Understanding supplier's costs is a powerful lever in procurement negotiations.

Should-cost analysis proves its worth by helping companies reduce what their supplies actually cost.

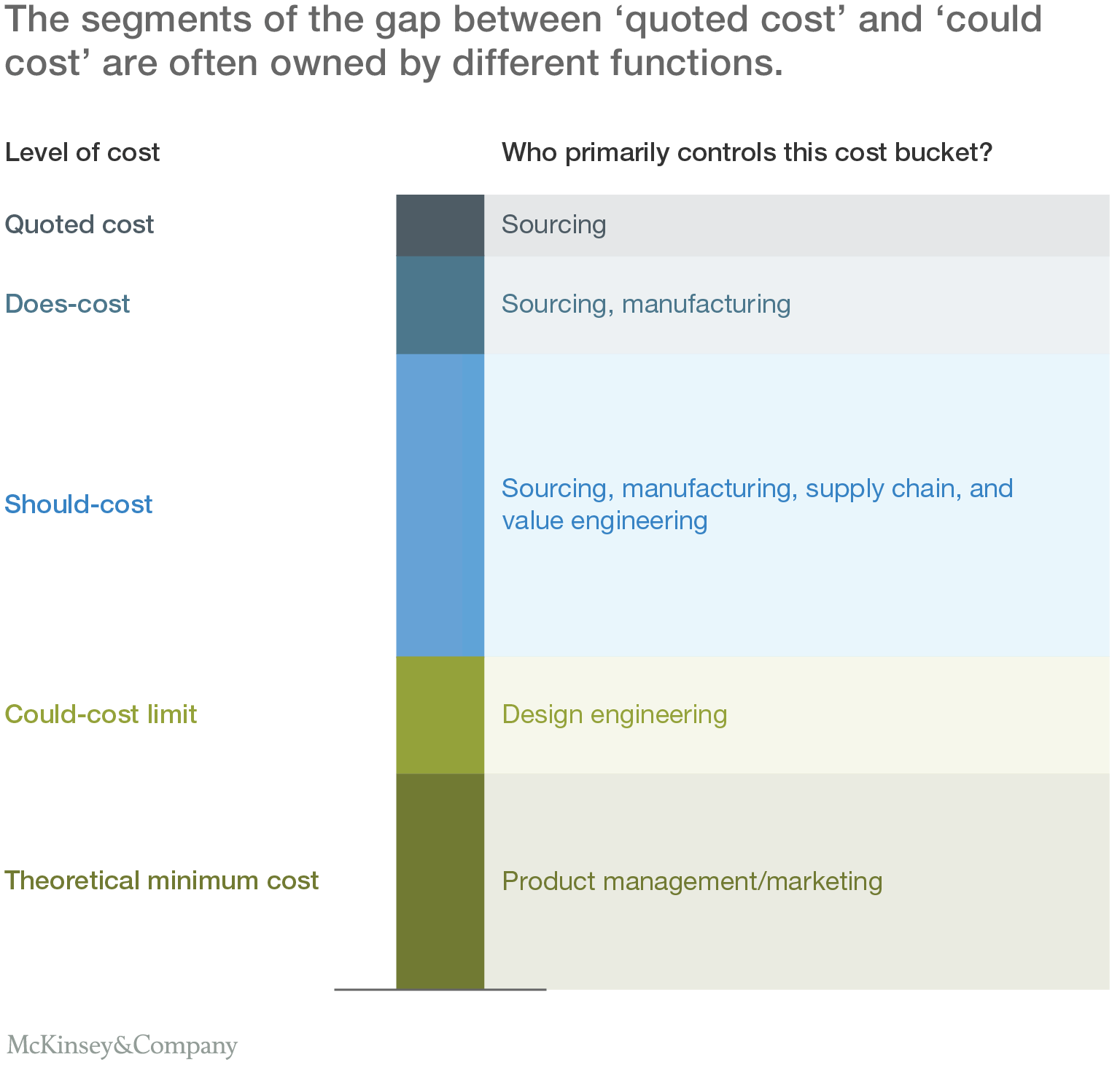

As discussed in the previous article in this series, to chip away at the costs that make a supplier's price higher than the price calculated under a detailed cost model (such as a Cleansheet), companies first need to understand the nature of those costs. We broke the gap between the two prices into three major classifications: does-cost, should-cost, and could-cost. That step made the problem more tractable by revealing the different sources of cost, which require differing strategies to address them.

Who owns the problem?

The short answer is that almost everyone in the value stream does: manufacturing, sourcing, supply chain, design. However, different parts of the gap are often primarily owned by different functions. These groups therefore should be tasked (and enabled) to lead projects that capture savings in each of their respective segments.

For example, to find savings in the should- to could-cost segment (light blue), there may be short-term, simple design changes that the value engineering team can bring to the table (Exhibit 1). Each lead function will likely solicit assistance and participation from other functions as well: the changes value engineering proposes may spark further savings proposals from manufacturing or supply chain.

How to close the gap from does-cost to could-cost…

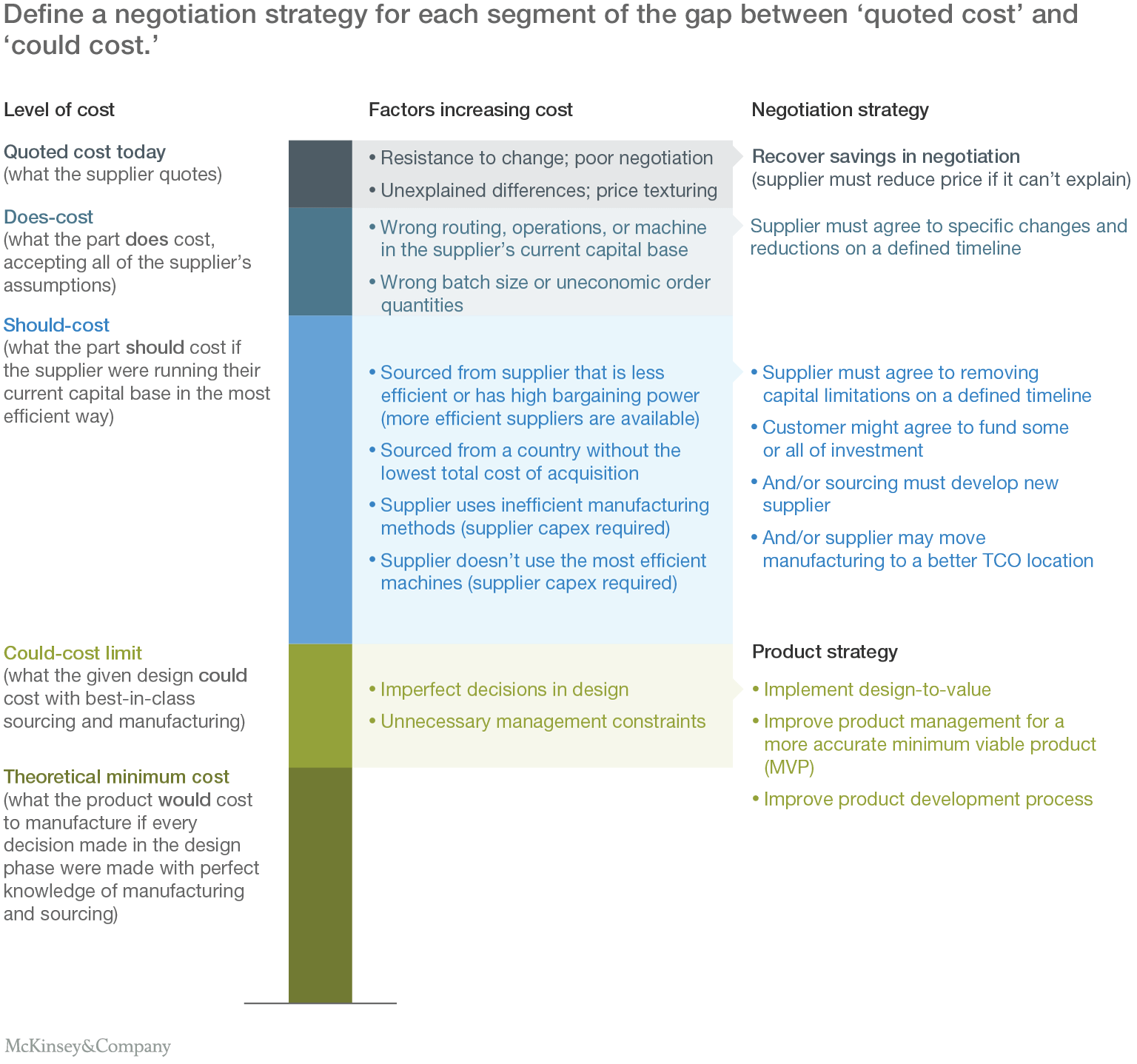

We believe it is possible to mine savings from each segment of the gap, but the timing and strategy varies depending on the cost threshold where the savings lie.

The dark-blue segment from quoted- to does-cost (reflecting the price today, calculated with a model that uses all the supplier's stated assumptions) often represents what the sourcing team is expected to recover in current negotiations. One might think that the gap would be small or non-existent, but that is not our experience. There is little reason not to secure these savings immediately, unless the supplier has strong situational leverage in the short or medium term. After all, the product cost-management team has costed the part or service using the supplier's own assumptions.

Getting supplier to provide meaningful transparency into their cost structure is no easy endeavor, requiring resilience across the buying organization for the time and effort it usually takes. One of the more effective techniques for uncovering the supplier's does-cost threshold is to incorporate credible best-in-class assumptions (grounded in real-life data) into the conversation, thereby shifting the burden to the supplier to justify its costs. The sourcing team can be quite rational and reasonable about the exercise, saying to the supplier: "If you don't agree with our assumptions, give us better ones. Show us how they're credible and we'll put them in our model."

This is not to suggest that the sourcing team should blindly accept the supplier's assumptions. In fact, we suggest the exact opposite. Many supplier-provided assumptions can be quickly checked against market information. If there is a still a gap to the supplier's assumptions, the supplier should reduce its price—unless it can provide a compelling reason, such as a category of cost that the buyer's model omits. The buyer team should insist that the supplier subtract any part of the cost difference that lacks such an explanation.

When the supplier has the upper hand

There is one caveat to this process: high supplier power. If the supplier (which in some cases could be an internal manufacturing plant) is the only short-term option, it may be able to insist on a price well above the does-cost. Accordingly, for critical supply needs and in high-spend categories, sourcing teams should invest heavily in exploring creative options for strengthening the buyer's leverage so that it can prevent being captive to the suppliers' price. This effort often generates a strong business case for developing new suppliers if the current incumbent doesn't yield—or for the manufacturing team to conduct a thorough make-buy assessment.

Timing the savings

One of the biggest mistakes we have seen companies make is to negotiate only for the savings they can get today. That leaves them winning back only the dark-blue segment. Alternatively, they might set out a set of generic "glide-path" reduction targets for the future—a blunt instrument that either unfairly punishes the supplier or leaves savings on the table.

The better practice is for the company and supplier to work together to identify the specific barriers (which sometimes are the buyer's own behaviors) between each cost threshold, and estimate the time and investment needed to cross each.

For example, the parties can typically close much of the medium-blue gap between the does- and should-cost thresholds through relatively inexpensive, short-term actions in the supplier's product-design, supply-chain, and manufacturing activities. Once agreed to, these actions should be specified in the contract on a defined timeline, with automatic savings deducted on the due date, unless the parties agree to an extension. (Exhibit 2).

Finding the right questions to ask

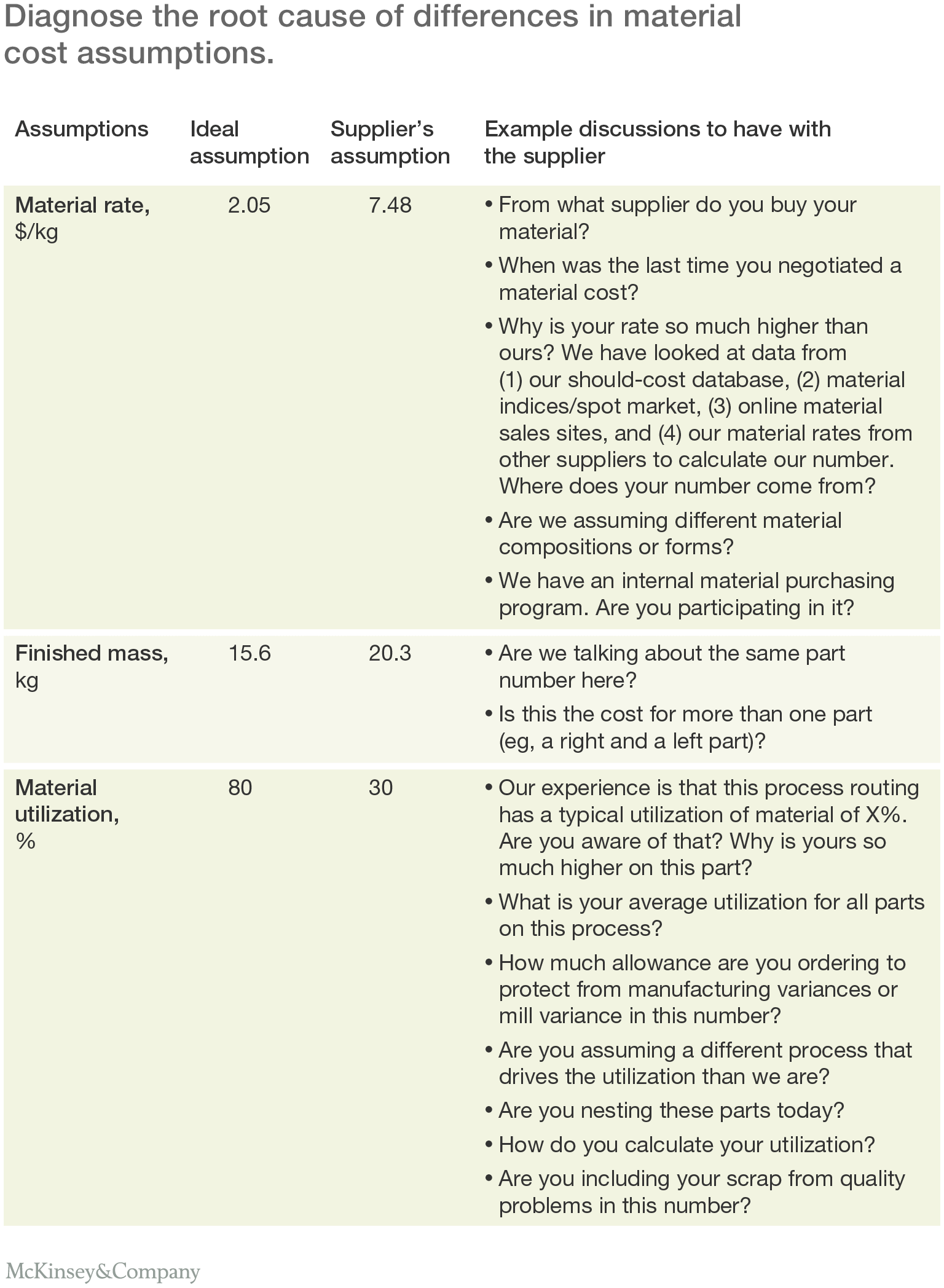

Raw material costs can be a good starting point. They usually offer a high recovery percentage because raw materials are typically purchased from a supplier further upstream, making negotiations somewhat less contentious than on other cost issues. But capturing these savings still takes some planning.

The cost estimates for raw materials are typically based on a few simple metrics, such as the cost of the base material, the mass required in the finished part, and the material utilization rate. Comparing ideal cost assumptions about these metrics with the supplier's assumptions can reveal important differences. Exhibit 3 shows a non-exhaustive list of the kinds of questions teams would ask their suppliers to diagnose the root causes of those differences.

…and from should-cost to could-cost

The should-cost to could-cost gap (in light blue on Exhibits 1 and 2) often holds bigger potential but will take longer, often requiring capital investment on the part of the buyer or the supplier. However, it should be handled in the same basic way as the short-term does- to should-cost gap. Let's examine two common longer-term supplier limitations:

- Inadequate capital investment. Perhaps the supplier does not have the most modern and productive capital equipment for meeting the buyer's should-cost. Even when the supplier is willing to invest the capital, doing so will take time. The timeline and reduced price should be explicitly specified in the contract.

- High negotiating leverage. When the supplier has intellectual property or a market position that gives it power to impose prices far above the should-cost, the only practical way to make progress is usually for the buyer to investigate new supplier possibilities. This will involve switching costs, such as engineering recertification, but these challenges can be overcome and should not deter the buyer if the business case is strong. This activity should also be communicated to the current supplier to give it an opportunity to come back to the table and prevent needless losses on either side. (When intellectual property plays a role in the supplier's leverage, it's especially important to consider scenarios and think through contract provisions that could restrict or mitigate the supplier's power—deal terms that should be negotiated strategically.)

When a party is unwilling

It may be that either the buyer or supplier is unwilling to take the actions to close the gap. If this is because of the supplier, the buyer sourcing team can start to investigate a new supplier, which is often a longer-term action. Or, the buyer and supplier may agree that they will leave part of the gap untapped—but at least everyone is aware why.

Once the team has contractually committed to take actions that account for most of the quoted- to could-cost gap, no further savings are usually possible with current technology unless the design itself changes. As noted above in Exhibit 2, the engineering team and other can undertake design-to-value activities within the current set of requirements. In addition, product management may take a harder look at what is really needed to meet customer expectations.

Executives should be aware that not every buyer will have the training or experience to ask questions of this type. Such questions are often essential for a profitable discussion, however. There are several ways to address this challenge:

- Ensure the negotiation team includes a product cost management expert

- Train the purchasing team on manufacturing or services processes and their cost drivers, and encourage them and gain experience over time

- Hire buyers with a strong technical background

- Coordinate negotiation preparation and strategy across functions, including the purchasing team, engineers, product cost experts, and finance

Next up and questions to consider

In the final article in this series, we'll look in more detail at the how the price of a product or service evolves over time, when managed correctly.

We'll conclude this one with some questions teams should ask themselves about their own ability to close the gap in supplier negotiations:

- Has the team documented its starting assumptions in the (Cleansheet) model for each sub-category of cost (material, each process, labor, etc.)?

- Has the supplier shared its underlying assumptions from its quote so that the buyer can input the data into the cost model?

- Has the team prepared for a root-cause analysis of the differences between the Cleansheet could-cost and the quoted cost?

- Have the team and the supplier analyzed the gap according to time horizons, separating the savings that can be recovered immediately from those that can only be recovered in future years?

- Have future-year savings been incorporated into the supplier contract and into internal action plans for the buyer team?

- Has a cadence of meetings for future cost review been set up?

- Has the team discussed actions to deal with limitations and excesses that can't be addressed in the near term, such as developing new suppliers or installing new equipment?

About the authors: Eric Arno Hiller is an expert in McKinsey's Chicago office and Milan Prilepok is a senior expert in the New York office.