The global financial crisis has shown that the developing world no longer holds a monopoly on investment risk. A new risk reality has emerged—one that is ubiquitous and less associated with the developing regions of the world. Thanks to this new reality, combined with macrotrends affecting the global economic landscape, businesses are now looking for new markets in which to invest. In the aftermath of the crisis, the “South–South” expansion of trade and investment is likely to accelerate thanks to the global appetite for natural resources; the effects of climate change will continue to complicate growth and open up new investment opportunities; and changing demographics will have important implications for productivity and demand. Against this backdrop, sub-Saharan Africa offers a better platform for profitable new investments than ever.

Future global economic growth will increasingly come from emerging markets. Following more than 20 years of hard-won political and economic reform, sub-Saharan Africa will be an important part of this story. Africa is often associated with poor governance, weak institutions, civil unrest, a lack of infrastructure, and other difficulties. The extent of these problems cannot be minimized, and African governments and civil society must continue to work against them. But there is an emerging side of the African story that speaks of successes often achieved below the radar screen. The region aspires to move past the image of extreme poverty and conflict with which it has long been associated and to show that it is not only open for business but also actually in business. Before the crisis, sub-Saharan Africa had been growing fast, with an average annual growth rate of 6 percent between 2002 and 2008. The region, which is weathering the global downturn better than most other parts of the world, is projected to grow by 3.8 and 4.5 percent in 2010 and 2011, respectively—faster than Latin America, Europe, and Central Asia.

Sub-Saharan Africa’s recent sustained growth has been made possible largely by improved political and macroeconomic stability, a strengthened political commitment to private-sector growth, and increased investment in infrastructure and education. Many sub-Saharan African countries have liberalized trade since the early 1980s, and throughout the continent fiscal soundness and monetary discipline are increasing. Debt as a share of exports has declined dramatically, to levels comparable to those of other regions, and sovereign credit ratings in parts of the continent enjoy a positive outlook. More of the region’s countries are now regarded as frontier emerging economies with relatively developed financial markets, including Botswana, Cape Verde, Ghana, Kenya, Mauritius, Mozambique, Namibia, Nigeria, Seychelles, South Africa, Tanzania, Uganda, and Zambia.

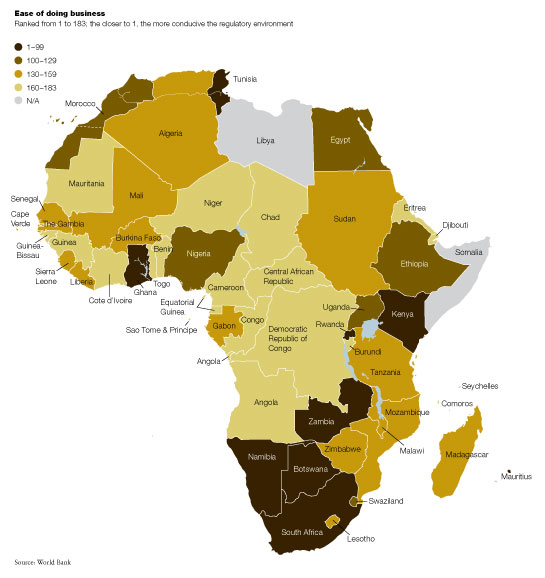

Most encouraging of all is the fact that the region is continuing to reform through difficult times. There is a broadly shared conviction among sub-Saharan Africa’s leaders that sustained growth will come only from the private sector and increased integration with the global economy. Last year, two-thirds of the economies of sub-Saharan Africa implemented reforms to ease the path of investors doing business there. In 2008–09 alone, Rwanda completed seven reforms, Mauritius six, and Burkina Faso and Sierra Leone five each. Indeed, Rwanda’s and Liberia’s measures were so significant that they both received “top reformer” status: Rwanda was the number-one reformer world-wide in Doing Business 2010, and Liberia was number ten.1

These reform efforts have been complemented by increased investments in infrastructure and human development. The figures for average years of schooling are catching up fast with those of the rest of the world, after having increased more than fivefold since 1960. Infrastructure spending amounts to $45 billion a year and absorbs more than 5 percent of total GDP.2 A recent $600 million private investment in high-capacity fiber-optic cable connects southern and eastern Africa to the global Internet backbone, widening the continent’s horizons of connectivity.

World Bank Index

Resource rush

As developing countries continue to increase their exports and imports, South–South trade and investment will make up a mounting share of global economic activity. Since 1990, sub-Saharan Africa has almost tripled its level of exports and diversified its trade and investment partners. The combined share of its exports to the European Union and the United States fell to 49 percent, from 73 percent. During this time, Chinese imports alone from sub-Saharan Africa increased to over $13 billion, from $64 million.

Natural resources will continue to be a key source of export revenue for sub-Saharan Africa as global demand, albeit decelerating when the economic contraction began, continues to grow. With pre-crisis growth rates and booming prices, investments in nonferrous metals around the world rose to $9 billion in 2007, from $2 billion in 2002. During this time, foreign direct investment in sub-Saharan Africa grew for eight consecutive years. Most of this investment took the form of greenfield and expansion projects prospecting for reserves of base metals and oil. In one decade, the region’s mineral fuel exports rose to $96 billion, from $11 billion. Today sub-Saharan Africa is not only a major supplier of natural resources but also the region with the greatest potential for new discoveries. As global growth resumes, the region should benefit from higher prices, in addition to higher volumes. The World Bank predicts that both energy and food prices, driven predominantly by the emerging economies’ resource needs, will remain high over the next 20 years.

The resource rush will also increasingly target renewable sources of energy. Sub-Saharan Africa is particularly well positioned for developing solar and hydro energy, as well as the production of biofuels. But the 2008 food crisis highlighted what could go wrong if food production is substituted for biofuels production. Africa can and must feed itself first while engaging in the development of a biofuels market that does not compete with food production. Between 2003 and 2007, two-thirds of the global increase in corn output went to biofuels, mostly to meet demand in the United States. While biofuels have contributed to higher food crop prices, they also represent an opportunity for profitable production in the developing world. Sub-Saharan African countries, including Angola, Mozambique, and Tanzania, have the potential to produce ethanol profitably from sugarcane on land that is not used for food crops. The International Energy Agency suggests that demand for grain to produce biofuels could increase by 7.8 percent a year over the next 20 years.

Rising commodity revenues will ultimately allow sub-Saharan Africa to increase its investment in infrastructure and education, especially as it continues to improve its business governance. Some 28 sub-Saharan African governments have adopted the Extractive Industries Transparency Initiative (EITI),3 with the aim of improving governance through the verification and full publication of company payments for and government revenues from oil, gas, and mining. In addition, 37 oil, gas, and mining companies, with assets amounting to more than $14 trillion before the financial crisis, have agreed to support the initiative.

Sub-Saharan Africa’s natural resources also provide it with a strong comparative advantage in agricultural development. The region has the resources both to feed its growing population and to meet the world’s burgeoning demand for food and other agricultural products. In sub-Saharan Africa, demand for food is expected to reach $100 billion by 2015, double the levels in 2000. Moving forward, appropriate investments in agricultural skills and infrastructure—for example, irrigation—could prompt a green revolution in sub-Saharan Africa. Both nontraditional and traditional exports are important, as are regional export markets for food staples and livestock. Global markets for nontraditional exports such as horticulture are expanding rapidly. Sub-Saharan Africa has many success stories, such as the production of cassava chips in Ghana, organic coffee in Tanzania, and cut flowers in Kenya, as well as aquaculture in Malawi. All of these products are exported to European and other Western countries. Expanding markets such as dairy production in east sub-Saharan Africa could also be scaled up for faster growth.

On the IT front, Africa has made great strides. It has, for example, become the fastest-growing region in the global cellular market, going from fewer than 2 million mobile phones in 1998 to more than 400 million today. More than 65 percent of the population now lives within reach of a wireless voice network, up from less than 1 percent ten years ago. Mobile phones have become the single-largest platform that can be used to deliver government services to the poor. Yet while great progress has been made in improving access to the information and communications infrastructure in many countries, much less effort has been made to exploit its potential to transform other sectors.

Climate change

Access to resources and agricultural development will increasingly require new methods of engagement with nature, such as the use of innovative technologies in energy consumption. Climate change makes the challenge of sustainable growth more complex. Developing countries, whose average per capita emissions are a third those of high-income countries, need major expansions in energy, transport, urban systems, and agricultural production. If pursued using traditional technology with carbon emissions, these developments will produce more greenhouse gases and, hence, contribute to climate change. With rain-fed agriculture helping to generate 30 percent of sub-Saharan Africa’s GDP and 70 percent of its employment, the region is particularly vulnerable. Climate change will continue to pose significant dangers to the region’s economic growth, with more droughts, floods, storms, and heat waves. Yet many adaptation and mitigation activities have significant benefits not only for environmental sustainability but also for public health, energy security, and financial savings.

Africa has great potential for sustainable, intensive farming through investments in new technologies and the conservation of vegetation, soil, and water. These approaches provide a “triple dividend” supporting adaptation to climate variability and change, mitigating carbon emissions, and promoting food security. The financial resources generated through mitigation could be very substantial. In sub-Saharan Africa, the economic potential from agricultural soil carbon sequestration is estimated to be 150 million tons of greenhouse gases a year. If agreement is reached at the 2010 UN climate change conference, in Cancún, Mexico,4 on the price per ton of carbon dioxide, Africa stands to benefit substantially from this new revenue stream. There is also great potential for reducing emissions from deforestation and forest degradation.

In short, the continent’s future potential for environmentally sustainable private-sector growth and opportunities in carbon abatement are immense. Sub-Saharan Africa has enormous potential for generating clean energy, such as solar, wind, and biomass. Preliminary results from two pilot projects in Kenya also show that smallholder agriculture can be integrated into the financial arrangements for carbon abatement.

Demographics

In the coming decades, one of sub-Saharan Africa’s most powerful offerings may be its growing population of young people, who serve as a source of competitive labor and a growing consumer market. It is estimated that by 2050, almost 20 percent of the world’s population will live in 4 Africa, up from 7 percent in 1950. Developing countries will be home not just to a larger share of the world’s population but also to a younger population. By 2050, young people 15 to 25 years of age will account for one person in five in sub-Saharan Africa.

By the same token, the region is rapidly urbanizing. Between 2000 and 2008, the rate of urbanization in sub-Saharan Africa was more than twice the world average. The region leads even the rest of the developing world. The United Nations projects that the proportion of sub-Saharan Africa’s people living in urban areas will nearly double between 2005 and 2050, from 35 percent (300 million) to more than 67 percent (1 billion).

Urbanization and the growing young population will have significant implications for productivity, growth, and demand. Sub-Saharan Africa has the potential to become an increasingly important resource for labor-intensive industries if it continues to invest in skills and infrastructure and to reform its business environment—especially as wages are expected to rise in Asia. Even if real wages in China rise by only some 7 percent a year, which is modest given the country’s GDP growth, they are likely to double over the next decade. The rising cost of manufacturing there will translate into an opportunity for sub-Saharan Africa. East Asia broke into large-scale global manufacturing only around 1980. By that time, the gap in per capita incomes, and hence wages, between China and the OECD5 countries had widened exponentially. To a large extent, this huge advantage in labor costs allowed China to become competitive in manufacturing. As labor costs rise, the advantage is likely to shift toward sub-Saharan Africa.

A new risk reality is emerging in the aftermath of the financial crisis, with continued demand for commodities, climate change, and evolving demographics driving the way people do business around the world. Sub-Saharan Africa stands to play an important role in each of these major trends. Many industries, while nascent, are already emerging as success stories across the region. From footwear in Ethiopia to emerging tourism in Cape Verde and Rwanda, the menu of options for profitable investments is growing.

There are, of course, many challenges to realizing this great potential. As the world turns its attention to new markets for the next spring of growth, sub-Saharan Africa must address the constraints to its competitiveness. More opportunities will come up as much-needed improvements in business governance, infrastructure, logistics, and education are implemented; critical policy areas (including competition and access to finance and land) are reformed and modernized; and reforms and strategic investments in the underlying foundations that nourish businesses continue. Sub-Saharan Africa stands to be the new frontier for profitable investments.6