It’s almost inevitable: to boost growth when a company reaches a certain size and maturity, executives will be tempted to diversify. In extreme cases—the United States during the 1960s and 1970s, for example—a corporation with a sharp focus on its core business can end up as a mix of strange bedfellows. One global oil enterprise famously acquired a computer business, another a retailer. And a major US utility once owned an insurance company.

Although a few talented people over time have proved capable of managing diverse business portfolios, today most executives and boards realize how difficult it is to add value to businesses that aren’t connected to each other in some way. As a result, unlikely pairings have largely disappeared. In the United States, for example, by the end of 2010 there were only 22 true conglomerates.1 Since then, 3 have announced that they too would split up.

Yet too many executives still believe that diversifying into unrelated industries reduces risks for investors or that diversified businesses can better allocate capital across businesses than the market does—without regard to the skills needed to achieve these goals. Because few have such skills, diversification instead often caps the upside potential for shareholders but doesn’t limit the downside risk. As managers contemplate moves to diversify, they would do well to remember that in practice, the best-performing conglomerates in the United States and in other developed markets do well not because they’re diversified but because they’re the best owners, even of businesses outside their core industries (see sidebar, “Conglomerates in emerging markets”).

Limited upside, unlimited downside

The argument that diversification benefits shareholders by reducing volatility was never compelling. The rise of low-cost mutual funds underlined this point, since that made it easy even for small investors to diversify on their own. At an aggregate level, conglomerates have underperformed more focused companies both in the real economy (growth and returns on capital) and in the stock market. From 2002 to 2010, for example, the revenues of conglomerates grew by 6.3 percent a year; those of focused companies grew by 9.2 percent. Even adjusted for size differences, focused companies grew faster. They also expanded their returns on capital by three percentage points, while the ROCs of conglomerates fell by one percentage point. Finally, median total returns to shareholders (TRS) were 7.5 percent for conglomerates and 11.8 percent for focused companies.

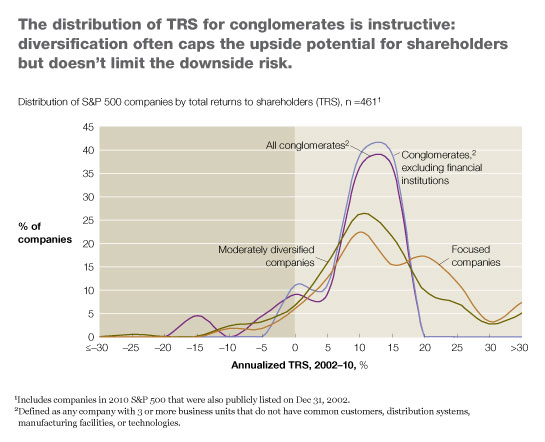

As usual, the median doesn’t tell the entire story: some conglomerates did outperform many focused companies. And while the median return from conglomerates is lower, the distribution’s shape tells an instructive story: the upside is chopped off, but not the downside (exhibit). Upside gains are limited because it’s unlikely that all of a diverse conglomerate’s businesses will outperform at the same time. The returns of units that do are dwarfed by underperformers and therefore probably won’t affect the entire conglomerate’s returns in a meaningful way. Moreover, conglomerates are usually made up of relatively mature businesses, well beyond the point where they would be likely to generate unexpected returns. But the downside isn’t limited, because the performance of the more mature businesses found in most conglomerates can fall a lot further than it can rise. Consider a simple mathematical example: if a business unit accounting for a third of a conglomerate’s value earns a 20 percent TRS while other units earn 10 percent, the weighted average will be about 14 percent. But if that unit’s TRS is negative 50 percent, the weighted average TRS will be dragged down to about 2 percent, even before other units are affected. In addition, the poor aggregate performance can affect the motivation of the entire company and how the company is perceived by customers, suppliers, and potential employees.

Prerequisites for creating value

What matters in a diversification strategy is whether managers have the skills to add value to businesses in unrelated industries—by allocating capital to competing investments, managing their portfolios, or cutting costs. Over the past 20 years, the TRS of the high and low performers among the 22 conglomerates remaining in 2010 clearly differed on exactly these points. While the number of companies is too small for statistical analysis, we did find three characteristics the high performers shared.

Disciplined (and sometimes contrarian) investors. High-performing conglomerates continually rebalance their portfolios by purchasing companies they believe are undervalued by the market— and whose performance they can improve. When Danaher identifies acquisition targets, for example, those companies must be good candidates for higher margins, using the company’s well-known Danaher Business System. By applying this strategy, over the past 20 years Danaher has consistently managed to increase the margins of its acquired companies. These include Gilbarco Veeder-Root, a leader in point-of-sale solutions, and Videojet Technologies, which manufactures coding and marking equipment and software. Both of those companies’ margins improved by more than 700 basis points after they were acquired.

Aggressive capital managers. Many large companies base a business’s capital allocation for a given year on its allocation the previous year or on the cash flow it generates. High-performing conglomerates, by contrast, aggressively manage capital allocation across units at the corporate level. All cash that exceeds what’s needed for operating requirements is transferred to the parent company, which decides how to allocate it across current and new business or investment opportunities, based on their potential for growth and returns on invested capital. Berkshire Hathaway’s business units, for example, are rationalized from a capital standpoint: excess capital is sent where it is most productive, and all investments pay for the capital they use.

Rigorous ‘lean’ corporate centers. High-performing conglomerates operate much as better private-equity firms do: with a lean corporate center that restricts its involvement in the management of business units to selecting leaders, allocating capital, vetting strategy, setting performance targets, and monitoring performance. Just as important, these firms do not create extensive corporate-wide processes or large shared-service centers. (You won’t find corporate-wide programs to reduce working capital, say, because that may not be a priority for all parts of the company.) Business units at Illinois Tool Works, for example, are primarily self-supporting, with broad authority to manage themselves as long as managers adhere to the company’s 80/20 (80 percent of a company’s revenue is derived from 20 percent of its customers) and innovation principles. The corporate center handles only taxes, auditing, investor relations, and some centralized HR functions. Berkshire Hathaway’s corporate center operates with no integration of cross-cutting functions.

Value-destroying failures litter the history of diversification strategies. Executives considering one should ask themselves, first and foremost, whether they have the skills to be the best owners of businesses outside their core industries.

Related Articles