This article was originally published by CSCMP's Supply Chain Quarterly in the Quarter 3/2014 edition (www.supplychainquarterly.com) and is republished here in full with permission.

Asia is a contintent of contrasts, with huge variations in natural resources, business environments, and cultures among its many, far-flung countries. One thing that most Asian nations have in common, though, is economic growth.

Since the late 1970s, Asian economies have dramatically outpaced the rest of the world when it comes to growth in gross domestic product (GDP) per capita. Income growth has remained strong since 2000, with average annual real gains of more than 5 percent. In some Asian countries, income levels have grown at a torrid pace. Vietnam, for example, took just 11 years (from 1995 to 2006) to double its per-capita GDP from US $1,300 to $2,600. Moreover, extreme poverty is rapidly receding throughout Asia. In 2000, 14 percent of the region's population lived below the international poverty line, with incomes of US $1.25 a day or less; by 2013, that share had fallen to just 3 percent. These are some of the reasons Asia's share of the global consumption of manufactured goods is expected to rise to 58 percent by 2025.

Asia's rise in affluence is happening hand in hand with a dramatic growth in technology penetration. Consider, for example, that annual mobile phone sales in the region have grown from 150 million in 2000 to 750 million in 2012. In addition, easy access to online content regardless of location has contributed to the growth of a highly aspirational generation of discerning consumers who seek the best quality, features, and service. In particular, China has shown an insatiable appetite for online retail. The Chinese e-commerce market, which reached US $190 billion in 2012, is expected to hit $500 billion by 2015, overtaking the United States to become the new global leader in that business segment. Although India was late in allowing e-commerce players, its market is projected to grow rapidly, to over US $40 billion by 2021.

Many global companies are seeking to capitalize on the growth in Asia's emerging markets by expanding their physical presence there. Major consumer goods players like Unilever, Procter & Gamble (P&G), and L'Oréal have significantly expanded their regional offices in Asia, and a number of companies have made assignments in their Asian offices an important element of leadership development.

If they are to capture the full potential of Asia's emerging markets, companies will have to understand and account for the unique supply and demand challenges of the region. Demand in these markets is complex due to the need to provide a wide range of stock-keeping units (SKUs) covering multiple price points. It is also volatile, as channel partners often struggle to sense and forecast changing consumption patterns. Reliable supply, meanwhile, can be hard to establish because of challenges posed by infrastructure limitations, taxation policies, and a shortage of needed employee skills. In light of these conditions, many international companies are deliberately creating different business models for Asian markets. For example, consumer goods companies that are traditionally configured by product categories in Europe have adopted geography-based structures in the more heterogeneous Asia region.

The influence of diversity

Asian economies are in different stages of maturity and therefore are very diverse. For example, Indonesia is a member of the influential "Group of Twenty" (G20) countries, while Myanmar, emerging from decades of isolation, is still an underdeveloped market working to build its institutions. At US $51,000, GDP per capita in Singapore is more than 30 times higher than in Laos and more than 50 times higher than in Cambodia and Myanmar; in fact, it even surpasses that of the United States. The standard deviation in average incomes among Association of Southeast Asian Nations (ASEAN) countries is more than seven times that of European Union (EU) member states. This disparity in purchasing power means that even multinational companies need to customize their products to meet a wide range of target price points for countries within Asia, thereby increasing SKU complexity.

This diversity extends to political outlook and policy. India, for example, has historically adopted protectionist policies that have controlled business sectors and the extent to which foreign corporations can invest in the country. It still does not allow 100 percent foreign direct investment in the retail sector. As a result, while international retail chains are booming in South Korea and Japan, they still account for less than 25 percent of sales in India. Multinational companies like Amazon operate in India purely as an online marketplace for other companies' products, since they cannot set up their own warehouses or retail operations. Similarly, complex tax structures in the country mean that even local companies often have to set up multiple logistics facilities across the states.

The infrastructure differences in Asian countries have made it necessary for companies to experiment with alternate routes to market. Markets like Japan, South Korea, and Singapore, with their well-planned cities and superior infrastructure that allow for economies of scale, operate in a completely modern trade environment. In countries like India and Indonesia, by contrast, burgeoning populations, less-planned urbanization, and developing infrastructure have resulted in a largely distributed trade environment, where the majority of sales are conducted through small, family-owned "mom and pop" outlets served by multilayered distribution networks with high logistics costs. Other markets, like China, Malaysia, and Thailand, are split roughly equally between distributed and modern retail channels.

Asia's diversity extends into social, linguistic, and cultural dimensions, all of which may require careful adaptation on the part of manufacturers. Some examples: Indonesia is almost 90 percent Muslim, while the Philippines is more than 80 percent Roman Catholic, and China is more than 95 percent Buddhist. India is 80 percent Hindu, with significant and active Muslim, Sikh, and Christian minorities.

Companies need to be aware of such intraregional differences and their sensitivities. During the months of Ramadan, for instance, products that appeal to the religious sensitivities of Muslims see a big jump in sales, while capital-goods and auto manufacturers in India wait for the holiday of Diwali to launch major sales promotions. The Chinese New Year, celebrated every February, practically cripples long-distance goods movement, forcing companies to build up inventories to serve demand during the festive period. Finally, because there is no one common language that binds Asia, and English is spoken and understood in few regions, companies are forced to customize their product labeling and promotions to meet local language requirements.

Five strategies for success

Asia's continued high growth rates make it a very attractive market for global manufacturers and consumer goods companies. But the ability to take advantage of those opportunities is only available to companies that appreciate the diversity and complexity of the region. McKinsey's research indicates that there are five key challenges or issues that companies must master to succeed in Asia:

- Succeeding with "last mile" delivery

- Handling extreme consumer diversity

- Unlocking the potential of e-commerce

- Managing risk through nearshoring

- Acquiring sufficient supply chain talent

In the remainder of this article, we will discuss each of these, including strategies for addressing them.

1. "LAST MILE" DELIVERY

Plan for demographic and social trends

The McKinsey Global Institute (MGI) forecasts that by 2020 over 4 billion people will be urban dwellers worldwide, and 80 percent of them will live in developing countries.1 This new urban consumer class will spend more on housing, recreation, health care, and consumer products. This in turn will drive up demand for increasingly sophisticated supply chain capabilities, including higher customer service levels, faster delivery, improved availability, and greater agility. The MGI study also indicates that although populations in urban centers are growing six times faster than in rural ones, this expansion is not limited to first- and second-tier cities. In China, Indonesia, and India, for example, major growth is occurring in smaller cities located in remote areas. Thus, the demographic and social trends in these countries indicate that existing cities will become denser, with alternate routes to market like modern retail, traditional distributed retail, and e-commerce, while today's towns will grow into young cities.

This trend has several implications for supply chains. First, the increasing service expectations will make last-mile (final delivery) distribution far more important than it is today. For example, it is not uncommon today for an Asian "mom and pop" store to work with a 60-80 percent level of on-shelf availability, compared to 99 percent in the developed world. Achieving higher levels of service will call for sophisticated management of the last mile, including real-time tracking of orders and deliveries, and optimization of routes and vehicle loading.

Second, increased consumption in the bigger cities will finally create the scale for third-party logistics (3PL) companies that specialize in last-mile logistics. These companies will start with a few key accounts but will soon become aggregators serving multiple manufacturers and retailers in a locality. In India today there are very few large 3PLs; most logistics activities are being managed by local, unorganized transporters. This will change as cities grow and customers demand superior service that requires sophisticated capabilities.

Third, multiple routes to market within the same cities will promote different last-mile logistics models. The modern, multibrand retailers and the larger, single-brand retailers that promise shoppers better customer service will prefer to work with the more Third, multiple routes to market within the same cities will promote different last-mile logistics models. The modern, multibrand retailers and the larger, single-brand retailers that promise shoppers better customer service will prefer to work with the more professional logistics service providers. At the same time, smaller, distributed retailers with an emphasis on low prices for customers will remain cost-focused and will seek low-cost, entrepreneurial delivery models.

One such innovative (and uniquely Indian) health-care distribution model is that of the ERC Eye Care Center, which offers affordable and quality eye care through its vision centers, satellite clinics, and a hub hospital in the northeastern state of Assam and nearby areas. As part of its effort to address the current shortcomings of the eye-care system in the region, the company plans to expand via its hub-and-spoke model across Assam to offer people in underserved communities access to affordable consultations, eyeglasses, and eye surgery. Under this model, the company maintains high-volume inventory at its hubs, and stocks low-volume inventory at the "spokes" (service locations located at a distance from the hubs).

Finally, the increase in consumption in rural areas will create fresh demand centers that will be profitably served by new, indirect distribution models. These models require the manufacturer to sell to a rural distributor, who then sells to retailers spread throughout 10 to 15 villages. The small scale and remote location of these retailers requires special modes of transport and may drive the aggregation of products across manufacturers. Consumer goods companies like Unilever, ITC, and Eveready developed the first such rural distribution models in India, and these organizations continue to innovate to serve growing rural demand. Unilever, for example, employs the Shakti Amma (the literal meaning is "empowered woman") model to reach smaller villages that it cannot otherwise serve directly. The company's rural salesperson at a district level appoints women entrepreneurs called Shakti Ammas in villages. These women pick small quantities of products from the salesperson and then sell them to small retailers in their villages.

Focus on efficient logistics

The complexity of last-mile logistics in many Asian markets inevitably leads to higher costs, and these costs have been exacerbated in recent years by rising service expectations and by other factors, like increasing costs for fuel, real estate, and labor. For most industries, logistics spend as a percentage of revenue is significantly higher in Asia than in Europe or the United States.

To stop their logistics costs from eroding too much of their margins, supply chain managers need to employ optimization tools like network planning, vehicle scheduling, and route planning to squeeze out the last bit of inefficiency in logistics.

This approach can lead to significant cost improvements. One Chinese logistics service provider, for example, saved 5 percent of its transport costs by rearranging its network. With over 130 hubs and 600 line hauls across China, the company decided to apply demand forecasts by line haul rather than by the national volume and to use advanced network modeling to balance cost with service. By reviewing and adjusting its line-haul volume plans monthly, the company has managed to transform its logistics network into a major source of competitive advantage.

A multinational commodity-goods company dealing in bulk logistics managed to reduce its logistics spend by 6 to 8 percent in just two years-without any drop in service levels-by adopting lean tools and techniques typically applied in manufacturing operations to its entire outbound logistics value chain. Among the company's initiatives were efforts to minimize railcar loading time and total turnaround time for road transportation, especially minimizing waiting time at the plant and warehouse; optimizing the mix of rail and road transportation; increasing road transportation capacity through the use of larger trucks; and setting up win-win contracts with transporters that included a mix of cost and safety factors. Successful implementation of these initiatives required an intensive effort to develop capabilities among more than 50 executives and managers in the company's logistics function.

Unlock working capital in the value chain

Another key focus for Asian supply chains is the management of working capital. Working capital management-for example, through inventory optimization and the management of payables and receivables-is an integral part of every business. In Asian markets, however, it takes on added importance due to the high amount of capital trapped in the extended value chain as well as the higher cost of capital. For example, it is not unusual for the cost of capital in India to exceed 12 percent. Supply chains in Asia are inherently complex due to their proliferation of SKUs, routes to market, and consumer segments. This greater complexity and uncertainty translates to higher inventory levels, not just in the company, but also in the extended value chain, including suppliers and channel partners.

While most multinationals and larger local companies maintain good control over their working capital, their smaller suppliers and partners do not possess similar capabilities. The high rate of borrowing in most markets means that these companies often struggle to raise cash, and that becomes the rate-determining step in the growth plans of larger organizations.

Increasingly, companies are realizing this and are responding in two ways. First, they are extending their superior supply chain capabilities to their partners. This includes investing in technology and planning systems that track and optimize end-to-end inventory in the extended chain. Second, they are helping their partners secure cheaper capital from banks. Banks in Asia are taking steps to help small and medium-size enterprises (SMEs) improve their working-capital management processes and systems, so that they rely less on borrowed funds to fuel growth. For example, the banks may help companies adopt vendor-managed inventory (VMI) techniques, in which a supplier holds and manages materials and parts for its customers. Once consumed, those parts and materials are regarded as having been directly purchased.

2. CONSUMER DIVERSITY

Match the supply chain to the product portfolio

A significant implication of the diverse nature of the Asian consumer is the need for products and services offering similar functional benefits but at widely different price points. This, coupled with local entrepreneurship, has meant that different business models have evolved to deliver the products and services consumers want at the prices they want to pay. Many successful companies have used this business strategy effectively in Asian markets. For example, one consumer goods company that sells detergent powders offers one brand at US $0.50/kg and another at $2.50/kg. A car manufacturer whose most popular brand was priced at US $15,000 has launched an equally popular model at just $5,000. One more example involves the Indian watchmaker Titan, which developed its brand strategy in tune with a customer-segmentation strategy. As the company came to encompass almost every value need and price point in the mass, premium, and luxury segments of India's watch market, it created a large array of brands with a price range of less than US $20 to more than $500.

These alternate business models, often employed within the same company, are underpinned by very different supply chains. Lean supply chains support high-volume, mass-market products with a greater emphasis on value, while agile and fully flexible supply chains deliver premium products, for which service overrides cost considerations. Companies that do business in Asia need to master this supply chain segmentation to successfully compete across the entire price portfolio.

Adapt planning methods to the market

One multinational operating across Asia uses variants of a "control tower" approach as part of its sales and operations planning (S&OP) to achieve an agile supply chain. Under this model, a cross-functional group of senior personnel from various supply chain functions, such as demand, production, inventory, and logistics, work together to identify and address supply chain issues. In mature markets like South Korea and Singapore, products are segmented based on margin and working capital, and a weekly joint planning meeting with retailers is set up to ensure transparency of supply and demand. However, in growing markets like Thailand and Indonesia, where SKU proliferation is common and there is a chronic shortage of skilled planners, the company simplified planning efforts by identifying the critical SKUs that require high-accuracy planning, and then using automated planning and replenishment to handle the remaining products.

Furthermore, in Southeast Asia, where each country market is relatively small, this company achieves economies of scale through regional production that is supported by both regional- and national-level planning and in-country control towers. This allows the company to achieve 96 percent product availability for modern retailers in North Asia while at the same time reducing inventory by 40 percent in Southeast Asia-without impacting lead times or serviceability.

A similar segmentation of SKUs by an auto-component provider in India, using the control tower approach to track shifting product demand in the face of a volatile market and material shortages, saw its "on-time in-full" levels increase from 68 percent to 82 percent without any increase in its inventory levels.

3. E-COMMERCE

Understand trends in emerging markets

Since the 2000s, delivery models that have had a tremendous impact on supply chains in Asia have emerged. The explosive rise of electronic commerce (e-commerce), for example, has transformed the Internet from a source of information about products and services to a way to buy them. While such channels are already considered an important aspect of doing business in developed economies, digital business-to-consumer (B2C) markets are also starting to boom across Asia's still maturing economies as Internet penetration grows.

But what really distinguishes Asian e-commerce sales is the customer's willingness to pay for convenience in light of Asia's infrastructure challenges. A McKinsey survey showed that more than 65 percent of respondents in India and 40 percent in China were willing to pay extra for convenience, compared to just 17 percent in the United States.2

Around 26 percent of Internet users in Asia in the 25-30-year age cohort use the Internet to buy products, and this is expected to grow to 60 percent by 2025. Consumers in Asia increasingly are accessing the Internet using new tools like mobile phones and tablet computers, and a growing number are relying on social media to make informed buying decisions. Not just dedicated e-retailers, but also traditional bricks-and-mortar retailers are embracing electronic commerce as a critical component of their emerging-market business operations. Such multichannel approaches for the delivery of products, along with the proliferation of SKUs discussed above, is forcing supply chain managers to adopt new and innovative strategies for product delivery in Asia.

The biggest challenge in establishing an e-commerce channel remains the management of the "back end" supply chain. For many e-businesses this is unusually complex due to the higher number of SKUs and suppliers the retailer needs to manage. The reliability and flexibility of these suppliers has not grown at the same rate as the demand, so e-commerce retailers often need to adopt more robust supply management practices than do traditional retailers.

Adopt innovative service strategies

Homeplus, a Tesco joint-venture company in South Korea, launched virtual stores in Seoul subway stations, using e-commerce to overcome a rival's greater physical presence. The walls of the Seonreung subway station in downtown Seoul came to life with virtual displays of more than 500 of the most popular products. The images incorporated bar codes, which customers could scan using an app on their smartphones to request delivery to their doorsteps. The new business was successful, as the virtual stores created fresh demand that was fulfilled by the company's already well-established supply chain. This success story prompted a Chinese online retailer to launch its first virtual stores in Shanghai.

Other companies are using their e-commerce channels not just to deliver products, but also to enhance the service offered by their conventional sales channels. For example, an Asian motorcycle manufacturer allows customers to select customization features like seating options and accessories online. This information is sent to dealers, who fit the appropriate parts so that the customers can collect ready-to-ride customized motorcycles after a very short delivery lead time.

4. MITIGATING RISK

Embrace nearshoring

Nearshoring refers to increasing the proximity of tangible (for example, manufacturing) and intangible (such as innovation) aspects of businesses relative to end-consumer demand. Nowhere has this been more relevant in the last decade than in Asian markets.

Most multinational companies began their Asian businesses by viewing these markets as geographical extensions for brands they were selling in the developed world. Their first business models therefore involved establishing routes to markets in Asia and selling products manufactured in North America or Europe. These models very soon changed to nearshoring of manufacturing and procurement, which has helped companies tap into market potential, reduce costs, and enhance agility.

The emergence of state-developed special industrial zones, such as those in China, Indonesia, Johor Bahru in Malaysia, and Gujarat and Uttarakhand in India, coupled with locally available raw materials and skilled manpower, made a ready case for the nearshoring of manufacturing. For example, in the first six months of 2012, the motorcycle manufacturer Harley-Davidson's retail sales were up 16.5 percent in the Asia-Pacific region. The company recently decided to open a manufacturing plant in India, its first outside the United States. Increasingly, manufacturers are encouraging their engineering and equipment vendors to establish factories and technical-support facilities near their manufacturing plants in Asia.

The more advanced companies are now taking the next step in the nearshoring process, with a focus on the intangible assets of knowledge and talent. In order to better understand Asian consumers and be able to offer products and services that are specifically developed for them, many companies are setting up consumer research centers, product research and development (R&D) centers, and leadership training institutes in Asia. One British company has recently established a management development center in Singapore-only its second such center, and notable for the fact that it is located outside Europe. This state-of-the-art center, which has a higher capacity utilization than its European counterpart, will be used for training and development of the company's Asian staff. And a German company has established its latest global R&D center in India with the brief to develop mass-market products for the world.

Adopt global risk management practices

It is generally recognized by supply chain managers that risk in their supply chains has greatly increased over the past few years due to shrinking economic cycles, increased geopolitical turmoil in developing countries, and unpredictable natural disasters. For example, floods in Thailand in 2012 caused havoc with the supply chain of Japanese high-tech and electronics companies with a manufacturing footprint in Southeast Asia. Automotive original equipment manufacturers (OEMs) in India witnessed up to a 50 percent drop in sales volumes in 2013, with some segments recording up to eight consecutive quarters of declining volumes due to the prevailing economic uncertainty.

A survey of supply chain professionals conducted by McKinsey & Company at an automotive conference in India in 2013 found that responding quickly to supply chain disruptions was the topmost priority for organizations in the next five years. (See Figure 1.)

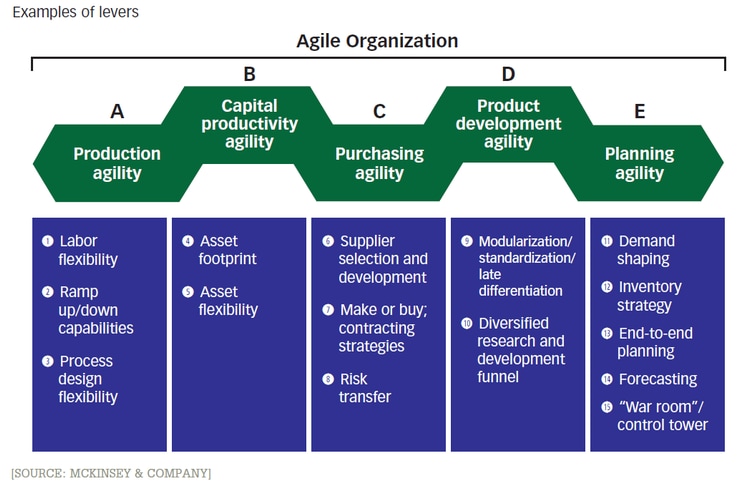

Achieving that objective would require a cross-organization approach that includes pre-empting "shocks" by reducing variability and building structural agility, detecting such shocks early through appropriate trigger points, responding in real time through predefined playbooks with clearly defined responsibilities, and capturing advantage. (See Figure 2 for a more detailed look at successful approaches to building agility across functions.)

Several companies in Asia have already adopted these models. For example, Honda has standardized its processes across all auto models and speeded its reactions to changes in the mix of models ordered by dealers, while P&G has implemented systems and developed the necessary infrastructure to ensure quick responses to changes in market conditions.

5. THE TALENT SHORTAGE

Find creative ways to fill the gap

Supply chain talent in Asia remains a scarce commodity. A Towers Watson talent management survey, which encompassed Asia-Pacific, North America, Latin America, and Europe, the Middle East, and Africa (EMEA), for example, found that demand for specific supply chain expertise is growing faster than talent development.3 In India, for example, human resources managers and employment consultants expect demand for warehouse managers to grow by more than 60 percent between 2013 and 2017, outstripping the supply of talent available to fill these positions.

As demand continues to boom, the education system in Asia is struggling to keep up. Even in India, which boasts of a high quality of education in traditional fields such as medicine, engineering, business administration, and law, there are very few institutions that offer a specialization in supply chain management. According to research by the Southern Alberta Institute of Technology in Canada, western countries are producing 50 percent more supply chain graduates per capita than is India.4

Companies are addressing this mismatch between demand and supply of supply chain professionals in creative ways. Some are training manufacturing or finance professionals who have some operating experience in logistics or are planning to take leadership positions in the supply chain function. Others are setting up "knowledge partnerships" with academic institutions to teach students how to solve problems and learn best practices. Many companies are developing strong job propositions, including an attractive career path, early leadership experience, and cross-functional exposure to woo the scarce talent available at campus recruiting events.

Multinational companies have the advantage of an additional lever to help them solve the talent problem: international transfers. Well into the first decade of the 21st century, companies in China were still hiring large numbers of managers from the United States (23 percent) and Western Europe (12 percent).5 The situation is little better today: Expatriates are leading the supply chain functions at most multinational consumer goods companies in Indonesia, for example, suggesting that there is a critical need throughout Asia to proactively address this issue. One way to do that might be the use of public-private partnerships that can help educate, train, and deploy graduate supply chain professionals.

Success requires an Asia-specific model

Asia has long been a fascinating land of contrasts, from the more developed North Asia cluster to vibrant Southeast Asia to the culturally complex South Asian countries. Economic disparity, demographic and cultural differences, lower consumption rates, poor infrastructure, and complex laws traditionally have made it hard to transplant successful American and European supply chain models here.

Asia is today at a tipping point, where growing economies, rising affluence, increasing consumer awareness, and aspirational lifestyles are driving a steep increase in the consumption of branded goods and services. Global companies with ambitious business plans will almost certainly find that a disproportionate share of their desired growth will come from Asian markets. However, the challenges of consumer diversity and supply chain complexity still remain, making business in Asia both an exciting and daunting prospect. The companies best able to take on these challenges will be those that focus on the five areas described in this article, and by doing so turn their Asian supply chains from a costly burden to a source of competitive advantage.

About the authors: Sumit Dutta is an expert principal in McKinsey's Mumbai office, K. Ganesh is a senior knowledge expert in the Chennai office, Pankaj Gupta is a senior expert in the Delhi office, Mads Lauritzen is an expert principal in the Bangkok office, and Greg Otte is an alumnus.