Consumer anxiety about retirement risks has jumped dramatically in the United States as a result of the economic crisis, which last year reduced the value of US household financial assets (excluding real estate) by an average of 18 percent. Yet the vast majority of US consumers haven’t changed their investment portfolios and don’t plan to postpone retirement, according to our nationwide January 2009 retirement survey of 2,000 US consumers. This finding suggests that many of them have not yet figured out how to react to the crisis.

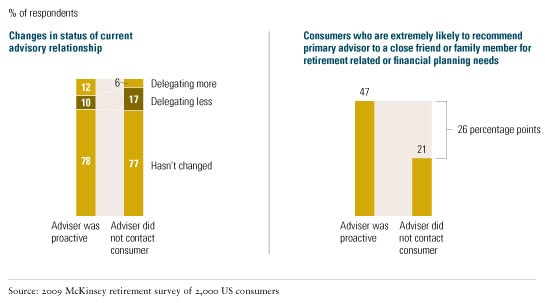

The reason, in part, may be that financial advisers have provided only limited guidance to their clients over the last six months, reaching out to just two in five of them—perhaps fearing an angry response after 2008’s staggering $2.4 trillion decline in the value of retirement assets in defined-contribution accounts and IRAs.1 The overall level of advice from financial advisers fell significantly, compared with 2007. But the best advisers were smarter: they reached out systematically and proactively even to clients with significant losses. The results, according to our survey, were significantly strengthened relationships, referrals, and asset flows.

To be sure, retirement fears have spiked across the board, as the results from our survey show: consumer anxiety about interest rate risks and a lack of guaranteed income has more than doubled, to around 60 percent, from the levels prevailing three to five years ago; worries about market and inflationary pressures have jumped by half, to about 75 percent; women continue to be significantly more anxious than men; and high-net-worth individuals—those with more than $1 million in investable assets—are even more concerned than others.

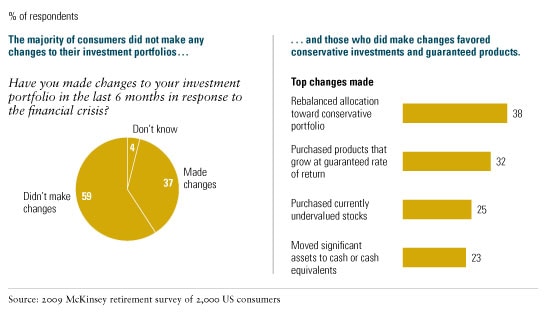

US consumers haven’t panicked, however: in the past six months, only 1 percent have moved assets away from their primary financial institution, just 37 percent have changed their investment portfolios, and no more than 20 percent have changed their retirement portfolios. Those who did make changes have tried to reduce their risk levels by rebalancing allocations toward conservative assets (38 percent), products with guaranteed rates of return (32 percent), and holdings of cash and cash equivalents (23 percent) (Exhibit 1). Most preretirees have also responded to the financial crisis by curbing their lifestyles: some 60 percent reduced spending in the six months leading up to January 2009, and 73 percent paid down debt.

A passive response

Although consumers have taken some prudent near-term steps, these could be masking a deeper failure to understand the state of retirement security. McKinsey’s retirement readiness index (RRI)—which uses Social Security, defined benefits, defined contributions, and other financial assets to measure the financial preparedness of households for retirement—is currently at 63 for an average household in January 2009.2 Consumers must have an RRI of 100 to maintain their current standard of living at retirement. An RRI below 80 calls for large reductions in spending on basic needs, such as housing, food, and health care.

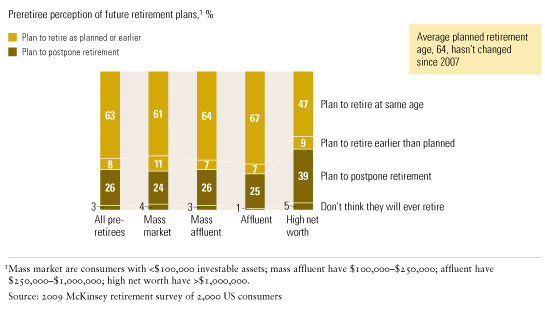

Yet our survey showed that only about a quarter of US consumers are considering postponing retirement as a result of the crisis: the expected retirement age, 64, hasn’t changed since 2007 (Exhibit 2). Despite the fall in home values, the proportion of people planning to finance their retirement through home equity has increased slightly. Although high-net-worth individuals seem more willing than others to work longer—39 percent now expect to postpone retirement—they aren’t willing to compromise their lifestyles or financial bequests.

No postponement

Trust improves the relationship

This disconnect between the crisis and the response to it means that financial advisers have a significant opportunity to step up their game and help consumers get back on track. Despite the failure to reach out, just 1 percent of preretirees hold their individual advisers primarily responsible for the impact of the crisis on them, compared with 43 percent who blame the government and regulators, and 27 percent who blame financial institutions. Indeed, proactively reaching out to consumers may be the best investment advisers can make right now: those who did so were nearly twice as likely to be recommended by them (Exhibit 3). Proactive advisers and institutions seem to have a compelling opportunity to win the trust of consumers, build stronger relationships with them, and provide practical, affordable solutions that can help people recapture their retirement dreams.