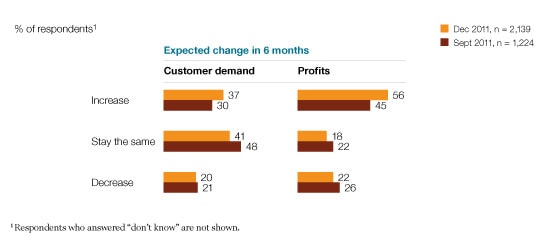

Executives’ expectations for corporate profit are on the rise. Fifty-six percent expect an increase in the next six months, up from just 45 percent in September. And although more executives are worried about low consumer demand than any other threat to economic growth, a bigger share now also expect demand for their companies’ products or services to increase over the next six months than they did in September. In spite of this hope for improvement, executives do indicate that they’re hedging their bets a bit. The share saying their companies are postponing capital investments or M&A has risen somewhat since June,1 perhaps an indication that many are waiting to see how the eurozone crisis plays out.

More broadly, executives from around the world say they are only a little more worried about several threats to economic growth, including sovereign-debt defaults,2 than they were in September. At a global level, economic expectations aren’t very different, with larger shares responding somewhat more negatively than positively. But there have been some notable regional changes, mostly for the better—even among executives in the eurozone, where the share expecting economic conditions in their countries to worsen in the next six months has fallen to 52 percent from 57 percent in September; still, their expectations have not recovered from the considerable change since June, when only 19 percent said the same.

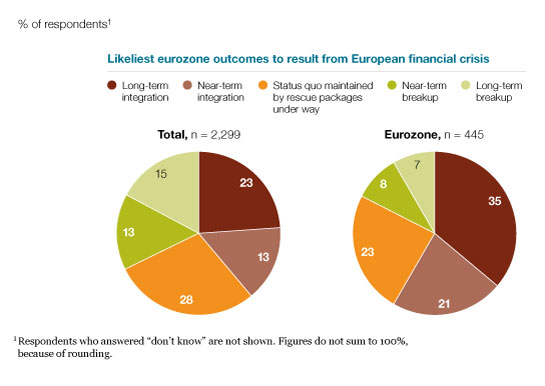

This survey was in the field in the week leading up to the December 8–9 European Union summit. The actual situation is fluid; at that time, 35 percent of respondents in the eurozone expected long-term economic integration to be the likeliest outcome of the current financial crisis, and a further 21 percent expected near-term integration. Only 15 percent of eurozone respondents, and 28 percent of all respondents globally, expected either a near-term or long-term breakup.3

Regional expectations shift

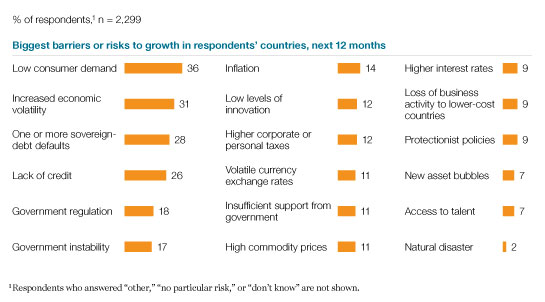

At a global level, perceptions of the top threats to economic growth have changed little in the past three months. Low consumer demand still leads the list, and the shares of respondents who selected each of the top four—demand, increased economic volatility, one or more sovereign-debt defaults, and lack of credit—have all edged up slightly since September (Exhibit 1).

However, across regions, respondents’ expectations for the global economy (Exhibit 2) and their national economies (Exhibit 3) have changed substantially since September. Respondents in the eurozone have become slightly less worried. Even larger shifts have taken place in the views of respondents in developed Asia, far more of whom now expect stability rather than improvement in their nations’ economies over the next six months—though they’re more hopeful about the global economy than they were in September. Among respondents in North America, there has been a marked swing from expecting worse to expecting better. Overall, though, respondents are still far gloomier about their countries’ prospects than they were in June, when nearly half expected their economies to improve in the next six months; now, 29 percent expect improved conditions.

Low demand threatens growth

Global expectations shift

Disparate views at the regional level

What about the euro?

Executives’ overall assessment of the role of the euro is positive: 44 percent of all respondents say that since its introduction, the euro has had a positive effect on their countries’ growth,4 and 54 percent say it has had a positive effect on the eurozone. Not surprisingly, those figures are higher among respondents in the eurozone, where just over three-quarters say the euro has had a positive effect on their countries and on the eurozone as a whole.

As for the eurozone’s future, more than half of respondents there and one-third of all respondents expect integration, as of the first week in December (Exhibit 4). Executives in the eurozone are far less likely to expect the zone to splinter: only 15 percent say so, compared with 28 percent of all respondents.

More hope for companies Executives’ expectations for customer demand and profits have risen markedly (Exhibit 5). Notably, while executives in the eurozone are less positive than those elsewhere, even they are more positive now than they were in September. It is important to note that these figures are still far below the share of positive responses in June, when, for example, 63 percent of respondents globally expected profits to rise.

Executives’ views on their companies’ current willingness to make capital investments or deals are also slightly dampened compared with June: 33 percent say their companies are postponing investments, and 24 percent say the same about M&A, compared with 28 percent and 19 percent in June, respectively.5 Notably, the figures are similar among executives in the eurozone, where 33 percent say they’re postponing investments and 27 percent say they’re postponing deals.

Europe predicts integration

Higher hopes for demand and profits