The best product cost-management programs build detailed plans for future progress.

The real value of product cost management comes when companies build on their initial savings over time for continuous cost improvement.

Now that we've examined what a product or service should cost, why the quoted price is often so much higher, and how to start closing the gap, we can turn to the final question: how to keep chipping away at cost and turn initial success into long-term value.

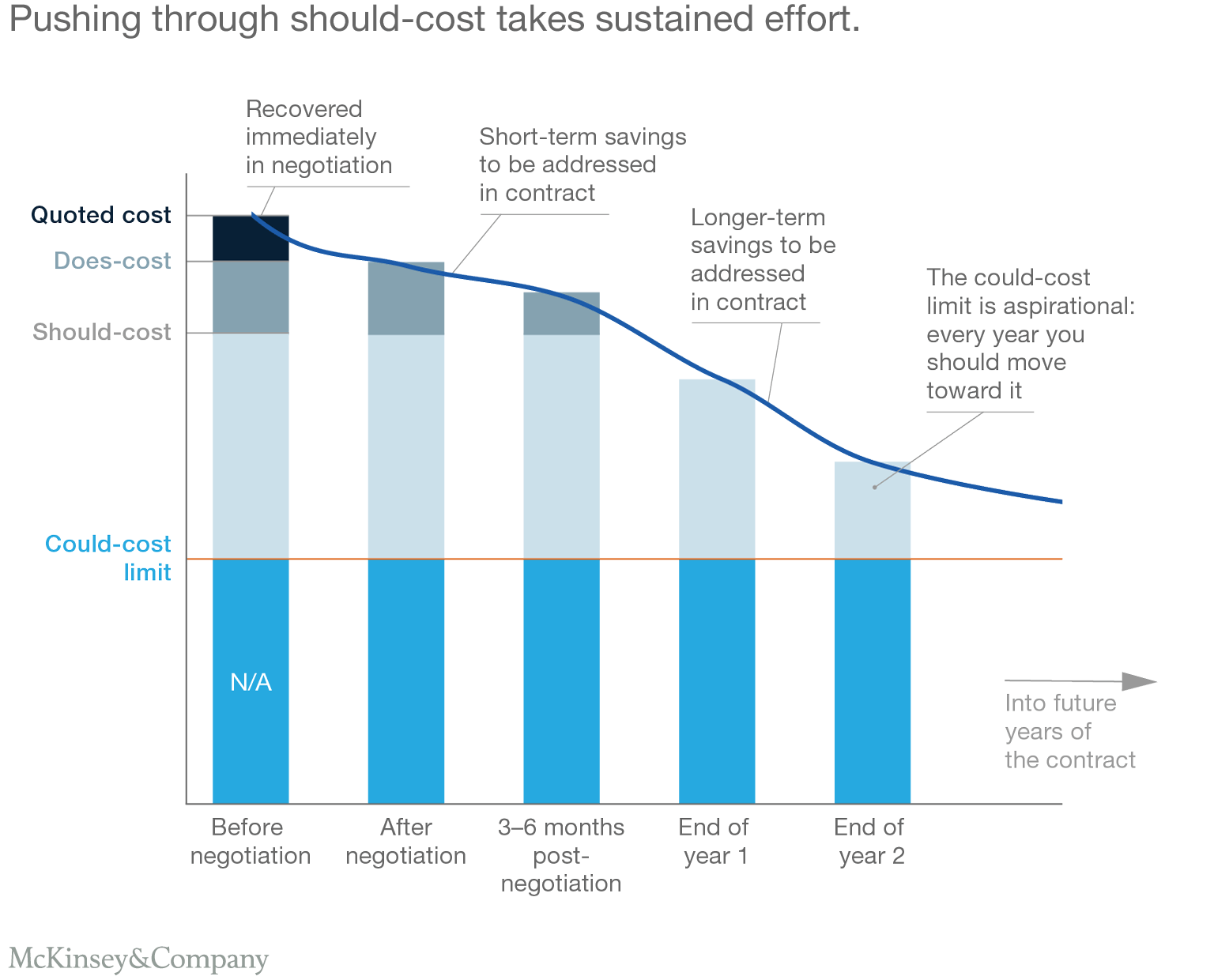

The vertical axis in Exhibit 1 shows the segments of a part's cost, calculated using Cleansheet analysis. Before negotiation, in the column at left, the calculated could-cost (the bright-blue segment) shows the minimum cost that can be achieved without major redesign or feature changes. The light-blue segment, representing the should- to could-cost gap, shows limitations that require substantial longer-term action to correct, often involving capital investment or new-supplier development. The grey does- to should-cost segment comprises smaller changes that can be done in the medium term. Finally, the black segment (quoted to does-cost) is what the team should be able to recover immediately in negotiation.

The horizontal axis shows the progress that's possible over time. But the reductions won't happen by themselves. Instead, the team should incorporate a review process into the contract's terms, setting up a defined cadence for assessing each of the segments that comprise the total gap. So, for example, after the review at the end of year one, the supplier and OEM should agree on a new does-cost for year two, with contract revisions spelling out the specific actions by the supplier and the customer in order to further analyze the gap and find additional cost-reduction opportunities.

This process is the reason that Exhibit 1 shows the light-blue bar starting to shrink after one year. We assume that by this time, that parties are able to take cost-reduction actions that weren't feasible when the initial negotiation took place. Examples might include the supplier installing new production equipment, or the customer's development of alternative sources of supply. Steps such as these gradually close the gap between quoted and could-cost. Yet it remains likely that the two will never meet. What matters more over the long run is that that the purchasing team develops a deeper understanding of the size and the causes of the remaining cost gap. It will also have a better idea of which of those root causes are addressable, helping to focus future efforts on the largest remaining savings opportunities.

The Cleansheet product cost management process in action

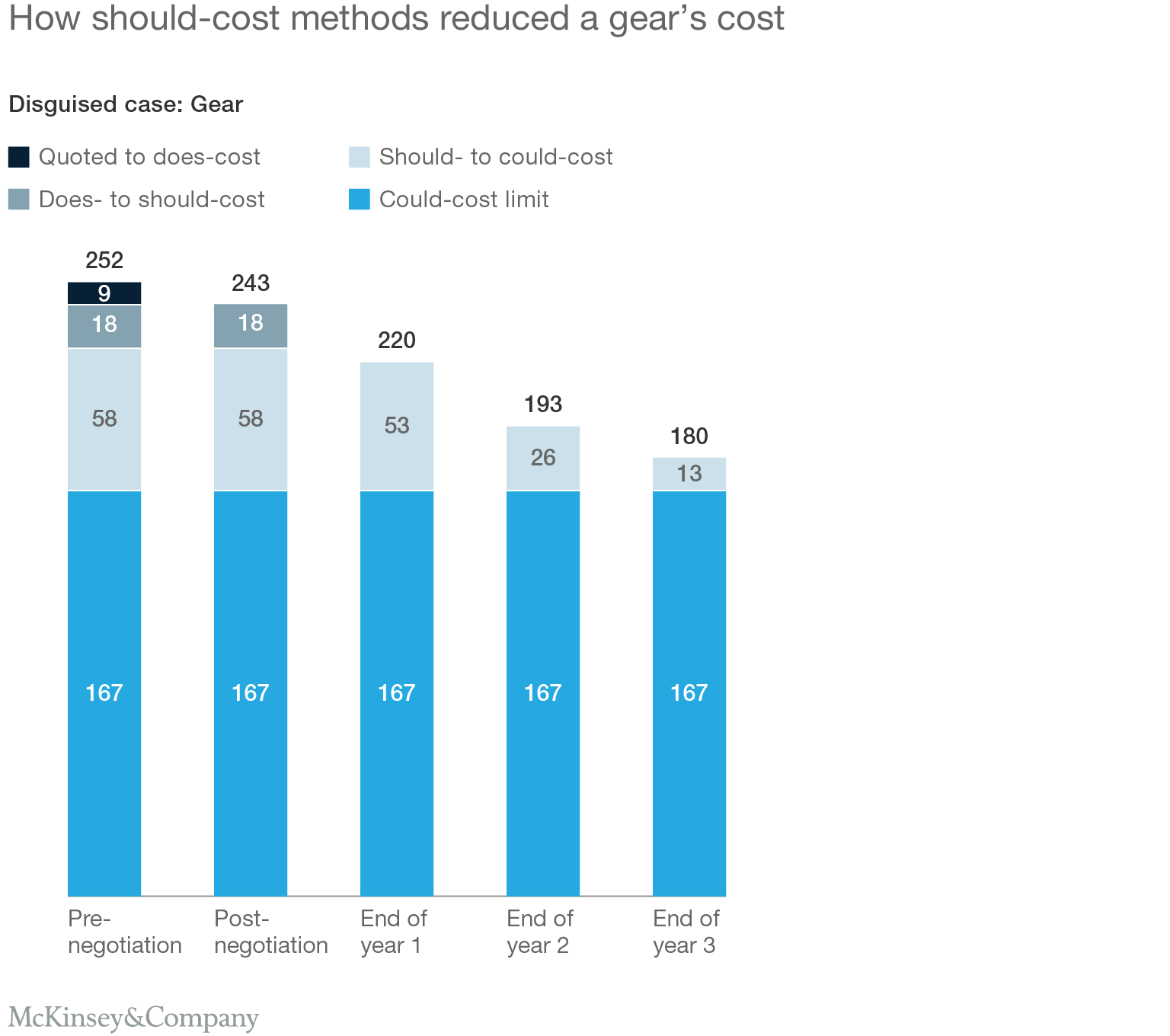

Let's look at how this approach might work on an actual part. Exhibit 2 shows the diagnosis of the cost gap for a gear.

In this example, the supplier and customer agree that another $18 of savings is possible with only minimal changes. Achieving that target will require the supplier to shift the part's production to a different, more-efficient line, and conduct a lean process-improvement event to generate further efficiency ideas. These actions are targeted to happen in a year, at which point the gap between does- and should-cost is fully recovered.

To address the should- to could-cost gap, the supplier needs to change to an entirely different process using a waterjet. However, capital constraints at both the supplier and customer mean that the waterjet machine cannot be purchased until year 2, reducing cost a by a further $27. That still leaves $26 of gap, which additional investments in year 3 could reduce by another $13.

At this point, the team may have exhausted its list of ideas, and it may be time to refine the Cleansheet model to identify new ones. But even if the remaining $13 cannot feasibly be recovered, reducing the cost from the initial $252 quote to $180 in three years is a significant win. It's based on specific, agreed-upon actions, not an amorphous "glide path" reduction target, which would likely have resulted in smaller savings.

Overcoming challenges

As they travel along the Cleansheet cost-management journey, companies may confront some common issues.

The supplier is already the lowest-cost alternative

The team may think it has already selected the lowest-cost alternative and that no other suppliers in the industry are available to quote. However, the Cleansheet analysis shows the lowest quote is still much higher than the could-cost. The team now has several options:

- Focus on cost reductions that raise the supplier's margin (or, at worst, are margin-neutral), such as by reducing the cost of raw materials or of sub-suppliers' parts or services.

- Look for suppliers outside the company's current industry that could provide the parts and certify them.

- Consider developing the capability to bring the part or service in-house.

- Redesign the part or service so it opens up other options for potential suppliers.

The supplier won't share granular cost data or assumptions

The Cleansheet process is built on fact-based negotiation. That is hard to do with only high-level, aggregated numbers. What if those are all the supplier is willing to share?

First, the purchasing team should ask themselves: have they ever asked for granular cost data before? Have they made it easy for the supplier to provide the data, such as by issuing a user-friendly list of information, or a template the supplier can quickly fill in?

Second, another useful strategy is to focus on physical quantities (masses, times, tooling, etc.) rather than cost numbers. This has several advantages:

- Suppliers tend to be willing to share physical quantities.

- Physical quantities allow a more bottom-up comparison of should-cost against does-cost.

- Physical quantities do not change with exchange rates or inflation.

Third, executives should communicate to the supplier the importance of fact-based discussions, with the message that disclosing the supplier's assumptions (and their basis in benchmarks or other data) is the best opportunity to find and correct mistakes that the customer's team may have made in estimating the does-cost number.

Finally, companies should ask themselves a few questions about their own longer-term actions to close the should-cost to does-cost gap.

- Have future-year savings been contractually recorded for the supplier and put on the internal action plans for the team?

- Has the future cost-review meeting cadence been set up?

- Has the team discussed how best to deal with limitations and excesses that are not actionable in the near- or mid-term—such as developing alternative suppliers or installing new equipment?

What Cleansheets can do

The concept of Cleansheet, while easy to grasp on the surface, is actually quite complex in an everyday product or service environment. However, with a good understanding of the approach, supportive management, and a dedicated and educated team, using Cleansheet as part of product cost management is a powerful profit-generating tool.

The key to closing the gap between could-cost and quoted or invoice cost is to break the gap down into smaller and more actionable cost segments, each with clear assumptions that can be compared with the supplier's assumptions. The team can make good progress towards does-cost in its first negotiation with a supplier (or an internal provider). Some of the could-cost to quoted-cost gap will require future actions, both internally and at the supplier, and these must be scheduled and tracked to gain savings. And although the quoted or invoiced price may never fully match the should-cost, with good oversight, the team can close more of the gap every year.

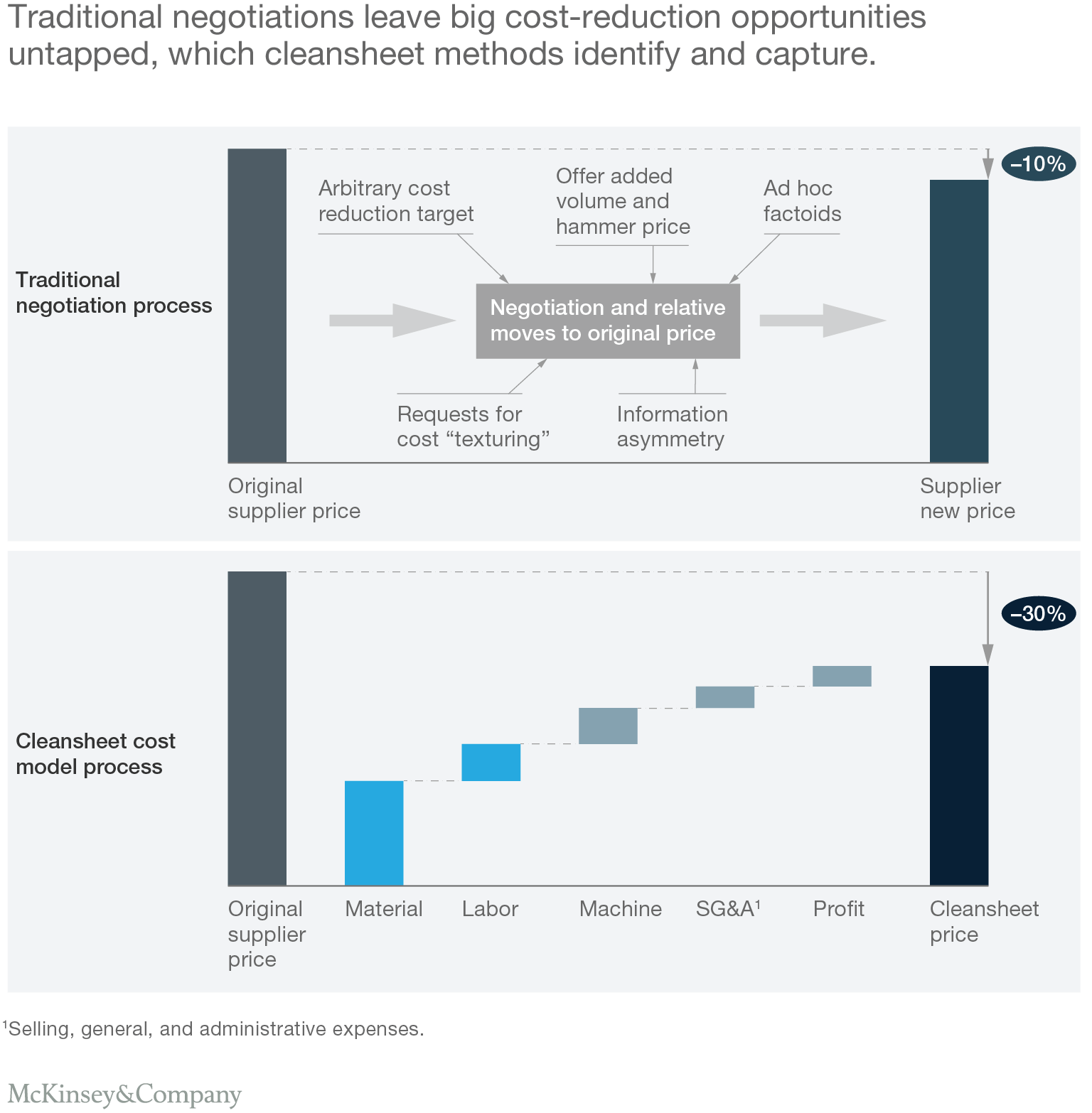

The Cleansheet methodology thus shifts the customer-supplier interaction from opaque and arbitrary traditional negotiations, based on a relative price movement, to transparent, fact-based bottom-up cost and profit estimates (Exhibit 3). Accordingly, the process usually results not only in greater savings, but also in better relations between supplier and customer: both sides of the table are aligning on the real reasons for gaps between the quote and the customer's expectations.

* * *

The Cleansheet process does require discipline and effort, but the potential rewards for the effort are huge. As we conclude this four-part series, here are some final questions to think about.

- Does your sourcing group negotiate the starting price of a contract based on facts—or power and contention in negotiation?

- Do you know what the cost of the part should be before walking into the negotiation, or do you just know it should be less than whatever the supplier offers?

- Do you and your supplier write specific cost reduction actions into the long-term contract, and work together to realize these savings, or do you just push on the supplier for undefined year-over-year "efficiency" reductions?

- Do you truly understand the assumptions that are in your cost models for parts and services, or does everyone seem to have different ideas of what is possible?

- Are you and the supplier clear on what changes need to occur to reduce part or service costs, and how long each will take to accomplish?

About the authors: Eric Arno Hiller is an expert in McKinsey's Chicago office.