The Great Recession has caused plenty of pain in the European insurance industry. Rock-bottom interest rates have reduced returns on the insurers’ holdings, while economic disruption continues to increase the volume of claims payouts.

Not all companies are suffering, of course; indeed, many are thriving. For insights into the factors that distinguish the top performers from the rest of the pack, we surveyed more than 80 life insurers and property-and-casualty (P&C) insurers across Europe.1 We were particularly interested in identifying the factors that most directly contributed to their superior cost performance, including product development, marketing, sales support, operations, and IT, as well as other support functions. Despite the strong economic headwinds, we found not only that companies in the top quartile of our survey outperformed their peers on costs but also that this operational strength—contrary to conventional wisdom—produced more robust revenue growth.

A yawning gap in costs

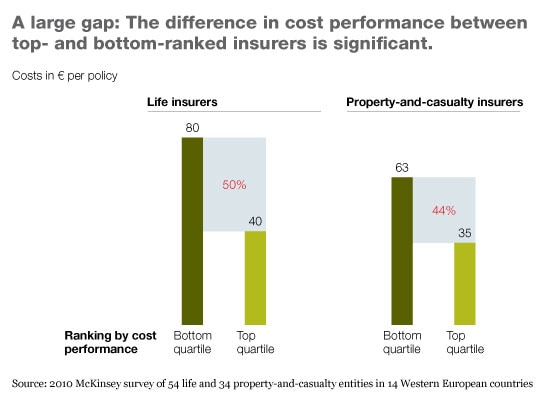

One of the more startling survey findings was the size of the cost difference between top- and bottom-ranked players. For top-tier insurers, the total operating cost per policy, across virtually every business function, is at least half that of companies at the bottom of the stack (Exhibit 1). Bottom-quartile players’ unit costs can be twice as high as those of top-quartile ones.

Some of the biggest differences result from the top companies’ much better cost management in sales support, operations, and IT. The consistency of this gap also runs contrary to the industry’s common wisdom: companies may squeeze costs in one area but must compensate elsewhere, with higher costs, to maintain revenues or buttress customer satisfaction. Instead, we found that top-tier insurers sustained their low-cost position without sacrificing top-line revenue growth. Leaders in our survey increased their gross written premiums—the industry’s standard revenue measure—two percentage points faster than the broader market index did.

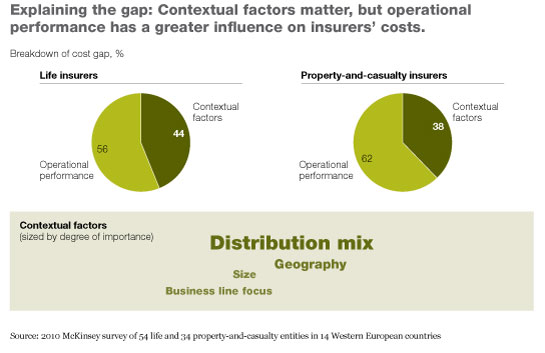

The survey also calls into question other industry credos (Exhibit 2). The first is that larger insurers have an implicit cost advantage. Our survey data show that while size provides some economies of scale, it often creates administrative and operational complexities that impede even larger efficiency gains. Second, it is often assumed that variations in the wages and regulatory regimes of different countries strongly influence the performance of the insurance companies that do business in them—in other words, that high wages and stiff regulations depress profits. Yet our findings indicate that top performers use operational excellence to dampen the effects of high wages and regulatory constraints. By moving back-office functions to cheaper near- and offshore locales, these companies deftly use labor cost arbitrage to create a lower average cost base. As a result, their cost performance is superior across all geographies.

Finally, we found that the best operators, despite their vigilance on costs, don’t allow that frugality to damage vital functions, such as customer service and due diligence for issuing new policies. When one large insurer found that its cost base was significantly higher than that of industry leaders, for example, its managers attributed the difference to the additional spending needed to ensure longer-term growth and profitability. The company assumed that its lower-cost competitors cut corners in areas such as risk assessment and undertook fewer medical checks to authenticate claims or confirm eligibility. Yet our analysis shows that low-cost leaders did not cut back in these areas and actually achieved higher levels of profitability than the company in question.

Fragmented IT and operations raise complexity and costs. The top-tier companies did more for less thanks to their operational excellence. In fact, among P&C insurers alone, top-quartile players’ profit margins, based on the industry standard combined ratio, were four percentage points higher than the average of the companies we surveyed.

How low-cost companies do it

Behind the low scores of our survey’s poor performers, one factor predominates: operational weakness. These companies are more likely to have an ungainly operational footprint, with limited cohesion among operating centers and fragmented IT systems, so they find it harder to streamline processes, share common tasks, and achieve economies of scale. Such deficiencies, which often disrupt a range of processes, lead to high backlogs, as well as frequent work-arounds and manual interventions—factors that slow down response times, raise costs, and hurt customer service.

We have identified three core operating principles that differentiate top-performing companies. These offer a roadmap for insurers seeking to improve their competitive cost position and growth prospects.

Create a centralized structure

Top performers are more likely to centralize their IT and back-office processes and to consolidate corresponding reporting lines under a single point of contact, often the COO, improving both productivity and governance. They are more likely, for instance, to pool medical experts instead of segregating them by location and channel. This approach reduces the number of resources needed—in some cases by as much as 40 percent—while increasing the quality of the guidance.

Taking this approach, one insurer—ranked in the bottom quartile back in 2007—began a three-year transformation to consolidate its back-office support functions and associated IT platforms and to shrink a sprawling network of over two dozen operational centers. These moves shaved 27 percent and 25 percent from the cost of operations and IT, respectively, and bumped the company from the bottom to the upper-middle quartile in cost performance. The savings were reinvested in several new product initiatives, which eventually raised the company’s market share in several key areas.

Ramp up automation

Top performers make wider use of automated processes, often deploying self-service systems that help customers, insurance agents, brokers, and independent financial advisers process simple transactions (such as low-risk claims) with minimal resort to adjusters.

One P&C insurer cut its processing times by 30 to 40 percent when it automated high-volume, low-risk claims for the replacement of damaged vehicle windshields and the like. Using computer-based, straight-through processing techniques that combine separate steps into an integrated work flow, the company’s process is now completed electronically, without manual intervention. Another insurer, faced with rising claims losses, decided to automate its loss-management process. By standardizing decision making through rules-based programs about eligibility requirements and new compliance guidelines, the company reduced its leakage from payment errors by 4 percent of revenues. These savings, which allowed the insurer to keep down prices for its most popular products, gave it a leg up on the competition and helped raise its revenues.

Use lean process design

Many low-cost leaders have applied lean-manufacturing techniques to alleviate backlogs and improve response times. That design focus allowed these companies to streamline their core activities across the business, to eliminate redundancy, and to route tasks and manage work flows more effectively.

One life insurer, for example, seeking to help its brokers, revamped the redemption process to speed up payout times, a key driver of customer satisfaction. A diagnostic revealed several problems, including frequent back-and-forth steps needed to complete documentation and a system that often jumbled together urgent and routine requests, making it hard for adjusters to prioritize tasks. The result was often weeks-long delays in the vetting and approval process.

In response, the insurer created two separate work streams, one for administrative or routine requests that were less time sensitive, the other for payouts. The company also established strict performance targets governing the payout timetable. For each step in the process, it set time limits, such as the number of days a given piece of documentation could rest with an individual agent or process owner. These changes shortened the payment process to 8 days, from 18, while improving overall productivity by 25 percent. In addition, the company now measures customer satisfaction, obtaining feedback directly from the broker network and using that information to further refine the process.

As our survey shows, organizations that take the steps we recommend stand a strong chance of outperforming their peers. While these findings center on the insurance industry, we believe that the same thinking can be applied to other service industries in which IT and operations can play a key role in speeding time to market and improving the way companies meet their customers’ needs.