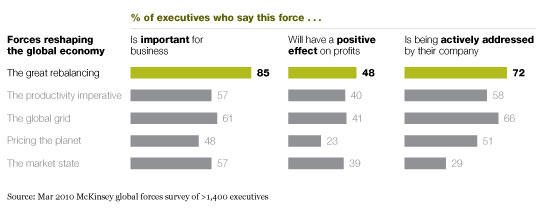

The vibrancy of emerging-market growth will not be the only major disruption reshaping the global economy in the next ten years, but it may prove the most profound. This decade will mark the tipping point in a fundamental long-term economic rebalancing that will likely leave traditional Western economies with a lower share of global GDP in 2050 than they had in 1700.

Two socioeconomic movements are under way.

-

Declining dependency ratios. Virtually all major emerging markets are undergoing demographic shifts that historically have unleashed dynamic economic change: simultaneous labor force growth and rapidly declining birthrates. Simply put, there will be more workers, with fewer mouths to feed, leaving more disposable income.

-

The largest urban migration in history. Each week, nearly one-and-a-half-million people move to cities, almost all in developing markets. The economic impact: dramatic gains in output per worker as people move off subsistence farms and into urban jobs. China and India are seeing labor productivity grow at more than five times the rate of most Western countries as traditionally agrarian economies become manufacturing and service powerhouses.

These same factors powered Western economic growth for the better part of two centuries. (And they should last well into the next decade—at least until China’s population, finally seeing the full effects of the one-child policy, begins to go gray.)

In the next decade, emerging-market economies will rapidly evolve from being peripheral players, largely reacting to events set in motion by wealthy Western nations, into powerful economic actors in their own right. They will shed their role as suppliers of low-cost goods and services—the world’s factory—to become large-scale providers of capital, talent, and innovation. (One hint of what’s to come: the number of BRIC1 companies on the Fortune 500 has more than doubled in the past four years alone.)

Nor is this trend just about China and India. To varying degrees, ASEAN,2 Latin American, and Eastern European nations, as well as portions of the Middle East and North Africa, are taking part in this economic renaissance. Even pockets of sub-Saharan Africa now demonstrate vigor after decades of stagnation.

For all companies—both established multinationals and emerging-market challengers—this great rebalancing will force major adjustments in strategic focus. No longer can established companies treat emerging markets as a sideshow. Emerging markets will increasingly become the locus of growth in consumption, production, and—most of all—innovation. More and more, global leadership will depend on winning in the emerging markets first.

Opportunity and adversity are the mothers of invention—emerging markets will be the world’s next fount of innovation

Consider that more than 70 million people are crossing the threshold to the middle class each year, virtually all in emerging economies. By the end of the decade, roughly 40 percent of the world’s population will have achieved middle-class status by global standards, up from less than 20 percent today. This means opportunity in consumer markets: P&G, for example, hopes to add a billion new customers to its ranks in the next decade, adding to the nearly four billion the company touches today. In recent quarterly earnings reports, nearly every global consumer products company—from Kraft to Nestlé—noted upticks in profits, driven primarily by unexpected gains in emerging markets.

The $2,200 Nano car, made by India’s Tata Motors, is just one among hundreds of new products that can turn traditional price and cost structures on their heads.

Seizing that opportunity won’t be easy. These new consumers come from a bewildering array of ethnic and cultural backgrounds. They have little loyalty to—or even knowledge of—established global brands. Their tastes and preferences will evolve just as rapidly, if not more so, than those of consumers in developed markets, and they will demand products with every bit as much quality. Yet, on average, they will wield just 15 percent of the spending power, in real dollars, of their developed-world counterparts.

Companies that can reduce cost structures to 20 or 30 percent of developed-world levels, or lower, will be in position to ride a swelling wave of unmet demand. While much has been made of the Nano, Tata’s $2,200 car, the truth is that hundreds of products now being developed promise to reinvent price and cost structures radically—from Hindustan Lever’s $43 water purifier, in use in more than three million Indian homes, to the Zero, a proxy ATM that costs less than $50 a month to operate (essentially a revamped cell phone with an attached fingerprint scanner, used by local merchants).

To tap the riches rising from these new markets, established organizations must reinvent business models. Hindustan Lever, for example, unable to find reliable distribution in large reaches of India, uses everything from bicycles to bullock carts to deliver products to market. When the Indian refrigerator manufacturer Godrej decided to release a refrigerator for the rural market, it worked with villagers to codesign a product that worked for their needs. The result: the ChotuKool, a $69 fridge that not only shattered price barriers but also included features that allow it to work in an environment where consumers cannot depend on their electricity to stay on.

Today’s unit share leaders will be tomorrow’s revenue winners—ignore them at your peril

Thanks to a low price structure, such innovations capture massive unit share long before they generate meaningful revenue share. This distinction matters. CEOs who miss it risk being overtaken by low-cost innovators that race up the value chain until they have a commanding lead.

Caterpillar, for example, is the world’s largest construction-equipment manufacturer. Its revenues are twice those of the next-largest player. No Chinese company makes the top ten by this measure, so China might appear to be a distant threat. But unit sales numbers tell a different story. Ranked by the number of vehicles sold, 9 of the industry’s 12 largest manufacturers of wheel loaders—the second-largest-selling piece of construction equipment—are Chinese. Nor do these players have an advantage only in their home market: Chinese manufacturers now supply a third of the wheel-loader volume in emerging markets outside China and are beginning to hit their stride in developed markets too. No wonder traditional industry leaders, including Cat, have raced to get a piece of the action, rushing to forge joint ventures with Chinese competitors.

Even luxury brands such as L’Occitane appeal to consumers in emerging markets—the French company’s fastest-growing segment. It is floating its upcoming IPO on the Hong Kong exchange rather than the Euronext.

Significantly, while emerging-market upstarts often gain market share by trading away margin to build position, that is not always the case. The best, forced to innovate by the harsh conditions of their home markets, are developing leaner business models that both boost low-cost demand and deliver enviable financial returns.

Consider Bharti Airtel, India’s leading wireless provider. In 2003, Bharti founder Sunil Mittal, struggling to hire telecommunications engineers and build out a network fast enough to keep pace with exploding demand for mobile services, made a controversial decision to outsource the construction and management of Bharti’s wireless network to Ericsson and Siemens. The result, a fundamentally new approach to managing a mobile-services company, allows Bharti to reap profit margins higher than most Western telecommunications companies do—despite average revenues per user just 10 to 15 percent of those of its developed-world counterparts.

The allure of emerging-market consumers touches even luxury companies. The privately held French beauty products company L’Occitane, for example, is floating its upcoming IPO not on the Euronext, in Paris, but rather on the exchange in Hong Kong. The reason: emerging-market consumers are the fastest-growing segment for this affordable luxury brand.

Don’t assume that emerging markets are just a cost play—technological innovation will be the next frontier

Last year marked the first ever when an emerging-market company—the Chinese telecom manufacturer Huawei—led the world in patent applications. No US company made the top ten. An imperfect measure? Perhaps, but it captures a deep underlying trend. Today, India supplies more technology workers than any other country, and China is on track to pass the United States as the home of the world’s largest R&D workforce. As more and more talent centers spring up across emerging markets and skills deepen, new innovation ecosystems will emerge. Already, more than 1,000 multinational companies operate R&D facilities in China, five times the level a decade ago.

In electronics, computing, and clean energy, among other fields, emerging-market companies increasingly define the future. Huawei, long dismissed as a perennially weak upstart to the likes of Cisco Systems or Ericsson, is now the world’s third-largest telecom-equipment manufacturer and builds some of the most sophisticated network equipment anywhere. It counts nearly every leading telecom operator as a customer.

Learn to manage multiple business models—or why the West still matters

For established Western multinationals, the biggest dilemma will be figuring out how to thrive while competing across highly different types of markets. Since both developed and emerging markets require innovation at breakneck speed, many companies may be tempted to underinvest in potential long-term revenue growth in new markets in order to pursue here-and-now profit gains in established ones. That’s understandable: while more than 50 percent of future global growth will occur in emerging markets—and in many industries much more than that—the lion’s share of profits so far remains in the OECD. But that’s shortsighted. Companies need to figure out how to win in both.

The mobile-phone handset market epitomizes the paradox: cutting-edge smartphones make up just 6 percent of global handset volumes, yet Apple, Research in Motion (RIM), and HTC now earn more than 50 percent of total industry profits. On the lower end, ultra-low-cost handsets from OEM manufacturers such as TCL and ZTE are capturing significant volume share in emerging markets. Traditional players such as Motorola, Nokia, and Samsung find themselves squeezed in the middle, fending off assaults on both top and bottom—largely from competitors that barely registered less than five years ago. Managing multiple business models is hard.

Blowback is real—so why not drive it yourself?

A few innovative companies are starting to get it right. GE, for example, has devised an electrocardiograph machine for the Indian market that can be sold profitably for $1,500, less than a fifth of the price of traditional ECG monitors in Europe and the United States. The new model has helped GE not only to extend a new level of health care to millions of Indians but also to figure out how to create a monitor it could sell for $2,500 in developed markets. Based on this experience and others like it, GE is now developing more than 25 percent of its new health care products in India—with explicit plans to deploy them both in emerging and advanced economies.

Shoppers in São Paulo, Brazil—just one country where investments by companies based in developed markets have spurred an “innovation blowback” in developing ones: the emergence of lower-priced, high-quality products that raise the stakes for global competition.

The prospect of this innovation wave unleashed by the great rebalancing should serve as a wake-up call to any CEO. Emerging markets are more than enormous growth opportunities; they are where tomorrow’s champions will hone their long-term competitiveness. Pursuing incremental product line extensions in developed markets, though profitable in the short run, will not suffice to build the critical muscle required. Innovation “blowback” is coming as lower-priced, high-quality products created for the mass markets of tomorrow move from the developing to the developed world. Buoyed by strengthening currencies and improved balance sheets, emerging-market challengers will move further up the value chain by acquiring more Western companies. Learning to win in low-cost, high-growth countries means winning not just there but everywhere.

The impact of global forces on business