed that most consumer categories exhibit an S-curve growth pattern: in other words, when a country achieves a basic level of income, growth rates accelerate three- to fourfold. While the exact inflection point differs among categories, many of them are just entering this phase of accelerated growth. The enormous expansion of mobile telephony in Africa provides clear evidence of this phenomenon.

Despite the recent slowdown in economic expansion, GDP per capita should continue on its positive trajectory of a 4.5 percent compound annual growth rate (CAGR) until 2015. That would mean a more than 35 percent increase in spending power. Combined with strong population growth (2 percent) and continued urbanization (3 percent), this increase leads us to estimate that 221 million basic-needs consumers will enter the market by 2015. As a result, the number of attractive or highly attractive national markets—with more than ten million consumers and gross national income exceeding $10 billion a year—will increase to 26 in 2014, from 19 in 2008.

Africa’s new consumers

Many local and multinational consumer companies are already thriving in Africa and delivering handsome returns to their shareholders. To succeed, consumer companies must address five major challenges, some familiar to businesses operating in other emerging markets.

Heterogeneous market structure. Africa has more than 50 countries, with large differences in spending power and consumer behavior, so a one-size-fits-all approach will not work. One consumer goods company approached this problem by segmenting African markets into four tiers, according to market potential and competitive dynamics. In tier-three markets, for example, consumers have low spending power and the infrastructure is poor, so this company simplified production by minimizing the number of SKUs, built strong distribution partnerships, concentrated marketing expenditures at the point of sale, and used smaller pack sizes to increase trial purchases and volumes. In tier-one markets, the company takes a totally different approach: in these relatively wealthy areas, consumers are easier to reach, so it uses direct distribution and sales, offers a full suite of SKUs, and focuses marketing on building the brand through a broad range of advertising approaches.

Low affordability levels. Ninety-five percent of the population and 71 percent of the income remain at the base of the pyramid. Companies thus will not be able to build sizable businesses through premium goods alone; they will have to reinvent their business models to deliver the right products at the right price point. To meet these consumers’ needs effectively, companies must tailor the way they design products and create product portfolios. Additionally, they must learn to compete against local players that have fundamentally different cost structures.

Underdeveloped distribution and route to market. Modern trade is still nascent in most of Africa. The traditional mom-and-pop shops, open markets, umbrella vendors, and the like dominate the retail scene, making up more than 85 percent of the trade volumes. Poor roads and infrastructure can make delivering products to consumers a daunting task, so companies must build strong sales and distribution networks by leveraging a mix of third-party, wholesale, and direct-distribution models.

Nascent categories. In Africa, many categories still are not fully developed; for example, usage per capita of toothpaste is lower there than it is in comparable Asian countries. Data about consumers’ needs and behavior are scarce, making it harder to develop specific consumer insights. In addition, the state of the communications media and education levels make it challenging to reach consumers with specific product messages. Competing in Africa therefore is not a share game. Rather, companies need to bring a market-development mind-set, investing in consumer education and nontraditional marketing techniques.

Talent shortages. Despite the abundant work opportunities, talent remains scarce across Africa. Truly competing and winning in the long term, however, will require local know-how and talent. At first, companies will need to bridge the gap by using a mix of local and international employees. In parallel, investments in developing and retaining local talent are required. Local capability-building programs, attractive career paths, and apprenticeship opportunities will be critical to achieving long-term success.

More on Africa’s consumers

To read more on Africa’s rapidly expanding consumer class, see “A seismic shift in South Africa’s consumer landscape” and “Picking products for Africa’s growing consumer markets.”

Infrastructure: A long road ahead

Rod Cloete, Felix Faulhaber, and Markus Zils

Between 1998 and 2007, spending on African infrastructure rose at a compound annual rate of 17 percent—up from $3 billion in 1998 to $12 billion in 2008, significantly outstripping the growth of global infrastructure investment.1 Africa accounted for 11 percent of total global private-sector and foreign-funded investment from 1999 to 2001 and for 17 percent from 2005 to 2007. This growth has been driven largely by increased funding from non-OECD2 governments—particularly China’s, which provided 77 percent of it in 2007. The private sector is still the largest single source of funds (45 percent in 2007). Rapid growth has attracted many multinational companies within and outside Africa.

While this growth has been substantial, the size of the investment gap that must be closed if the continent is to realize the United Nations’ Millennium Development Goals is more than $180 billion for sub-Saharan Africa alone (2007–14). Governments and the private sector must therefore substantially increase their infrastructure spending. For Nigeria, which aims to be among the world’s top 20 economies by 2020, reaching the same infrastructure levels that Brazil has today would require investments in excess of $190 billion—60 percent of today’s GDP—or an additional 3 percent of GDP for the next 20 years.

So the growth trend in African infrastructure is far from over, and several countries have already announced significant additional spending. South Africa, for example, will invest $44 billion in transport, fuel, water, and energy infrastructure from 2009 to 2011—a 73 percent increase in annual spending from the levels of 2007 to 2008. Since infrastructure investments also offer a high stimulus multiple in times of economic slowdown, Angola, Kenya, Mozambique, Nigeria, and Senegal have announced essentially similar programs, though on a much smaller scale.

Examined at a more granular level, this remarkable growth has clearly occurred in a limited set of countries and sectors. Algeria, Kenya, Morocco, Nigeria, South Africa, and Tunisia were responsible for 75 percent of the investment from 1997 to 2007. Infrastructure spending, fueled by an oil boom, is also growing rapidly in Angola.

Infrastructure partnerships

Lying behind this unevenness are big variations in the size of African economies, economic volatility, political stability, and the quality of logistics, health care, and skills. Almost three-quarters of these countries do not have GDPs large enough to sustain projects of more than $100 million (a comparatively small budget for, say, a port, an airport, a major road, or a power project).3 Similarly, the quality of roads and the density of populations vary considerably. Fifteen African countries are landlocked, and African transport costs are up to four times higher than those in the developed world, complicating the importation of equipment and materials.

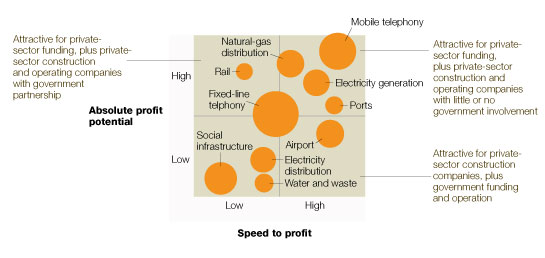

Infrastructure investment has been similarly concentrated in specific sectors. Mobile telephony accounted for more than 30 percent of it from 1997 to 2007 because this market was very attractive and the required infrastructure had a relatively short payback period. Electricity generation, distribution, and transmission accounted for 23 percent of investment as countries across the continent developed large-scale projects (for example, the Bujagali hydroelectric power plant, in Uganda). Infrastructure for natural-gas transmission made up a further 10 percent. Investments in rail, largely in South Africa, took 11 percent of the total. Those in other transportation assets, such as roads, ports, and airports, were limited by poor business cases and long payback periods. Likewise, investments in water and waste made up only 1 percent of the total, given the poor business case for private players.

Yet investment in African infrastructure can be very profitable, with returns “up to twice as high as we get elsewhere,” according to one expert. We have identified five keys to success.

Arrive early and take a long-term view. If a company is to offset short-term currency risks and create the sustained relationships critical to success in Africa, a long-term view is essential. The construction company Julius Berger Nigeria, for example, has more than 100 years’ experience in Nigeria, and the industrial conglomerate Mota-Engil first entered Angola in 1946. Both are now benefiting from the infrastructure booms in these two countries.

Build relationships. The reality of Africa is relationships in quasi-monopolistic markets, as its most important asset classes require special and hence scarce skills, and the operators and project sponsors are typically state-owned monopoly players (for instance, railroads, airport companies, or road agencies). Finding the right local company to partner with gives multinational companies immediate access to excellent political and business relationships, as well as expertise in managing local labor and regulations. Both APM Terminals and DP World, for example, operate most of their African ports with local partners. In many countries, partnering with local companies is required (and where not required, usually favored) in the tender process.

Be vigilant. While risk management is important in all infrastructure projects, it is especially so in Africa, where the range of potential issues is wide and often unpredictable. Equipment problems at Mombasa port, in Kenya, for example, have caused significant, unexpected delays in the delivery of equipment for infrastructure projects in Burundi, Rwanda, southern Sudan, and Uganda.

Manage actively. Because Africa’s business environment is so volatile, active management through the entire project life cycle is essential. One company developing a power plant in the Congo, for instance, discovered through active risk management that significant absenteeism in the workforce could be traced to the local traditional leader’s dislike of the company’s agreement with him. It had to resolve the dispute quickly to prevent a shutdown.

Diversify your project portfolio. No company can avoid all the risks associated with infrastructure in Africa. Successful companies therefore maintain a wide portfolio of projects. One approach is to diversify by geography: for example, APM Terminals operates ports in seven African countries. The other is diversification by sector: GE provides equipment for both power plants and railways; Julius Berger, construction services for transportation, commercial and residential property, ports, and the oil and gas industries in Nigeria.

Fast-growing companies have used different strategies to combine these sources of success. Some go deep into one country and then proliferate across its business environment, especially if relationships and local understanding are critical. This approach is most important for construction companies and funders, since asset-specific expertise is not the most essential value driver for them. The engineering, construction, and petrochemical company Odebrecht, for example, entered Angola to develop the Capanda hydroelectric dam and has since expanded into residential and commercial construction, mining projects, and a partnership in a diamond exploration venture.

Other companies do business in a broad range of geographies, but in a specific class of assets (for example, ports and airports). This approach makes sense, especially for operators. If there are network effects beyond an individual country’s borders, it is best to operate assets in a highly standardized way at a global level. DP World, for example, entered Africa through the Doraleh Container Terminal, located at the port of Djibouti, in 2000 and has since expanded to six terminals across Africa.

Mining: Unearthing Africa’s potential

Pepukaye Bardouille, Alasdair Hamblin, and Heinz Pley

Africa’s mining sector presents a paradox: although the continent is strongly endowed with mineral resources, mining has not been the consistent engine of economic development that people in many countries have hoped for. Nor, to date, has Africa attracted a share of global mining investment commensurate with its share of global resources. Unlike the output of most economic sectors (though like oil and gas), most minerals are globally traded. Global demand is therefore driven primarily by the needs of developed nations and the pace of growth in a few large developing countries. What’s more, mining areas in Africa compete with those elsewhere for development funding. From a growth perspective, the question facing the sector is thus whether and how Africa can make its full potential contribution to satisfying the world’s ever-growing need for mineral resources and capture wider socioeconomic benefits from their development.

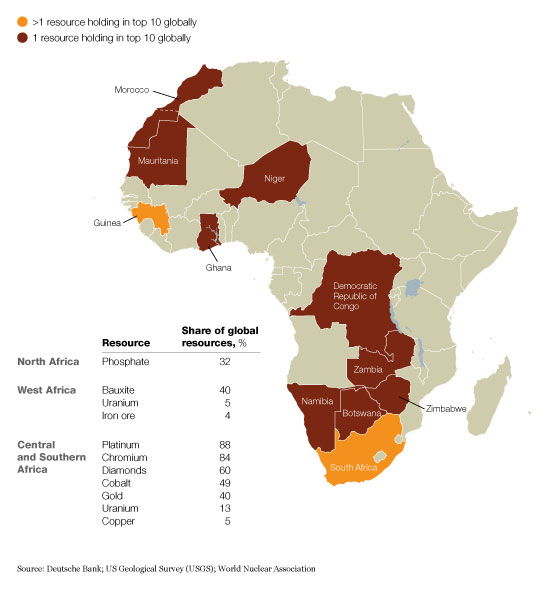

Many parts of Africa have long been known to be rich in mineral resources. Eleven of its countries, especially in southern and western Africa, rank among the top ten sources for at least one major mineral. The continent has a majority of the world’s known resources of platinum, chromium, and diamonds, as well as a large share of the world’s bauxite, cobalt, gold, phosphate, and uranium deposits. The development of these resources has faced more significant challenges, however, when compared with the experience of more developed mineral-rich countries, such as Australia or Chile. Even outside well-publicized conflict zones, many African countries have been thought to pose high political and economic risks for investors. Furthermore, infrastructure problems often hinder development: many bulk mineral deposits require multibillion-dollar investments in rail and port facilities to allow ore or semiprocessed minerals to reach their markets. Such investment decisions are not taken lightly, especially for less stable countries where the rule of law and security of tenure are not necessarily guaranteed.

Largely as a result, Africa’s pattern of mining investment differs from that in other regions of the world. Of the five largest global diversified mining companies, only one has a major share of its production in Africa. With the diversified majors relatively quiet, junior mining companies and major ones focused on diamonds and precious metals have played a significant role in developing the continent’s resources. In recent years, newer players, such as Chinese and Indian companies, have entered the scene, but few projects have been developed to the point of production.

The recent financial and economic crisis has hit the global mining industry hard—and Africa at least as severely as other regions. Commodity prices slumped by 60 to 70 percent in late 2008, although they have since recovered considerably. There is now less appetite for the relatively high risk that usually comes with mining in many African countries. Despite the recent market turbulence, most observers expect demand for major mined commodities to grow strongly in the next 10 to 20 years, to support increased urbanization and infrastructure build-out in China and the emergence of India’s middle class. Africa, given its share of global resources, will surely play a significant part in meeting that demand.

Rich in resources

For mining companies and investors, the economic crisis has taken the froth out of the market. But it hasn’t fundamentally changed many of the factors that will shape long-term investment decisions, including political and economic stability, taxation regimes, and the availability of infrastructure. Nor, of course, has it changed the underlying geology. Lower commodity prices and stock market valuations have shifted the “build or buy” balance between in-house exploration and development, on the one hand, and mergers and acquisitions, on the other. If valuations continue to recover, this window of opportunity may be short-lived.

Over the longer term, international companies considering investments in Africa will need to spend time and energy to gain a deeper understanding of the unique challenges of every African country. They should learn from the success stories of other players, assess risk comprehensively, and determine the role each country will play in their portfolios. Mining projects will need to include the broader socioeconomic-development programs that have been commonplace in petroleum for many years. In many cases, these programs will be achieved through partnerships between mining companies and other parties, which will provide financing and infrastructure development.

Africa’s governments will play a major role in shaping the future environment. In recent years, governments have expressed frustration about the way the continent’s resource endowment hasn’t translated into economic development. The African Union and the UN Economic Commission for Africa (UNECA) have developed the African Mining Vision 2050, which sets out a number of ideas for increasing the resource wealth flowing to the nations that host mining operations. Some of these ideas would transfer wealth from mining companies to governments—for example, by making the auctioning of exploration rights more effective and linking taxation to commodity prices more closely. Others, such as the better management of resource income and the active development of the supply and infrastructure sectors, aim to create a more favorable environment for economic development.

Oil and gas: New sources of growth

Occo Roelofsen and Paul Sheng

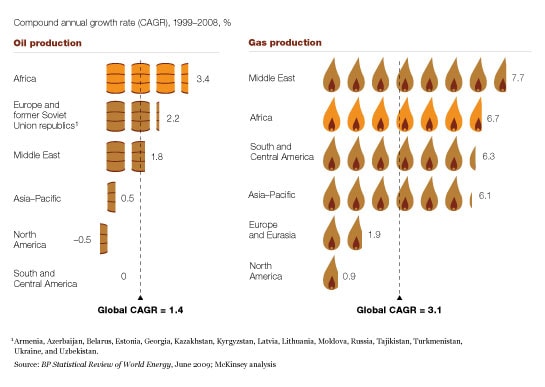

African oil and gas have become important components of the world’s hydrocarbon supply–demand balance. By 2015, 13 percent of global oil production will take place in Africa, compared with 9 percent in 1998—a 5 percent compound annual growth rate (CAGR). African oil projects have attracted substantial investment thanks to their cost competitiveness versus those in other regions.

What’s more, the oil and gas sector is a foundational element of economic growth for the continent, as 19 African countries are significant producers. It accounts for a significant part of the state’s revenues there and represents a prime mover for employment, domestic power development, and, in many cases, infrastructure development (for instance, schools, hospitals, and roads).

The sources of growth in oil and gas are evolving. In the past decade, production increases came primarily from deepwater oil in Angola and Nigeria, along with new sources in countries such as Chad and Sudan, as well as offshore gas in Egypt. Production of deepwater oil will continue to grow (in the Gulf of Guinea, for example), while onshore gas and new-resource development in emerging East African hydrocarbon producers (such as Uganda) are expected to become the other main engines for growth.

International oil companies as a group have fared well in Africa, as the licensing of acreage and M&A gave them access to valuable properties. These companies have also moved expeditiously into the new, technically complex frontiers of liquid natural gas, deepwater oil, and underdeveloped countries (Chad, for example). Superior operating capabilities and financial muscle continue to give the internationals a competitive advantage in Africa; however, sustained growth has eluded those that acquired little and mainly operated more mature fields or had operations in countries with geopolitical and security risks.

Large and growing

Indigenous national oil companies have set ambitious goals to become stand-alone, commercially viable domestic (and in some cases international) operating organizations. The inefficiencies of working in bureaucratic environments where these companies must strive to meet economic and sociopolitical missions have stifled their development, however. National oil companies have been further constrained by the challenge of developing local technical, commercial, and managerial capabilities. These companies must transform them fundamentally and create systems, a performance culture, and governance models along the lines of those found in commercially driven enterprises.

In recent years, new kinds of competitors have entered and grown in Africa, once the domain of the large international oil companies. Smaller independent oil companies (such as Addax, Heritage Oil, and Tullow Oil) have made successful finds in emerging basins. National oil companies from outside Africa, including China (CNPC, CNOOC, Sinopec), Malaysia (Petronas), and Russia (Gazprom) have also aggressively invested in the continent, linking broader infrastructure investments and government-to-government relationships with access to resources. The challenge for these competitors in the years ahead will be to build sustainable enterprises and local capabilities beyond the scope of an individual project or investment.

As for the countries that host oil and gas operations, they should continue to offer international and national oil companies alike an attractive investment environment, which ought to foster competition for natural resources, greater efficiency in the oil and gas sector, and the building of sustainable capabilities. Governments must also focus on new ways to leverage their resource sectors to capture the economic multiplier of broader GDP growth—for example, by using oil and gas as the catalyst for downstream energy (such as power stations, refineries, and retail outlets) and related industrial development (petrochemicals and basic materials).

Telecommunications: From voice to data

Zakir Gaibi, Andrew Maske, and Suraj Moraje

Telecommunications has been an important driver of Africa’s economic growth in the last five years. The market is increasingly competitive, and world-class local enterprises are emerging in voice and data services. Telecom revenues have increased at a compound annual growth rate (CAGR) of 40 percent, and the number of subscribers rapidly exceeded 400 million. To meet the increased demand, investment in telecom infrastructure—about $15 billion a year—has also grown massively, with a 33 percent CAGR from 2003 to 2008.

But annual growth will slow down to the low double digits—still quite enviable by Western standards—as the traditional urban markets become saturated; penetration in major cities such as Abidjan (Côte d’Ivoire), Lusaka (Zambia), and Libreville (Gabon) is 70 percent or more. Still up for grabs are two key pockets of growth, data and rural voice, with an additional revenue pool of $12 billion to $15 billion by 2012.

About 50 percent of the growth in voice will come from rural areas. To capture this opportunity, however, operators and regulators must forge new industry practices. The industry structure should be rationalized, for example, because many markets, even smaller ones, have four or more players. Also needed are new operating models, which might be created by slashing the cost of deploying base stations by 50 percent or more, innovating in distribution and recharging practices, and seeking more individualized pricing models, ideally delivered directly to customers rather than through advertising.

Data services are the other large growth pocket, of about $5 billion, and that’s not all. Experience in other countries suggests that a 10 percent increase in broadband penetration translates into additional GDP growth of some 0.5 to 1.5 percent. Social welfare improves as well; many small-boat fishermen in Senegal, for example, now use mobile-data services to select the best ports for unloading their catch each morning, increasing sales by 30 percent. Applications such as mobile health care will also provide significant benefits, helping governments to stretch thin resources further. McKinsey’s experience in developing markets indicates that 80 percent of health care issues can be resolved by mobile phone, at a cost per capita that is 90 percent lower than that of traditional health care models.

Extending the signal

Policy makers can help drive the data market in several ways, including making lower-spectrum bands available, promoting infrastructure sharing, providing rollout incentives, and, potentially, reducing rural license fees. To capture this opportunity fully, operators must adapt their operating models—for instance, by developing low-cost off-peak packages, scaling up compelling applications, and making data-enabled handsets available more cheaply.