Automated claims processing, price comparison platforms, mobile bill paying—these are just some of the digital services that insurance customers expect and insurers want to provide. As the demand for digital skyrockets, so does the need for insurers to invest in IT. In the past seven years, the share of IT in total operating costs of property-and-casualty (P&C) insurers increased 221 percent. The rise of digital means technology is no longer a cost center. Rather, it is an asset that, if managed well, can increase growth and profitability.

But do these IT investments pay off? As the COVID-19 pandemic exacerbates already increasing cost pressures, insurers’ IT budgets are under scrutiny; they want to see the business impact of their IT investments.

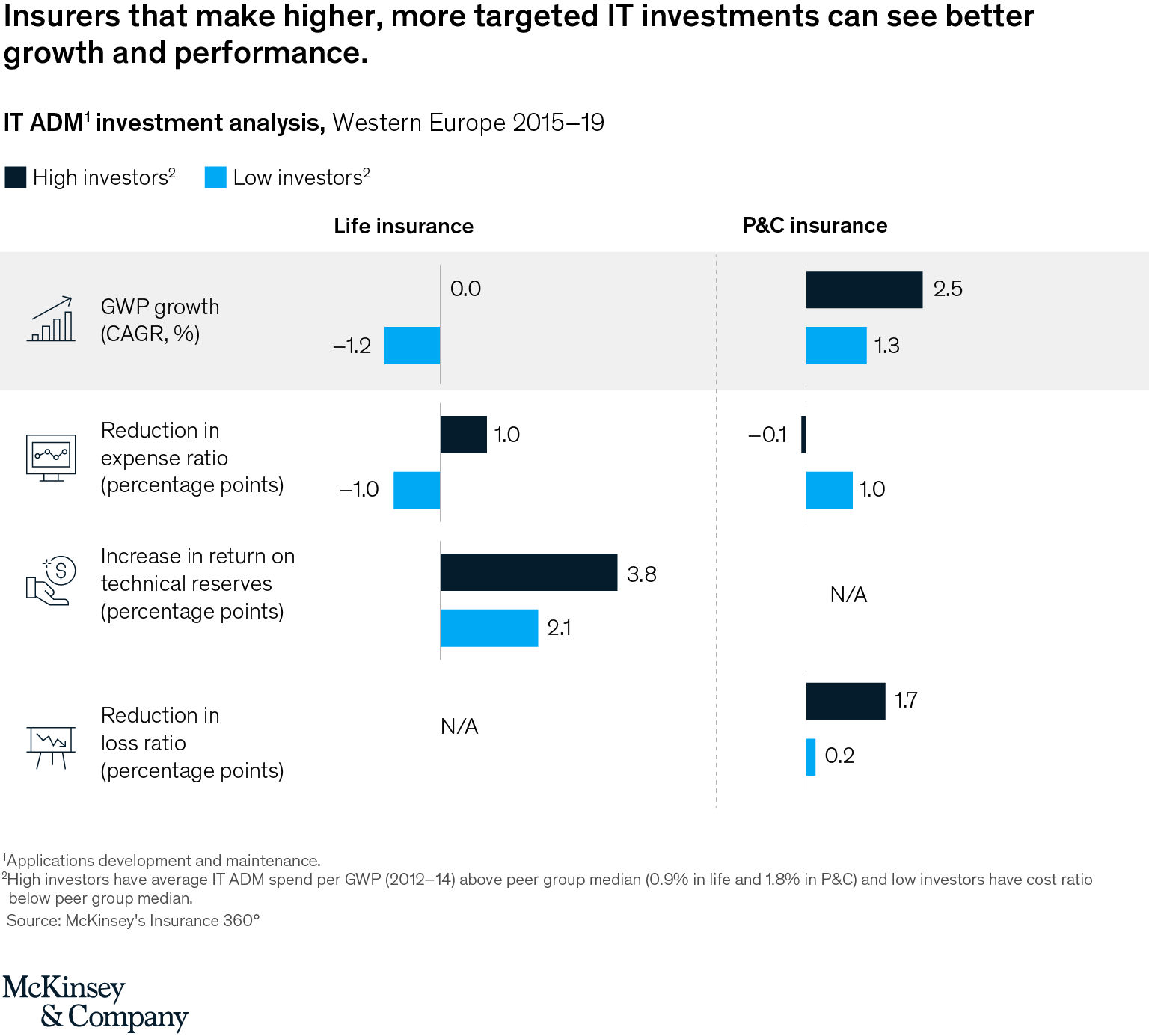

Insurers with targeted IT investments achieve better growth and performance

Data from McKinsey’s Insurance 360° benchmarking survey provide strong evidence of the positive business impact of targeted IT investments. In fact, insurers that invest more in technology outpace competitors that don’t pursue targeted investments in business measures such as gross written premium (GWP) growth, return to shareholders, and expense and loss ratio (exhibit).

As an example, in life insurance, companies that invested more in IT saw a greater reduction in expense ratios (by 2.0 percentage points) and higher returns on technical reserves2 (1.7 percentage points) when compared with insurers with lower IT investments. Insurers achieved these outcomes within three to five years of making their investments.3

For P&C insurers, those with high IT investments achieved approximately twice the top-line GWP growth of low IT investors. High IT investments also produced a greater reduction in combined ratios when compared with those with low IT investment.

Four areas for targeted IT investment

So what kinds of technology investments can help insurers achieve growth and improve productivity and performance? Investments in four areas are critical:

Marketing and sales: Marketing technology solutions can increase sales and processing efficiency, improve the quality of core customer-facing processes such as policy inquiries and policy applications, and improve customers’ overall experiences. McKinsey’s Insurance 360° benchmarking data show that tech investments in this category can facilitate top-line growth for P&C insurers by up to 20–40 percent; for life insurers, that growth could be 10–25 percent over a three- to five-year period.

Underwriting and pricing: Automated underwriting fraud detection can improve the likelihood that insurers correctly identify fraud and set accurate prices. A pricing tool kit that analyzes pricing across competitors and enables a flexible, more segmented market versus technical pricing further improves profit margins. Insurers that deploy these and other product, pricing, and underwriting technologies have seen improvements in their profit margins by 10–15 percent in P&C insurance and 3–5 percent in life insurance.

Policy servicing: Workflow automation, artificial intelligence–based decision support, and user experience technologies in policy servicing and within IT can improve the customer self-service experience and automate back-office processes, thus reducing IT and operations expenses. And state-of-the-art self-servicing options will reduce processing times and even improve customer experience. An analysis of programs for large-scale insurance IT modernization finds that insurers that deploy these and other product, pricing, and underwriting technologies have seen improvements in their profit margins by 5–10 percent in P&C insurance and 10–15 percent in life insurance.

Claims: P&C insurers can use automated case processing—machine-learning technology trained to process basic claims cases—to segment more complex cases and significantly improve claims accuracy. Combined with better partner integration and steering technologies embedded in a transformation of the claims operating model, such technologies can help P&C insurers improve profit margins by 25–40 percent, according to McKinsey analysis of large-scale IT modernization programs.

To realize the full value of IT investments, insurers must strategically allocate their resources and view tech as an asset, not a tool.

Jens Lansing is a partner in McKinsey’s Düsseldorf office, and Ulrike Vogelgesang is a senior expert in the Hamburg office.

Download the full article (PDF)

1 For an earlier, more detailed analysis of changes in cost structures, see Tonia Freysoldt, Sylvain Johansson, Christine Korwin-Szymanowska, Björn Münstermann, and Ulrike Vogelgesang, “Evolving insurance cost structures,” April 11, 2018, McKinsey.com.

2 Technical reserves are the funds allocated to pay for underwriting liabilities.

3 For more information, see Shahed Al-Haque, Kia Javanmardian, Rohit Sood, Binu Sudhakaran, and Angelina Tan, “How insurers can improve combined ratios by five percentage points,” August 18, 2020, McKinsey.com.