Executives’ economic expectations, though gloomy, don’t appear to have worsened notably over the past six weeks, according to a McKinsey Quarterly survey in the field from January 27, 2009, to February 2, 2009,1 during another round of significant layoffs and falling stock prices. Many respondents say government action has made the economic situation better than it would have been otherwise. Looking ahead, more executives say government help should focus on fostering innovation than on helping existing companies or industries. Most companies, respondents indicate, are still coping with the crisis by cutting costs, and many are also making more use of long-term tactics (such as restructuring) suggesting that they see the global economic turmoil as the new normal.

Battered but resilient economies

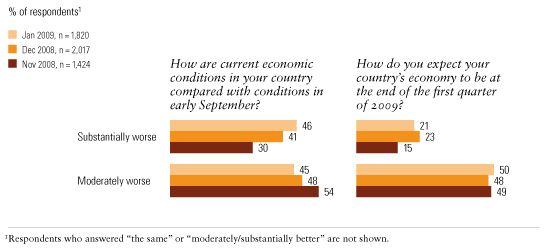

Three-quarters of all respondents, and more than 90 percent of those in the eurozone, expect their nations’ GDP to fall in 2009. This is an increase from November, when 59 percent of all respondents expected GDP to fall. Given that opinion, it’s not surprising that executives indicate that their nations’ economies are bad and that they have low expectations for the near term. Notably, however, those views have remained fairly stable between December and January, after falling markedly between November and December (Exhibit 1). This may indicate a belief that the economy has hit bottom and that even tens of thousands of layoffs and continued steep losses in shareholder value aren’t worsening the situation. Some 40 percent of respondents expect an upturn to begin by the end of this year. Many executives are betting on the United States to lead that upturn, whenever it comes; more than a third say the upturn will start in North America, followed by 26 percent who expect it to start in several regions at once. This global hope for North America is aligned with earlier findings—that executives in North America have consistently been slightly more positive about their country’s near-term economic chances than those in other regions, which continues to be true in this survey.2

The new normal

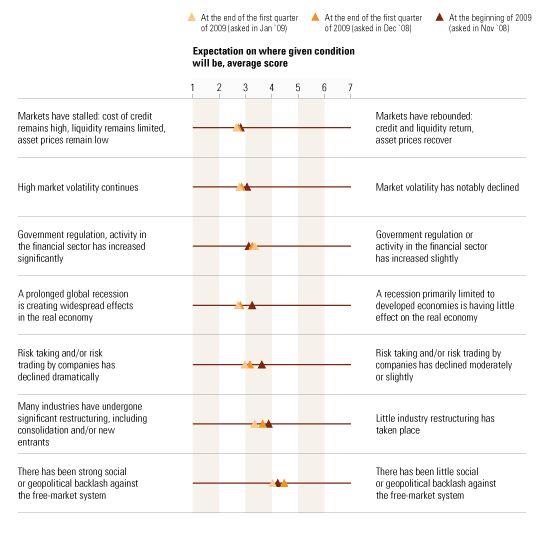

Overall, executives’ views on a series of macroeconomic trends indicate slightly less confidence in recovery than reported in November and December (Exhibit 2). However, when executives were asked about a set of possible future scenarios created by grouping those trends and other factors together, more—44 percent—say they expect a battered but resilient economy than any other outcome. This implies a recession of 18 months or so, with a recovery driven by effective regulations and fiscal policies, safe leverage ratios, and moderate recovery of trade and capital flows. More than half of the respondents, 55 percent, say a long freeze, characterized by a recession that lasts for more than five years and continued tight credit, is the least likely outcome.

Gradual deterioration

Government: The good guy?

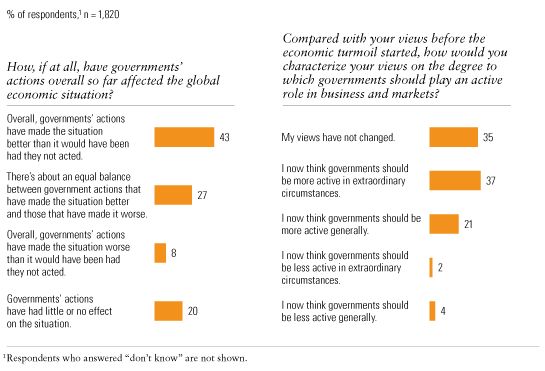

Survey responses indicate that, as bad as things are, they might have been worse. Overall, 43 percent of respondents say governments’ actions have helped. Furthermore, a majority say that, compared with before the crisis, they now think governments should be more active in business and markets at least some of the time (Exhibit 3).

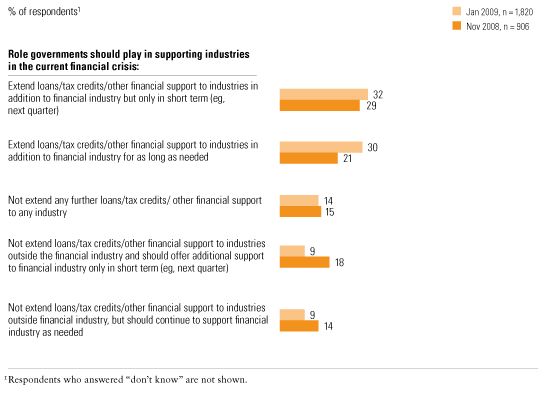

Following up on questions we asked in November, just after the US presidential election, this survey asked respondents about the actions governments should take in supporting industries, in regulation, and in fiscal and monetary policy. Executives now indicate a bit more favor for long-term government support of a range of industries (Exhibit 4). Executives in North America are the likeliest—at a fifth—to say government should extend no further financial support to any industry, while those in the developed countries of Asia are likeliest, at 42 percent, to encourage support for all industries as long as it is needed.

Government in action

Supporting industries

On regulation, executives have increased their focus on banks’ basic operations, with 45 percent now saying governments should be more active in regulating banks, compared with 37 percent in November. This increase may be related to many banks’ ongoing operational troubles.

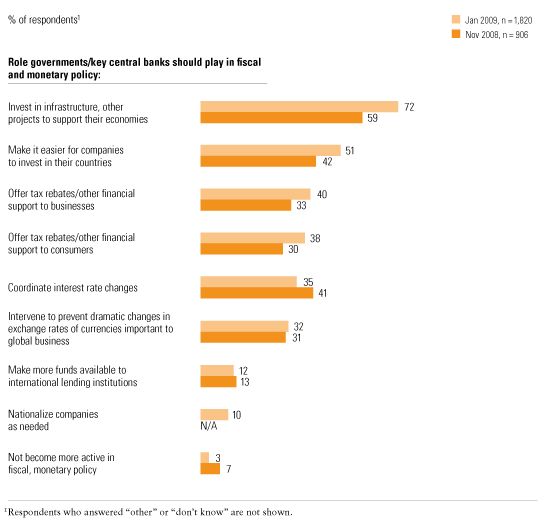

In addition, executives’ support for infrastructure projects as a way to boost economies has expanded markedly since November (Exhibit 5), even more than the increase in support for tax rebates or other financial support.

Infrastructure first

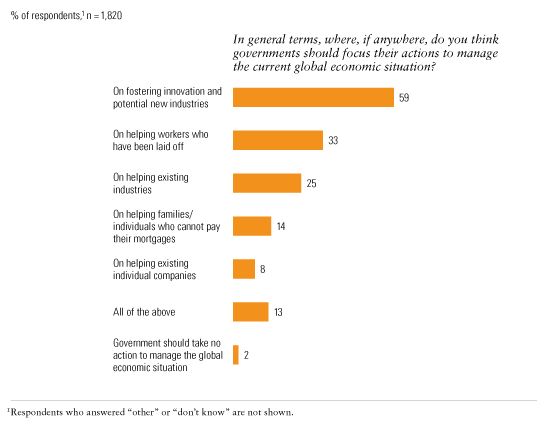

Whatever specific actions governments take, executives indicate that support for innovation should be the overall focus of governments’ actions, rather than help for existing industries or companies (Exhibit 6).

Innovate to improve

Companies hanging on

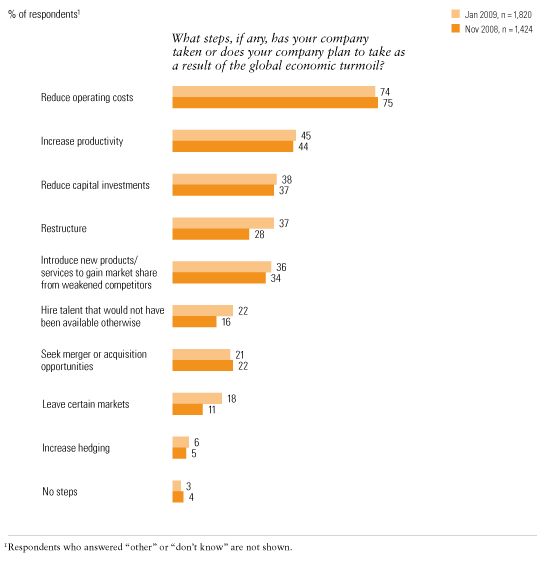

Companies are on the whole sticking to the tactics they identified last fall as helping them manage the global economic turmoil (Exhibit 7). A higher proportion of companies are now taking longer-term actions such as restructuring, hiring talent, or leaving markets altogether, perhaps indicating that more see the turmoil as creating long-term structural changes.

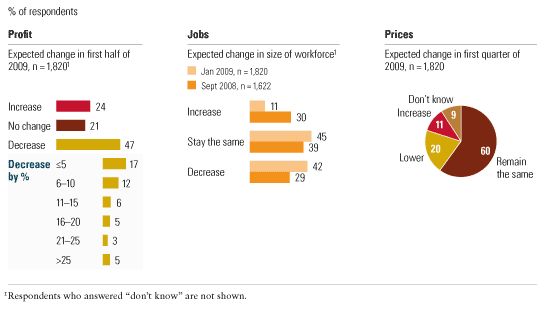

More executives expect their companies to shrink than grow in 2009 in terms of profits and workforce size; however, most have not changed prices and don’t expect to (Exhibit 8). Just under half of all respondents say their profits fell in the second half of 2008.3 But even those who saw profits increase aren’t necessarily well placed: 49 percent of them expect profits to rise again in the first half of 2009, but 29 percent expect profits to fall. For those already doing poorly, the news gets worse: more than two-thirds of those that saw profits fall in 2008 expect profits to continue dwindling in 2009.

Managing the crisis

Company expectations

The proportion of companies that have sought external funding since mid-September has remained stable over the past six weeks, at about a quarter. The same proportion, nearly half, were able to obtain all the funds they needed, and most of the rest were able to obtain some. Among respondents whose companies got funding, just over half say the cost of funds was higher than funds obtained before last September, a proportion that has remained stable since October.