The euro’s future is in limbo. GDP growth in emerging markets is slowing. Uncertainty about sovereign debt threatens economic growth across the globe. It’s no surprise, then, that in our latest survey on economic conditions,1 executives’ expectations for the global economy are the lowest they have been since March 2011.

This survey was in the field in the week leading up to Greece’s elections, and the responses reflect the chronic concerns about the country’s debt and the eurozone as a whole: the largest share expect Greece to default on its debt, sovereign-debt defaults are the most-cited risk to global economic growth, and executives are almost twice as likely as in March to expect a eurozone recession in the next six months. After a renewed vote of confidence in their own economies three months ago, most executives—and a particularly high share of those in Europe—expect economic conditions in their countries either to stay the same or to worsen.

All that said, executives remain optimistic about their companies’ prospects. Only 15 percent say customer demand for their companies’ products and services will decrease, and more than half expect profits to increase in the next six months. But this optimism does not extend across all regions and industries: larger shares in India and in the manufacturing sector now expect demand to decrease than did in March.

Global grief

Only 10 percent of executives say current conditions in the global economy are better now than they were six months ago, and just 20 percent expect conditions to improve in six months’ time. This result is a notable drop in optimism since the previous survey and also the smallest share expecting better economic conditions since March 2011, when we began asking the question (Exhibit 1).2

Given the survey’s timing,3 these results are no doubt linked to the political and economic uncertainty in the eurozone, where 46 percent of global respondents expect to see a recession in six months. Respondents in the eurozone are more optimistic than average about the region’s prospects: only 32 percent of executives there expect a recession, while 35 percent expect minimal contraction of the economy. Even so, the share predicting recession has grown since March.

Over the next decade, the largest share of executives still believe that emerging-market leadership is the likeliest outcome for the global economy, despite the slower GDP growth that India and Brazil posted in the first quarter of the year.4 There is a notable shift in the share of executives expecting both developed and emerging markets to struggle with ongoing structural challenges, as well as multiple economic and financial shocks: 24 percent predict this outcome, compared with 15 percent who said so in March.

Domestic tensions

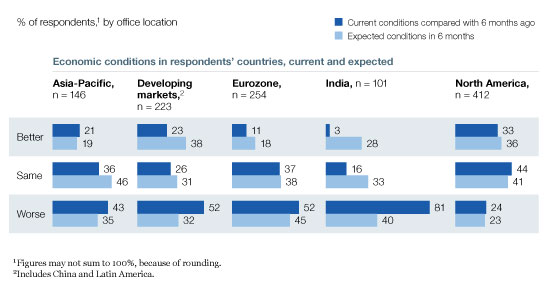

Along with their sweeping concern for the global economy, executives are more negative than positive about their own countries—just three months after their views were moving in a consistently optimistic direction—though the extent of the pessimism varies across regions (Exhibit 2). Only one-quarter of respondents in North America say conditions in their economies are worse now than they were six months ago, compared with 52 percent in developing markets5 and 81 percent in India who say the same.

Likewise, few executives in the eurozone countries (11 percent) believe conditions have improved or that they will in six months (18 percent). Those in developed Asia are equally wary of improving economic conditions, with nearly half saying conditions in their countries will stay the same; roughly one-quarter of executives in the region said the same three months ago. As in March, expectations for unemployment vary by region, and respondents in the eurozone are still the most likely to say unemployment rates in their countries will increase.

Country-level views differ

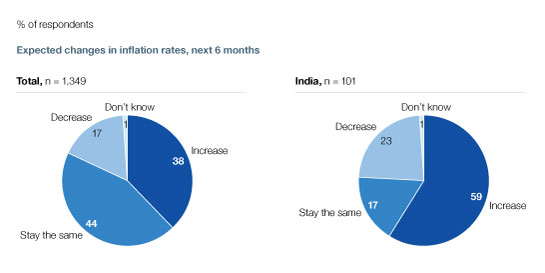

In India, executives have a particularly negative outlook on inflation, which the majority of respondents there expect to increase in the next six months (Exhibit 3). Fifty-four percent also cite inflation as one of the biggest risks to economic growth in their country in the next year, second only to insufficient support from government.

Inflation-wary India

The risks ahead

For the fourth survey in a row, executives cite low consumer demand most often as a risk to economic growth in their countries.6 Still, despite otherwise gloomy expectations, most respondents maintain a rosy view of their own companies. Only 15 percent expect demand for their companies’ products and services to decrease in the next six months (compared with 13 percent in March), while just 21 percent expect the size of their workforces to decrease, and more than half say their companies’ profits will increase.7 Not everyone has high hopes for their companies, though: executives in India are likelier to expect decreased demand— 14 percent now say so, compared with 6 percent in March—and the share of manufacturing executives expecting a decrease in demand rose to 24 percent, up from 13 percent three months ago.

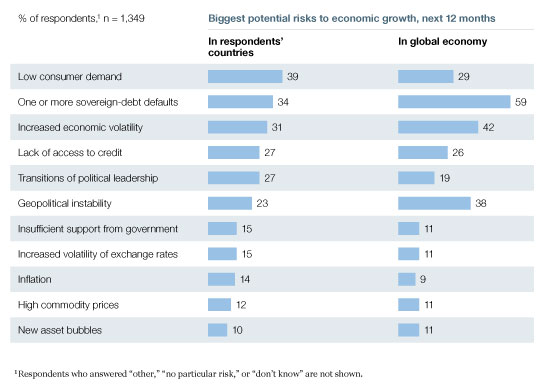

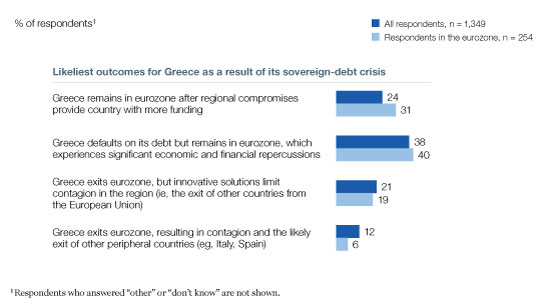

Yet new threats to growth have emerged: respondents say that sovereign-debt defaults and economic volatility are among the top three risks at both the country and global levels (Exhibit 4) and are cited much more often than they were three months ago.8 It is not surprising, then, that the largest share of respondents expect Greece to default on its debt. Executives in the eurozone countries are more likely than average to say Greece will stay in the economic and monetary union (Exhibit 5), yet they are also likelier than others to cite sovereign debt as a risk to growth in their own countries. With respect to the global economy, respondents in all regions are most likely to cite sovereign-debt defaults as one of the biggest risks to growth over the next year.

Sovereign debt and volatility threaten growth

Default predicted for Greece

Considering the long-term obstacles, executives say government regulation, low levels of innovation, and geopolitical instability will most likely hinder their countries’ economic growth over the next decade. The risks vary greatly by region: respondents in developed Asian countries, for example, are more concerned with access to talent while those in India cite a lack of access to energy and commodities much more often than the global average.