Should-cost is a simple idea, but it's crucial to get the details right. Here's where to focus.

Should-cost can seem easy to explain, but the devil is in the details—especially the assumptions that underlie should-cost calculations.

How much should you pay for a product, component, or service? The supplier's quote tells us the price, which we hope is tied closely to the total cost of developing that item, manufacturing it, and delivering it to us. But is it? The short answer is: it depends.

For decades, cost experts have talked about a concept called "should-cost." People will loosely define this as what it really costs to design, manufacture, and deliver something, plus a reasonable profit. Should-cost is typically compared with the price quote, which is simply the price being paid today, or offered by a supplier in negotiations. There's almost always gap, which most companies want to close for the things they buy.

The definition of Should-cost includes some important assumptions, however, which a company must understand if the approach is to be useful.

What's in the should-cost?

Although should-cost seems simple, anyone who has ever been in a should-cost discussion with a supplier will tell you that the concept is far more complex because of one word: assumptions. Should-cost calculations inevitably depend on numerous assumptions, both physical (such as the machines used in fabrication, the number of workers on the assembly line, the cycle time to process, or the set-up time for a batch) and financial (such as material cost, labor rates, overhead rates, profit, and payment terms). In many ways, the final cost number does not matter as much as the assumptions behind it, since those assumptions determine both the gap between should-cost and quoted prices, and the opportunities to close that gap.

Where are we now?

Cost may change significantly over the product's development timeline from planning through to concept design, detail design, quoting, manufacturing planning, sourcing, and production.

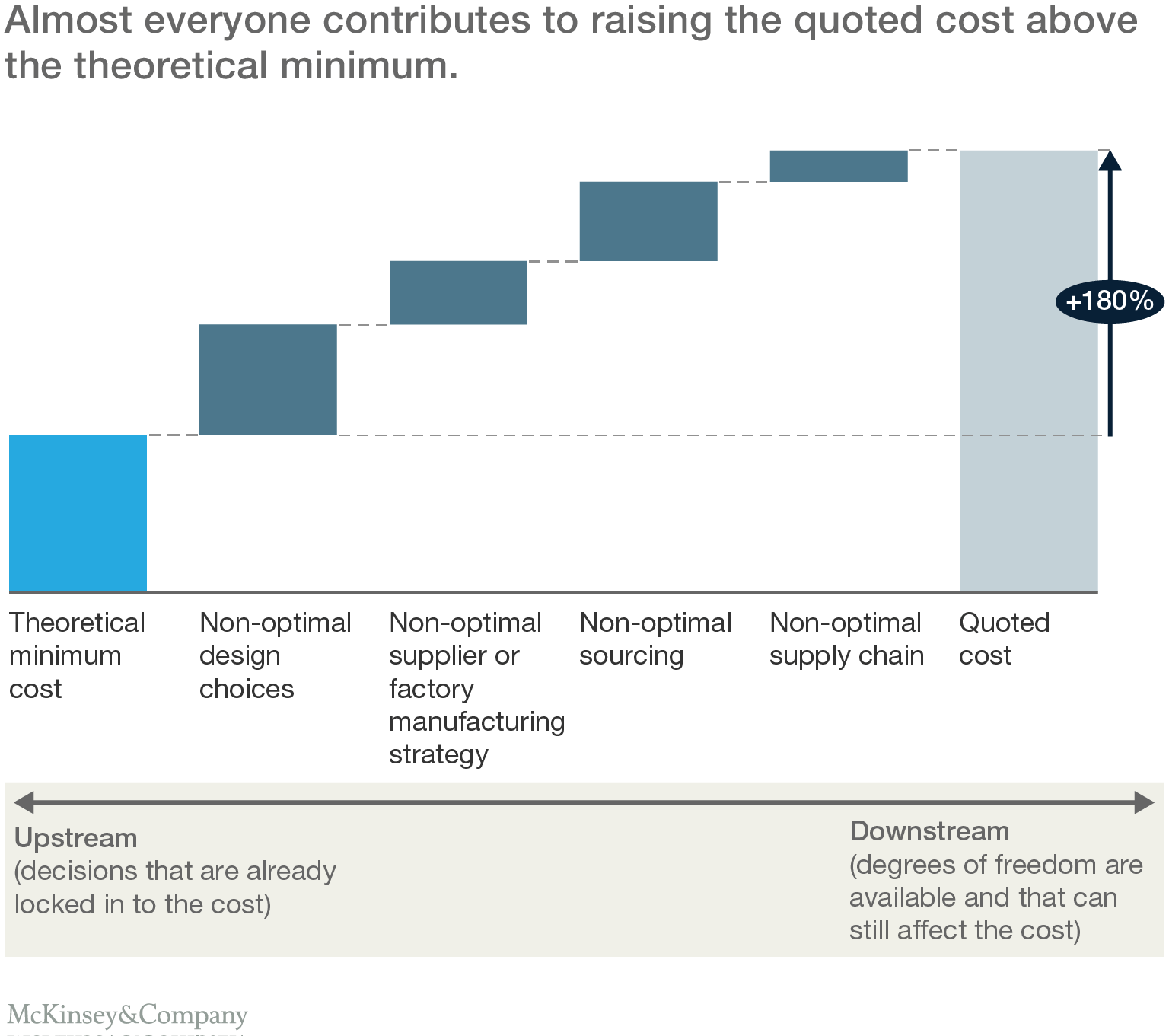

The further down this timeline you go, the more you have to accept decisions that have already been made about the product, whether those decisions were optimal or not. That leads to another important concept: theoretical minimum cost. This is the lowest cost at which a product or service with a given value or set of attributes (performance, quality, weight, features) could be delivered to the customer, if optimal decisions were made throughout the development lifecycle using the best current technology.

Exhibit 1 shows the journey from theoretical minimum cost to the final quoted cost or internal factory cost of a product. If every decision in the development process were optimal, these two costs would be the same. In reality, however, as soon as development begins, the actual cost starts to diverge from the theoretical minimum.

- Every function involved in the development process plays a part in this divergence, at every timeline stage.

- Planning decides to offer a hybrid-electric powertrain when a gasoline direct-injection engine would have met the customer's target fuel economy at lower cost.

- Engineering, in the concept design stage, decides to use a complex casting when two welded sheet-metal parts would have accomplished the same function at lower cost.

- Engineering, in the detailed design stage, specifies tolerances that are higher than necessary to meet the part's functional and assembly requirements.

- Purchasing requests a non-lean delivery process, so the supplier must increase its quoted price to preserve a fair profit margin.

- A service company engages a subcontractor when hiring internal resources would have been more cost-effective.

- A product company sources from a low-cost-country supplier without considering the total cost of acquisition (including for shipping, tariffs, communications, management), when a local or near-shore supplier would have been less expensive.

- The supplier's supply chain team uses warehouses that are distant from end customers, raising inventory costs.

The development team's constant job is to minimize suboptimal decisions like these, wherever and whenever they occur. A particular problem is that companies often think about should-cost only after the design is frozen—but this is a short-term perspective. Even though supply chain, sourcing, and manufacturing have pressing work to get the current design to the customer, design should still continue to be involved, to identify where they can implement changes, even if those changes have to wait for the next design cycle.

As companies make their should-cost calculations, they should think carefully about which decisions in the development process are upstream (frozen for the time being) verses downstream (actionable). In the light of this knowledge, they should also consider optimal timing for these decisions in future product cycles. And, rather than assuming a percentage reduction of a previous quote or invoice, they should base their decisions on detailed, bottom-up cost calculations, such as through a Cleansheet costing process (more on that in the next article).

What's reasonable?

Another area that can lead to confusion is the difference between a reasonable, best-in-class should-cost and one created using unreasonable assumptions.

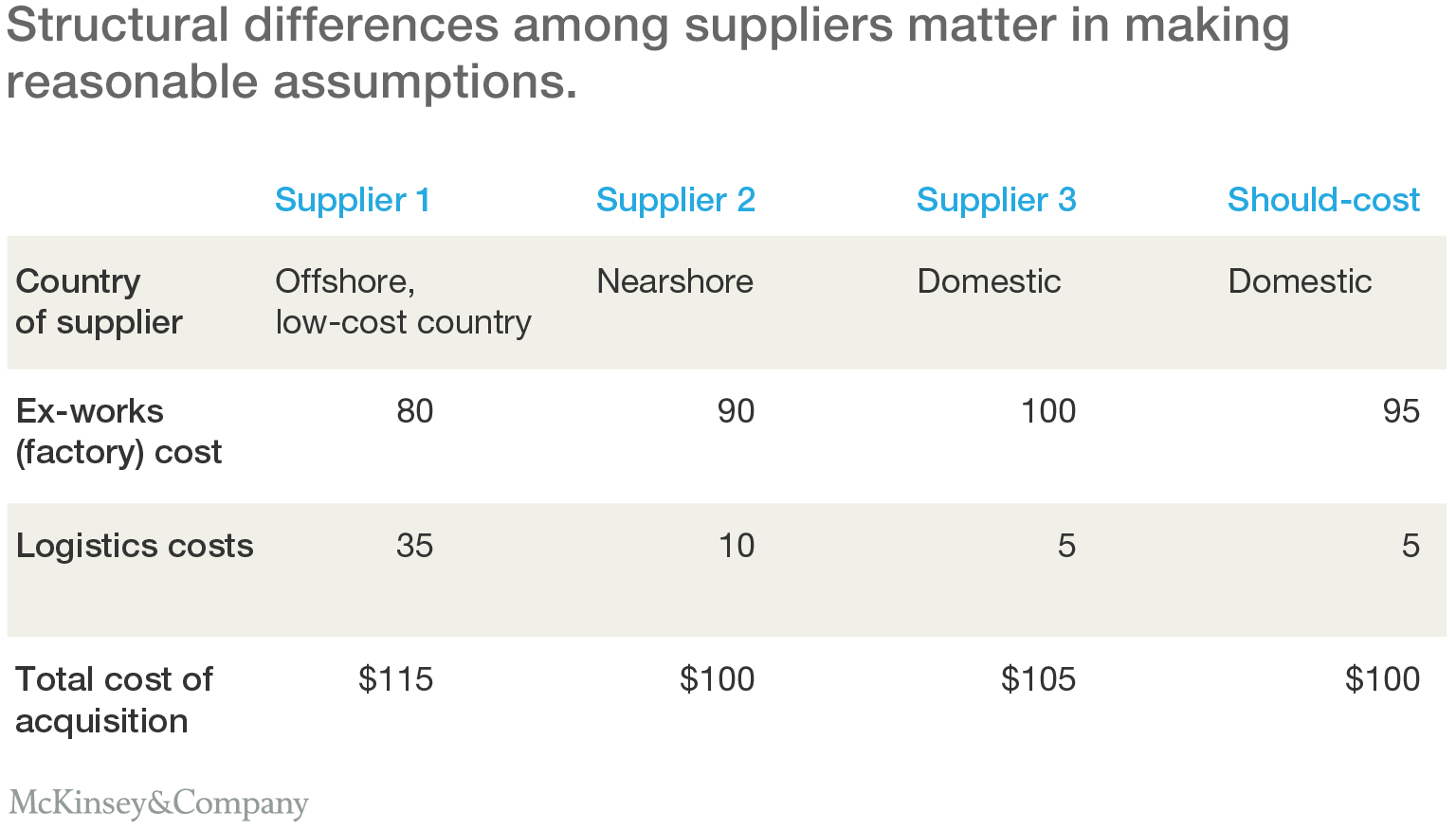

It is difficult to give a definition of what is a "reasonable" assumption in every case, but Exhibit 2 shows an example illustrating three suppliers with a simplified total cost of acquisition.

Assuming that the domestic Supplier 3 has equally or more productive equipment than Supplier 1, it would be unreasonable to expect it to match the ex-works cost of Supplier 1, which has a lower-cost overseas labor rate, or to expect Supplier 3 to produce overseas, but maintain a $5 logistics cost. However, it would be reasonable to expect Supplier 3 to match an ex-works Should-cost of $95, calculated using its own assumptions. Other potentially unreasonable assumptions include:

- Cherry-picking structural costs (labor rate, government tax structure, shipping costs) from different regions of the world, and applying them to the region in which the supplier is based

- Assuming technology that is not proven, implementation-ready, or commonly available.

- Expecting a supplier to make a capital investment in technology, without being willing to pay a fair share of that cost, or to allow any increase in the direct overhead rate to amortize the investment.

"Reasonable," however, does not mean lax. Should-costs should use best-in-class assumptions for non-structural items, such as available technology, labor efficiency and raw material costs.

The past is no guide

In some companies, a significant barrier to understanding should-cost is a culture that assumes future prices will be based on market quotes or historical costs. In these organizations, the bottom-up calculation of should-cost is treated almost as an academic exercise, without basis in reality. Management may need to lead a mind-set shift to help people see the should-cost as a real target that is achievable over time, even if it cannot be matched fully in the current cycle.

Teams can get started by thinking through a few basic questions that assess their own attitudes and approach to should-cost:

- At what stage of the development cycle are we?

- What are the decisions we have already made (or will be forced to make) that will drive the product or service cost the furthest above theoretical minimal cost? Can we change any of those decisions?

- Do our assumptions for should-cost cost reflect all the degrees of freedom that are still available downstream

- What can be done immediately to affect the cost, and what ideas should instead become assignments for the next development cycle or production cycle when changes have been made in the supplier factory?

- Are the assumptions from which we calculate should-cost reasonable?

- Are the assumptions from which we calculate should-cost best-in-class?

- Do we take should-cost modelling and calculation seriously enough? Or do we view past costs or current quotes as the only valid cost?

* * *

In later instalments, we'll look at the various contributors to the gap between what a product should cost and what suppliers quote; we'll explain how companies can use their understanding of those contributors during initial supplier negotiations; and how they can go on using that knowledge to drive further savings over time.

About the authors: Eric Arno Hiller is an expert in McKinsey’s Chicago office.