| This week, how energy systems around the world are expected to change profoundly in the coming decades. Plus, what makes an organization healthy, and Tim Koller, a partner and corporate-finance expert, on recessions and value creation. |

|

|

|

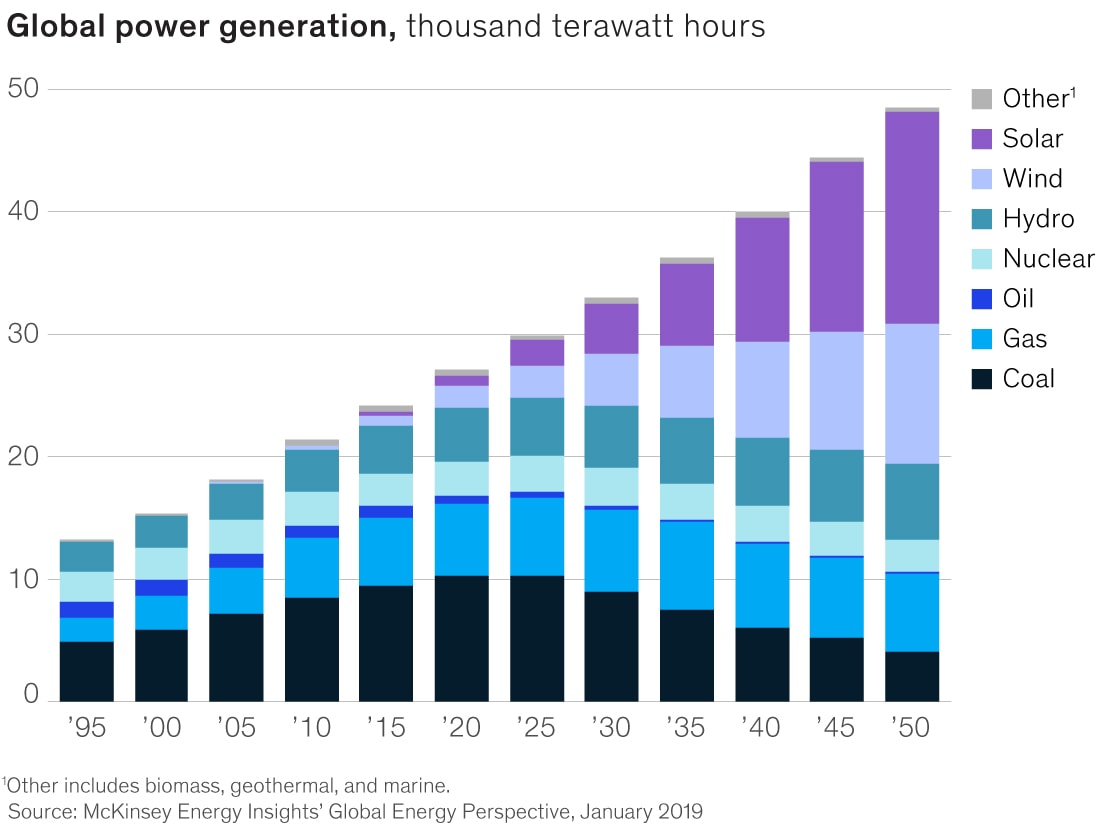

| A historic shift away from fossil fuels. The coming dominance of solar and wind power. The rise of electricity in road transport. Energy systems around the world are changing rapidly, which will transform the way we fuel our cars, heat our homes, and power our industries. That’s the conclusion of McKinsey’s Global Energy Perspective 2019, a detailed outlook across 146 countries, 55 energy types, and 30 sectors. |

| After more than a century of constant growth, global energy demand is expected to plateau around 2030—even as populations grow and become more affluent. How? In part, it’s the shift to low-consumption service industries, and even heavy industry is getting more efficient. For example, China’s total energy consumption for steel production may halve after 2035 thanks to more efficient blast and arc furnaces. |

| We’re also witnessing the rise of renewable resources. Wind and solar power are a tiny slice of overall production right now, but they’ve accounted for more than half of new capacity in recent years. The boom is yet to come, when building new solar or wind capacity becomes cost competitive with existing plants. Wind and solar are expected to increase by a factor of 13 and 60, respectively, from 2015 to 2050. By 2035, renewables are expected to make up more than 50 percent of generation. |

|

|

| On the flip side are fossil fuels. Growth in oil and coal demand is expected to slow, with oil peaking in the early 2030s. Gas demand is expected to grow until 2035, thanks in great part to outsized demand in China, then to plateau, largely because of increasing competition from renewables. |

| The big question, for many, is what all of this means for carbon emissions. For the first time, we project a peak in global carbon emissions—with the first declines in the mid-2020s and a fall of roughly 20 percent by 2050. Are deeper cuts possible? Yes. Here are eight potential shifts that could accelerate the energy transition. |

|

|

|

|

|

| INTERVIEW |

| CreditEase’s founder on how to ‘educate your prospect’ |

| McKinsey recently spoke with Ning Tang, the founder and CEO of CreditEase, a Chinese fintech firm providing wealth-management, lending, and other services to customers in more than 250 cities in China and, increasingly, around the world. |

| “We make our investor education very entertaining, like a video game. It’s very interactive, very participative,” he said. “In financial services, what’s the most effective customer-acquisition tool? It’s educating your prospect. If you become the prospect’s teacher, of course you can win his or her heart, right?” |

|

|

|

|

| MORE ON MCKINSEY.COM |

| What makes an organization healthy? | Organizations must be in peak condition to function well over time. To stay in shape, they should remain in sync with their customers and create an innovation model for the long haul, among other things. |

| Embracing the next-gen operating model | We’ve all heard that competing digitally requires a fundamentally new way of working. Here are six lessons that have made a difference for the companies that applied them. |

| The 3 Ps: people, people, and people | Change is hard for public-sector organizations. But by tackling the cultural factors underlying their cautious mentality, they can create new outcomes. |

|

|

|

|

|

| There has been a lot of talk in recent months anticipating a new economic downturn. You wrote a well-received article after the last downturn about that topic. What lessons can we draw from that article today? |

| The message back then was that executives should monitor credit markets, particularly for those parts of the economy with too much debt or loose lending standards. Our analyses showed that those markets were better bellwethers of change than equity markets, which always show volatility but don’t drive the economy as much as credit markets do. The same principles hold true today. Executives should pay close attention to credit markets and think about whether certain geographies or sectors—for instance, real estate, consumers, or government—are overleveraged, because that often indicates imbalances in the real economy. |

| Executives in emerging markets should also examine whether companies or governments are borrowing excessively in US dollars or in euros. Another factor for all executives to consider is the possibility of trade wars, which is something that hasn’t been an issue in decades. Unfortunately, once imbalances arise, there is no way to completely prevent a downturn; but at least you can be prepared when you see it coming. |

| In general, how do you think about recessions and the way they emerge? |

| After 2007, people put a lot of emphasis on trying to understand or remake financial theory and market regulations to keep us from falling into future recessions. Those factors are important, but in my view, bubbles and crises emerge when companies, investors, and governments forget to value “value.” That is, they misunderstand which investments create value, or they neglect to measure value properly, or both. They continue on this path until the magnitude of value-destroying investments triggers a crisis. |

| Think about it: securitizing risky home loans did not make those assets more stable or more valuable, as banks and financial-services companies argued when they sold those securities to investors. No additional cash flows were created, so no value was created, but the initial risks remained, eventually prompting a credit crunch when the volume of underlying bad loans became clear. And if you go back to the Asian debt crisis, building manufacturing capacity far beyond the needs of the economy and financing it with US-dollar debt was similarly destined to create problems. |

| I believe we need to relearn how to create and measure value in the tried-and-true fashion. This is an essential step toward creating more secure economies and defending ourselves against future crises. |

| What do companies and investors need to understand about value creation? |

| The guiding principle is that companies create value by using capital they raise from investors to generate future cash flows at rates of return exceeding the cost of capital (the rate investors require as payment). The faster companies can increase their revenues and deploy more capital at attractive rates of return, the more value they create. The combination of growth and return on invested capital relative to its cost is what drives value. |

| Companies can sustain strong growth and high returns on invested capital only if they have a well-defined competitive advantage. With this knowledge, companies can make wiser strategic and operating decisions, such as what businesses to own and how to make trade-offs between growth and returns on invested capital—and investors can more confidently calculate the risks and returns of their investments. The key to avoiding or mitigating the fallout from the next crisis is to reassert these fundamental economic rules, not to revise them. |

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

|

Copyright © 2019 | McKinsey & Company, 55 East 52nd Street, New York, New York 10022

|

|

|

|