Banks are trying madly to raise it, investors are wary of giving it, and lenders seem keener than ever to hang on to it. Strange, then, that we hear so little about how to manage the scarce resource of the day: capital. One reason for the lack of discussion is the sorry current state of the art of capital management. In the run-up to Basel II, banks treated the subject with appropriate energy. But as the global expansion after 2001 turned into a full-fledged boom, capital was plentiful and cheap, and a strategy to manage it was not only unnecessary but even, arguably, counterproductive. According to some, banks that worried about improving their capital usage were thinking too small and missing much bigger opportunities in rapidly expanding businesses. Whatever their view, most banks paid only scant attention to the husbanding of their capital.

Now, at a time when regulators, investors, and rating agencies, in various ways, are forcing banks to deleverage and increase capital ratios, the focus is on finding more of it—that is, on recapitalization. Of late, however, the search has yielded very little. Capital, when it can be found, is extremely expensive. Effective capital management is no longer just a nice, if somewhat obscure, skill to have; for some banks, it is a question of survival.

Out of necessity, then, banks are rediscovering the lost art of capital management. Done well, capital management not only answers the immediate need of improving capital adequacy; it also protects banks from risks and even enables growth. Should the industry consolidate, as seems likely, superior capital management will almost certainly be one of the chief distinctions between buyers and sellers.

While a comprehensive capital-management program includes seven elements, two of these—reducing capital “wastage” and developing “capital light” business models—are essential for boosting capital adequacy ratios. Many institutions squander their capital by allocating more of it to a business than is required. This can happen through inefficiencies in business and credit processes and poor data, and through poor choices in the risk-modeling approach. Banks can draw on a catalog of proven ideas to reduce this capital wastage.

They can achieve even more if they also successfully implement capital-light business models—that is, if they adopt smart credit-management principles in their day-to-day business and help frontline lenders and sellers internalize these principles. Typically, banks that both reduce waste and put in place capital-efficient business models can achieve a reduction of 15 percent to 25 percent in risk-weighted assets (RWAs). Further, some banks also see revenue increases of 8 percent to 12 percent. These improvements result in additional economic value—for one global bank, about 25 percent in two years. Seventy percent of impact is typically achieved within a year of launch.

Reducing capital wastage and implementing a capital-light business model are not only the cheapest ways to improve capital ratios—much cheaper than appealing to once-bitten, twice-shy investors—they can also inform the bank if it has any true additional capital needs. And if banks do instead resort to capital injections, they will not only pay dearly in the short term but also lock in their capital inefficiencies for the foreseeable future. At a time when the need to rebuild return on equity is paramount, capital inefficiency is like a weight around the neck—a burden that will keep the bank uncompetitive but that when removed will result in a powerful uplift to performance.

A new imperative

With the onset of Basel II, in 2004, banks were forced to take a more active approach to capital management. Capital requirements under the Basel II internal-ratings-based (IRB) approaches—especially the advanced, or A-IRB, approach—depend heavily on internal models to estimate risk. The quality of the data entered into these models is critical, and so banks began to pay more attention to how they used their capital. Thus at most banks, a bare-bones capital-management approach took hold.

The global financial crisis has rendered that basic approach untenable. Capital proved to be far less available than banks had assumed, and mark-to-market losses ($934 billion as of May 2009) from credit investments and subprime-related assets have eviscerated capital ratios at nearly every institution of any size. The rise in market volatility and the need for more capital to cover it only make the problem worse. The lack of adequate capital, as is well known, forced many banks into bankruptcy or into the safe haven of government rescue plans. To date, governments around the world have provided more than $1 trillion to recapitalize financial institutions.

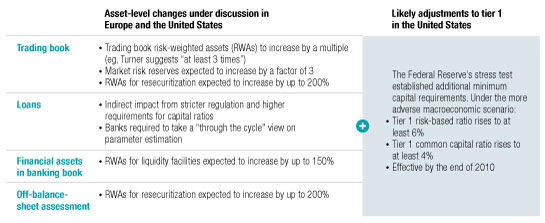

Already severe, the capital shortage will almost certainly get worse with the coming of new banking regulations. Ironically, the green shoots of economic recovery that many have noted may provide regulators with the faith they need to push through three changes that will particularly affect corporate and investment banks. First, most countries seem sure to impose a cap on banks’ leverage and to introduce “procyclical” adjustments to these such that in good times, the cap will grow tighter. Second, many believe that changes to the calculations used to measure risk in the trading book will increase RWAs by at least a factor of three (Exhibit 1). Off-balance-sheet items and securitized assets will also likely be saddled with much higher capital requirements. Finally, the focus will shift more toward tier-1 and common tier-1 capital (consisting mainly of common shares, cash reserves, and retained earnings), thus limiting the usefulness of the hybrid structures that many banks now employ to ensure capital adequacy.

Capital requirements on the rise

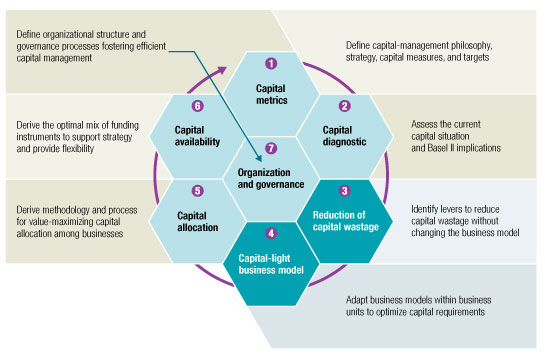

All these regulatory changes are in different stages of development and implementation but will likely come to pass over the next few years. While many banks are still struggling to come to grips with capital management, leading banks have recognized the trend and are establishing or recommitting to a comprehensive approach to capital management. Exhibit 2 lays out the seven building blocks common to the best of these approaches.

Seven building blocks

In our experience, two of these elements are essential for a successful hunt for capital, regardless of the bank’s starting position: reducing capital wastage and instituting capital-light business models. All the elements are important, of course, but for expediency we will concentrate on these two. The former is by far the more powerful and faster to produce results, and banks should begin with this.

Reducing capital wastage

As noted, the primary source of waste is a too-generous allocation of capital to individual businesses to reserve for the credit and market risks they run. We see three common mistakes that afflict most banks.

First, many banks have optimized their credit risk-mitigation activities (underwriting, collateral management, and workout) for cost efficiency—but in so doing have cut a lot of corners that considerably undermine their capital efficiency.

Second, banks routinely struggle with poor data. Although data issues exist throughout banks—some consider the modern bank more a technology business than a financial one—the problem is particularly acute when it comes to capital efficiency. Information is insufficient, incorrect, or incomplete (for example, gaps and noncredible outliers in loss databases used for risk-parameter estimation). Nor do banks always treat their data properly. Assets are often misclassified; for example, small-business loans are sometimes treated as retail rather than corporate exposures, when a corporate classification would reduce the risk weight.

Finally, although hard to believe given some of the risks banks took that culminated in the recent crisis, bankers’ innate conservatism actually leads them to overestimate their risks at times. The tendency is understandable: if estimates are too optimistic, regulators will likely question them and then impose additional capital reserves. Another problem is that banks choose and develop risk models from a purely mathematical perspective, giving little or no consideration to the realities of the business. For example, estimates of loss given defaults (LGDs) are often set too high. Finally, many banks use the same internal model for all their businesses, when a variety of models, including some less conservative ones, might be more useful. For example, the Effective Positive Exposure (EPE) model for counterparty risk in trading book assets is not used as extensively as it might be.

Capitalizing on the opportunity

All these practices eat up more capital than the business really requires, presenting banks with an opportunity. Banks should begin by thoroughly checking the data quality and risk-parameter estimates in their banking and trading books. They should then benchmark the main risk parameters, especially:

-

Effective risk weights by asset classes, that is, RWA per exposure at default (EAD)

-

LGDs by asset class, and, more specifically, the level of collateralization by portfolio segments and recovery rate by collateral type

-

Credit conversion factors (CCFs) by product categories. CCFs are used to calculate EADs, which equal drawn exposure plus the CCF times undrawn exposure

Further analysis can identify whether any gap between current performance and best practice is due to inadequate processes or poor data quality, or perhaps overly conservative modeling. For example, high risk weights for a given asset class can be a sign of too little Basel II–eligible collateral. Digging deeper, the bank might find that its model does not sufficiently distinguish between different types of collateral or does not manage the collateral provided for maximum value.

Knowing the source of the problem, the bank can then design a highly specific program of capital optimization. Our experience suggests that there are more than 100 levers available to reduce capital wastage. For further details on some of these levers, and for an example of a large European bank’s use of them in developing a capital-optimization program, see Exhibits 3 and 4 in this article’s downloadable PDF. Note that there are no “silver bullets” in this work; rather, it is the sum of 20 to 30 small optimizations that generates the significant amount of capital savings that these programs can produce.

Although banks will not often choose exactly the same set of capital-wastage reduction levers, we have found the following to be especially powerful for most banks:

Improve collateral management in the banking book. As a rough rule of thumb, each additional euro or dollar of Basel II–compliant collateral reduces RWA capital by 50 cents without changing the exposure at default. This makes collateral management a significant source of additional capital. Two ideas often work well to improve this activity. First, a comparison of the front-office systems with the back-office systems that are used in the RWA-calculation model will often reveal that there is much more Basel II–eligible collateral collected than is entered in the model; data quality is often the underlying reason. Banks can correct the data and make sure that all the available collateral is used to mitigate RWAs. Second, the ways that collateral is classified and valued are often suspect; improving this can also significantly reduce RWAs.

Improve netting and collateral processes in the trading book. Collateral management is also an issue in the trading book. As financial markets recover, demand is rising for capital markets and risk-management products. At most banks, the 20 or so largest corporate and institutional customers are again pushing up the capital requirements for counterparty risk in the trading book. More frequent settlement with corporate customers and faster collateral processes can significantly slow this RWA increase. Surprisingly, netting processes are far from perfect. In the quest for cost efficiency, many banks have not put in place netting agreements with their second- and third-tier counterparties—even though in aggregate these customers create significant RWA and capital requirements. Similarly, banks do not often have collateral agreements with these smaller customers; as a result, RWAs increase with every profitable trade.

Adjust Basel II risk parameters. Regulators usually require banks to include unresolved cases of default or workout in their estimation of recovery rates and LGDs. Banks must make some assumptions about the extent of eventual repayment. They tend to take the most conservative approach and assume very little or no further payment; after all, this minimizes time and money spent on model development and allows banks to avoid intense discussions with regulators. A more realistic and still inexpensive approach is to estimate repayment based on the current status of the workout or restructuring. This not only significantly lowers the bank’s LGD and the loans’ risk weight but is also much more representative of business reality.

Reconfigure credit processes and install early-warning systems. Since estimated risk parameters under A-IRB are based on a bank’s historical losses, they reflect not only the bank’s assumptions about the future but also the past performance of its credit processes. Improving credit processes is its own reward, of course, as it reduces credit losses. But it also improves risk parameters, allowing the bank to further lower its CCFs and EADs, LGDs, and risk weights.

In the past year, many banks have been caught off guard as financially weak customers drew down lines of credit and then defaulted. Banks should make timely and full use of all available information, such as credit-line usage, incoming payments, and reports from credit bureaus, to develop insights into customer behavior. These leading indicators, coupled with better credit-monitoring processes, allow a bank to identify high-risk customers early—typically six to nine months before loans become past due. Banks can then reduce their lines with some at-risk customers and also ensure that no additional credit is extended to them. This will lower CCFs and EADs, and can also help lower LGDs as uncollateralized exposures are reduced and banks get faster at seizing and liquidating collateral.

Capital-light models

The second essential element of effective capital management is the longer-term ambition to align a business unit with the principles of efficient capital use—what we call the capital-light business model. The gap between principle and practice is often large. For example, two or three products might serve a customer’s needs equally well, with no noticeable differences to the customer—but they may have very different implications for the bank’s capital requirements. Similarly, a loan can be collateralized in various ways; the choice makes a big difference to the bank’s capital. Cash and high-quality securities such as US government bonds are the most capital-effective; real estate is typically much more capital-effective than inventory; and residential real estate is in most countries more effective than commercial real estate.

Some banks have taken steps toward a capital-light model by streamlining their processes, actively managing the credit portfolio, and rethinking their securitization strategies. These are good moves, but banks can do more. We suggest five actions to establish a capital-light business model.

Embrace risk-adjusted pricing. Banks should introduce risk-adjusted pricing for every client type and every product. The move to risk-adjusted pricing began many years ago but is still not standard operating procedure at some banks where risk is consistently underpriced. Risk-adjusted pricing is an essential first step to maximize value for the bank; the price of a loan must cover the bank’s cost for risk, capital, liquidity, and operations.

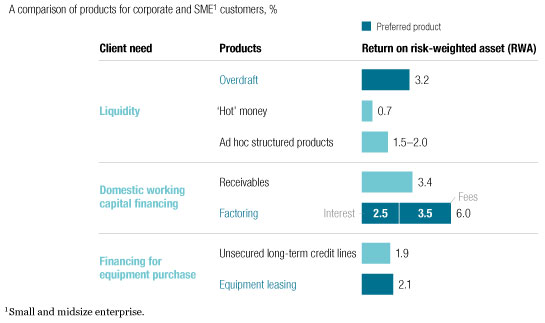

Sell the right products and get the right collateral. Banks should provide commercial guidelines and tools to help the front line meet two goals: to sell the product with the highest RWA-adjusted return for a given customer need and to boost the level or quality of collateral wherever possible, without jeopardizing that return (Exhibit 5). To achieve both goals—that is, a product and collateral that are optimized for both economic value added (EVA) and RWA returns—frontline staff must have transparency into RWA under Basel II, and their incentive schemes must be set accordingly.

Sell the right products

Understanding the return on RWA is essential; it may look very different for short-term lending and factoring, or for investment loans and leasing. To help sellers with this, actual risk costs must be reflected in pricing and performance calculations. Staff must be well trained in Basel II regulations and equipped with the necessary tools—simulation tools and pocket guides that will help them quickly assess the implications of their choices.

Many banks give sellers incentives based on ROE at the time of origination and then freeze this ROE for purposes of compensation. A better approach is to link compensation to ROE at various points in the life cycle of the loan. That creates a situation where, when the client’s credit risk deteriorates and its capital consumption increases, the responsible lending officer will follow up and ask for additional collateral or take other action to reduce exposure.

Advise clients on financial ratings. Banks can provide clients with solutions to improve their financial profile and therefore their rating. If successful, clients will reduce their cost of credit, and banks will be able to lower their reserves for products sold to these clients. Clients will also gain from a better understanding of Basel II logic and opportunities. Additional benefits for the bank include a deeper relationship with the client and strong cross-selling opportunities that will emerge from the client’s enhanced knowledge.

Develop a superior capability for market placement. Banks should put in place all the requisite skills and infrastructure needed to participate fully in opportunities to sell assets, such as syndication, club deals, private placements (which have proved resilient through the crisis), and also, once the crisis has passed, securitizations. Obviously, securitization has become much more difficult and will change further with Basel II. Banks must rethink their approach to this business. But even now, when liquidity in most markets remains dried up, disposing of parts of the loan portfolio, either through securitization or syndication, can be a successful strategy to reduce RWA. To capture the benefits fully, banks need for the moment to follow Basel II–optimized securitization strategies and then to be ready to update these when expected changes come through. One thing that is clear already is that securitization structures will have to become more transparent. More standardized credit contracts for securitized loans and more transparent securitization structures—in other words, instruments comparable to the German Pfandbrief and other covered bonds—will have to be adopted.

Scale back business with EVA-negative clients. Often very few customers (5 percent or less) account for more than 20 percent of RWAs and do not contribute significantly to the bank’s P&L—even before the cost of capital. Banks should sort through their portfolios, especially in corporate banking, to reduce their business with these clients, and they should put in place strict rules on new business that will prevent them from acquiring more.

Identifying these clients is difficult, however. Some banks may first need to develop a metric for customer profitability, embed it in their systems, and then systematically review the portfolio. They can then reduce their business with EVA-negative clients. Large customers should be discussed at the highest level and each case considered individually. For small customers, a special unit can work to reduce exposures and change the product mix. To keep the problem from getting worse, banks can provide guidelines to frontline staff, as discussed earlier.

Reducing capital wastage and transitioning to a capital-light model are not straightforward approaches. Banks must lay the groundwork if the efforts are to succeed. In our experience, there are three prerequisites. First, banks must establish clear governance of capital management at every level. This task must be incorporated into the mandate of a senior leader, usually the CFO or CRO, and people responsible for the activity in every major business unit must report in to him. Second, the bank must ensure the close collaboration of the businesses and the risk and finance groups. A cross-functional team goes a long way toward meeting this goal. Finally, the bank must focus relentlessly on execution. An excellent way to maintain focus is to continually track the increases in capital and the impact on the bottom line. Some leading banks have already institutionalized the hunt for capital by setting up RWA- and capital-management units and launching internal competitions to find capital-savings opportunities.