Executives are ending the year with an outlook that’s more positive than negative, though they remain concerned that overall anemic consumer demand will threaten growth, according to our most recent survey on economic conditions.1

Respondents’ views on country-level prospects differ notably by region. Those in developed Asia, for example, are more likely than their peers to say current conditions in their countries have worsened and that future conditions will improve. Across regions, new concerns have emerged: executives in developed economies are much more likely than they were in September to cite insufficient support from government (that is, a lack of fiscal or monetary policies that support economic and business activity) as a risk to domestic growth.

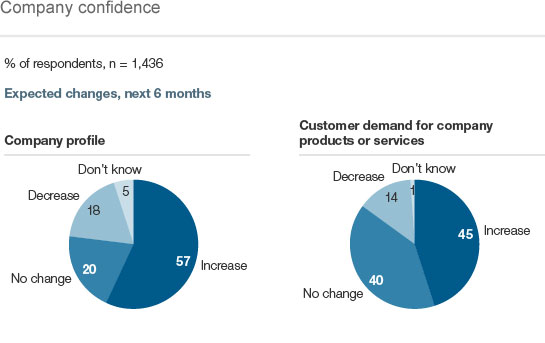

Beyond the more optimistic global outlook that respondents report, the latest results indicate two other bright spots. Executives broadly believe that demand for their companies’ products or services—as well as their companies’ profits—will increase in the next six months, despite their concern about sluggish global and domestic demand. They also predict that emerging markets will continue to drive global growth and are less likely to expect a sharp slowdown in China’s growth over the next year and the next decade than they were in September.

Global hope and hazards

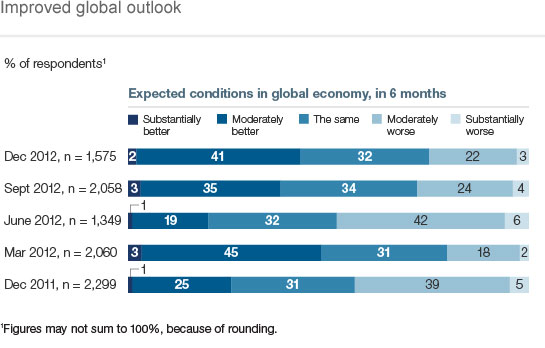

At year’s end, the largest share of executives (40 percent) say current conditions in the global economy are the same as they were six months ago. This is a slightly more positive view than three months ago,2 when the same share—and the largest—said conditions had worsened. Looking ahead, executives are more optimistic: 43 percent say they expect the global economy will be better six months from now, up 17 percentage points since last December (Exhibit 1).

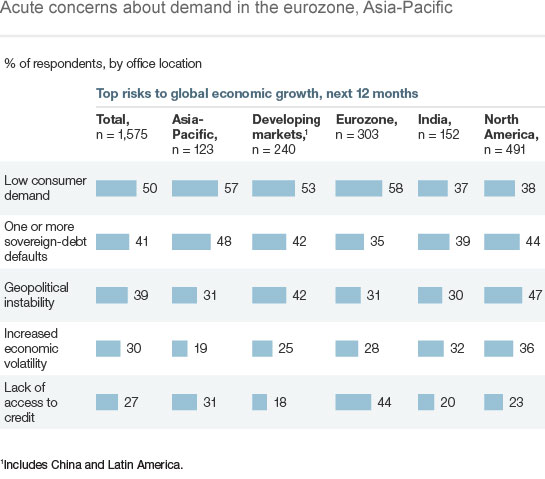

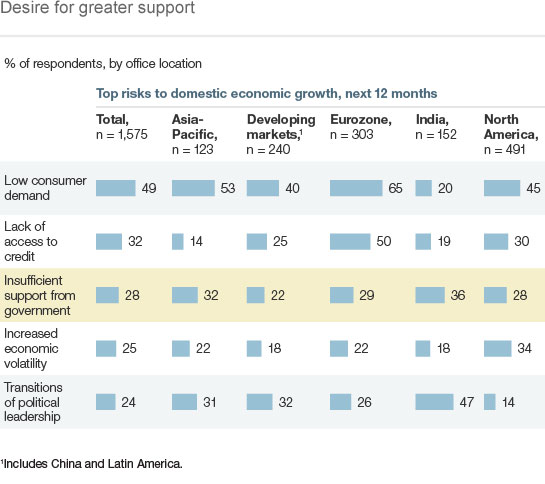

But their responses on risks to growth temper their more positive view. As in our two previous surveys, sluggish consumer demand tops the list of threats to global growth over the next 12 months, and low demand is of particular concern among executives in the eurozone and developed Asia (Exhibit 2). Those in developed Asia are also the most likely to say international demand for their countries’ products and services will increase in the next few months, with half of respondents there saying so; only 39 percent of executives in developing markets3 say the same.

When asked about the likeliest shocks to the global economy, more than 90 percent of executives expect to see geopolitical risks in the Middle East and North Africa next year—a share similar to what we observed in September. Given that this survey was fielded in early December (and coincided with the budget debate in Washington, DC), respondents also express a strong view on the US government’s budget. A larger share of respondents than in September say it’s at least somewhat likely that imminent spending cuts and tax increases will go into effect next year, citing this “fiscal cliff” as the third most likely shock of eight; three months ago, it was ranked seventh.

If these spending cuts and tax increases do go into effect, the global consensus is that US economic growth will suffer: 70 percent of all executives—and 82 percent of those in the United States—say so. But respondents in the United States are more skeptical than others that the country will go over the cliff: 21 percent of respondents there (compared with 16 percent of all respondents) say it’s not at all likely to happen.

No country-level consensus

On average, respondents have a slightly more positive view of current and future conditions in their home countries than they did in September. However, they are still inclined to say things are worse now than they were six months ago: 30 percent of executives rate conditions in their countries as better now, while 38 percent say conditions are worse.

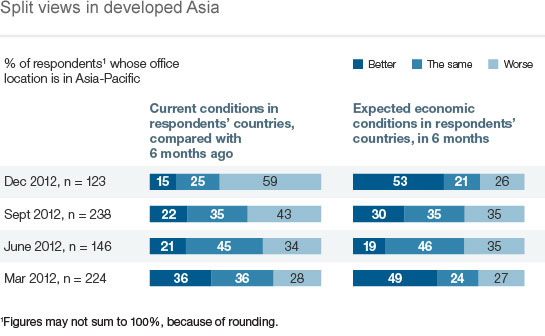

Opinions diverge across regions, and the results from developed Asia are particularly noteworthy (Exhibit 3). With 59 percent of executives there saying current conditions in their home countries are worse now than six months ago, domestic views in this region are more negative than they have been in the last few surveys. But the outlook in developed Asia is among the most optimistic: 53 percent of executives in the region say conditions in their countries will be better—more than three times the share who say current conditions have improved in the past six months. Furthermore, their expectations for the global economy are more positive than they have been all year, with 45 percent expecting conditions to improve in the next six months.

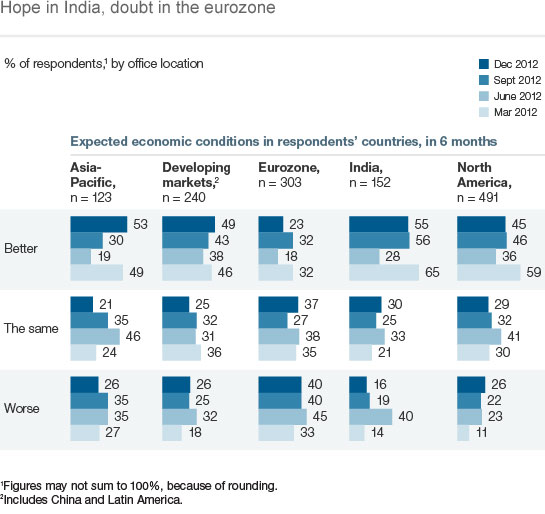

Executives in India continue to be the most positive about their country’s prospects, while those in the eurozone are still the likeliest to expect conditions will worsen—as has been the case for all of 2012 (Exhibit 4).

With respect to risks that threaten domestic growth, low consumer demand tops the list for the sixth survey in a row. A lack of fiscal or monetary policies that support economic and business activity also has emerged as a concern, especially in developed economies. In the eurozone, for example, 29 percent of executives cite insufficient support from government as a threat to growth (Exhibit 5), compared with only 19 percent who said the same in September.

Confidence in companies and emerging markets

Overall, executives maintain an optimistic view of their companies’ short-term prospects. More than half of respondents predict that company profits will increase in the next six months. And in contrast to the relatively gloomy view of demand at the global and domestic levels, a plurality of executives—for the first time since March—expect demand for their companies’ products or services to increase (Exhibit 6). Nevertheless, the results indicate little change in workforce expectations, with the largest share of executives (44 percent) predicting the size of their workforces will stay the same.

The results also indicate some renewed optimism about emerging economies. Compared with September, smaller shares of executives say they expect a sharp slowdown in China’s growth in the next year and over the next decade.4 And looking ahead to the next ten years, more respondents than in the previous survey say growth led by emerging markets is the likeliest economic outcome, while smaller shares now predict that developed and emerging markets alike will face continued slow growth, challenges such as income inequality and onerous government debt, and multiple economic shocks.5

Related Articles