Sharp jumps in the price of oil and gas caused by the US Gulf Coast hurricanes of 2005 delivered huge profits to ExxonMobil and other major oil companies, in some cases helping them report record quarterly earnings. But even beyond the oil patch many other companies, in a broad set of industries, also generated massive earnings. Indeed, a growing number of companies, such as Citigroup, General Electric, IBM, Microsoft, Toyota Motor, and Wal-Mart Stores, now earn around $10 billion or more annually.

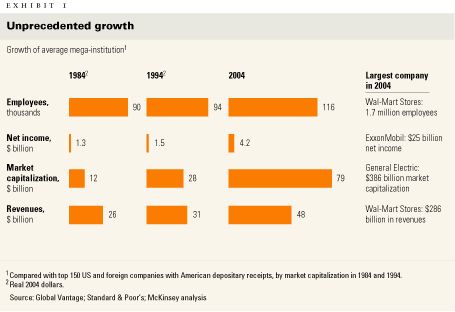

The emergence of such mega-institutions1 and the ways in which they are developing their extraordinary scale and scope represent a basic structural change in the landscape of business. Although the average mega-institution doubled its revenues from 1984 to 2004, by far the most striking increase has come in these companies' net income and market capitalization, which jumped three- and sixfold, respectively, during that period (Exhibit 1).2

In today's global marketplace, mega-institutions face few external limits on their size and profitability: for instance, Citigroup—the world's largest financial institution, with $250 billion in market value and nearly 300,000 employees—holds only 5 percent of the global financial-services market. Straightforward projections, based on the experience of the past 20 years, indicate that in 2015, 350 companies would be larger than the smallest company on the list of today's 150 biggest corporations. The largest of them would approach $700 billion in market capitalization and earn $40 billion or more a year.

Mega-institutions are developing extraordinary scale

The most successful of these companies are creating a new model of competitive advantage—a model that poses a profound management and planning challenge for corporate strategists. Historically, large companies such as General Motors and Unilever used their scale and scope advantages to obtain privileged access to tangible factors of production (such as capital and labor), relying on integrated value chains of production to overcome geographic and market barriers.

But today's most successful large companies have a more nuanced formula for success. They are exploiting their size and scope, as well as the large number of talented professionals they employ, to combine tangible and intangible assets across the enterprise. In this way, they create unique capabilities and value propositions that help them achieve a distinctive and durable competitive edge.

Three fundamental characteristics are at work. First, successful mega-institutions recognize an ever more direct link between their profitability and their large professional-talent pools—the engine for generating and deploying intangible assets. They also overcome the barriers of internal complexity that often accompany large scale and scope. Finally, these companies develop and mobilize unique intangibles, such as knowledge and relationships, to create value propositions that exceed the sum of their individual elements.

That three-part formula is already at work in the way companies such as Citigroup and Goldman Sachs have organized themselves internally to marshal their forces to serve large clients. It can also be seen in the ability of companies such as General Electric to parlay their expertise in manufacturing to build highly successful global finance, maintenance, and service businesses.

The evolution of the mega-institution

The development of today's largest corporations can be traced to a remarkable shift in the mix of the top 150 companies and in the nature of the workforce they employ. Consider a striking fact: financial-services and health care companies represented just 12 percent of the top 150 in 1984 but now make up 39 percent of that elite group. These two sectors employ relatively large numbers of professionals and managers, who create value primarily by generating and using knowledge through interactions with others rather than their own individual labor. What's more, the largest companies in other sectors (such as manufacturing) have also shifted their employment base significantly by utilizing a greater proportion of professionals and managers. GE, for example, had a workforce of 330,000 in 1984, when this group of employees accounted for some 25 percent of the total. By 2004, although GE's employment base actually had shrunk a little, the percentage of professionals and managers in the company's ranks had more than doubled. Meanwhile, net income per employee soared from $13,000 in 1984 to $54,000 in 2004 (in constant 2004 dollars).

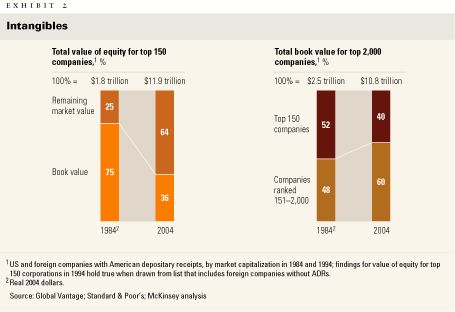

Tens of thousands of talented professionals work in mega-institutions—companies such as Citigroup, GE, and IBM each employ well over 100,000. These people create and exploit not only tangible assets such as capital but also intangible ones. To see the increased importance of intangible assets, consider the fact that book value accounted for only 36 percent of the market caps of the top 150 companies in 2004, as opposed to 75 percent in 1984. While this trend is relevant across many public companies, it is especially pronounced in mega-institutions. In fact, book value's share of the market caps of the top 150 companies has declined markedly relative to its share in the top 2,000, indicating that mega-institutions increased their physical capital more slowly than have other large companies (Exhibit 2).

Book value is shrinking for the top 150 companies

Increasing income with fewer employees

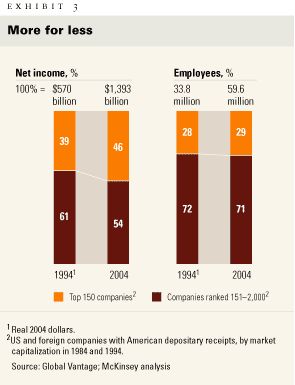

Today's mega-institutions also stand apart from companies that were their peers a decade or two ago in the way they have raised their profitability. On average, their economies of scale and scope have risen faster than the diseconomies associated with their increased complexity, or what economists call "the costs of excessive largeness." The mega-institutions' 2004 combined net income—nearly $650 billion—accounted for 46 percent of the combined net income of the top 2,000 corporations by market value, compared with 39 percent in 1994. But as the mega-institutions have increased their share of these companies' total net income, their share of the total workforce hasn't risen in proportion (Exhibit 3). To put the same point another way, the biggest companies boosted their average constant-dollar profit per employee from $21,000 in 1994 to $64,000 ten years later.

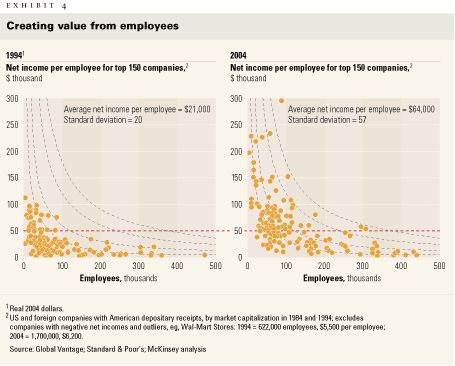

Averages don't tell the whole story. Within the top 150 companies, some earn much higher returns on capital and net income per employee than others. As recently as 1994, for example, only 25 companies in the top 150 netted more than $50,000 per employee (in 2004 dollars); by 2004, 79 did (Exhibit 4). By contrast, 41 companies among the top 150 in 2004 still earned less than $25,000 per employee. This increased variation didn't result from changes in industry mix or any specific metric. Indeed, such variations characterized nearly every industry represented in the list of the top 150 companies. A similar (though less pronounced) pattern of variation was also evident returns on invested capital.

Increasing returns on net income per employee

The evidence suggests that during the past decade, some mega-institutions developed strategies and organizational models, largely involving intangible assets, that help them to produce extraordinary profits and to exploit their economies of scale and scope more effectively. Such strategies and models now have a greater impact than the diseconomies of increased size. It's notable that these companies are capturing the excess returns rather than competing them away as consumer surplus. This development in turn suggests that the elite mega-institutions have created unique business models and intangible assets that competitors can't easily replicate.

Toward a new performance metric

This new breed of corporation faces a new set of strategy conundrums. The first is that it must have a way of measuring performance—one focused on the productivity of employees. Highly knowledge- and talent-intensive industries, such as advertising, consulting, and legal services, have long used performance metrics that revolve around people (profit or revenue per partner, for example). In a world of integrated global capital markets and very wide access to capital, talented employees have become the ultimate scarce resource, so profit per employee is a critical performance metric.3

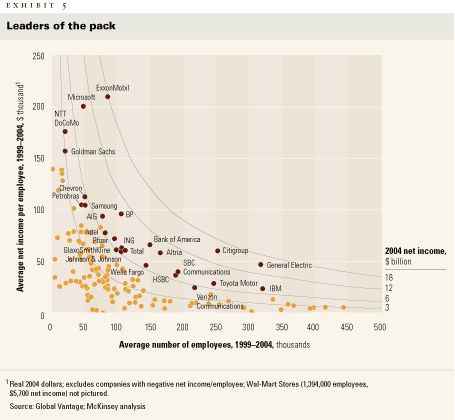

As value in the largest corporations becomes increasingly dependent on talented professionals who produce and share intangibles, managers should learn to view profit per employee as a fundamental metric.4 By this measure, Microsoft and ExxonMobil are two of the planet's top five companies (though the former employs only about 55,000 people, the latter about 90,000), for both earned an average of more than $200,000 in profit per employee each year from 1999 to 2004. Among the largest 150 companies, we have identified 25 that earn the highest profit per employee relative to others with similar employment levels (Exhibit 5). These 25 companies earn 41 percent and nearly 20 percent of the total profits of the top 150 and the top 2,000, respectively.

The leaders achieve higher levels of profit per employee

How did these 25 companies break away from the pack? While each has a different story, most of them found ways either to increase their profit per employee dramatically or to take on more employees at high levels of profit per employee. For example, several companies on this list (ExxonMobil, Microsoft, and Samsung) raised their profits in an extraordinary way without adding employees. Others (Citigroup, GE, and Toyota) raised their profit per employee significantly even while they increased the size of the workforce. Still others (HSBC and IBM) managed to keep their profitability per employee constant while expanding employment rapidly.

The challenge of complexity

Complexity remains a significant challenge for many mega-institutions: as employment levels rise, fewer and fewer companies earn high profits per employee. Only four companies in the world (Citigroup, GE, IBM, and Toyota) have averaged more than 200,000 employees and earned upward of $25,000 over the past five years for each of them. In other words, the larger and more complex the company, the harder it is to perform extremely well by this standard.

A large company's degree of complexity depends, first, on external factors, such as the difficulty or ease of reaching customers and of contracting with outside suppliers. It also hangs, in large part, on internal considerations, including the nature and organization of the work that employees perform. The unprecedented complexity of today's mega-institutions can overwhelm strategic initiatives and collaborative efforts; in fact, a majority of the executives polled in a recent McKinsey Quarterly survey5 said that their companies had become so complex over the past five years that seizing growth opportunities is now significantly harder. With management stressing the need to exploit the most important opportunities through internal collaboration across functions and products, the problem gets worse the larger a company grows (see sidebar, "Where complexity hurts").

Where complexity hurts

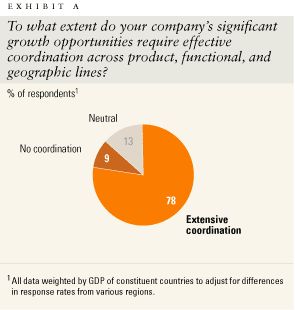

The bigger a corporation, the more complex it can be—which is a problem because the bigger a company gets, the more crucial collaboration among its executives becomes to its continued growth. In a 2005 McKinsey Global Survey of Business Executives, more than three-quarters of the respondents at companies with annual revenues of more than $20 million said that seizing growth opportunities calls for extensive coordination across product, functional, and geographic lines (Exhibit A). An even higher percentage (84 percent) of the respondents from companies with annual revenue of more than $30 billion stressed the need for widespread collaboration.

To what extent do your company's significant growth opportunities require effective coordination across product, functional, and geographic lines?

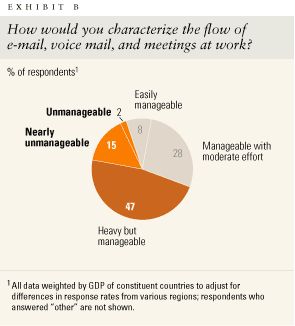

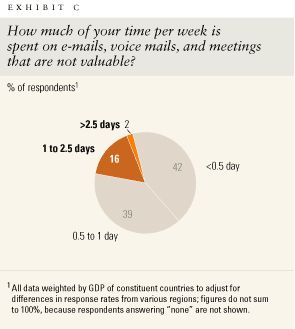

To facilitate collaboration, companies must understand how complexity hinders it. Communications overload is a big factor: many executives must deal with hard-to-manage volumes of voice mail, e-mail, and meetings (Exhibit B). What's more, nearly 40 percent say that they spend from half a day to a full day every week on communications without value (Exhibit C). For some, the situation is even worse.

How would you characterize the flow of e-mail, voice mail, and meetings at work?

How much of your time per week is spent on e-mails, voice mails, and meetings that are not valuable?

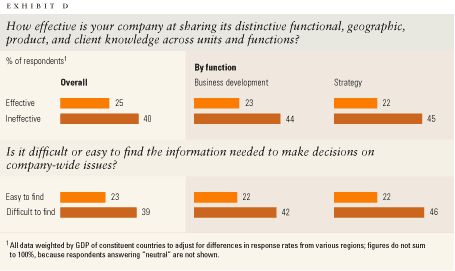

The other major problem of complexity is that it makes it hard for executives to find information—and people in growth-producing functions such as strategy and business development have the greatest difficulty (Exhibit D). Mega-institutions are coming to recognize the link between profitability and the productivity of their professionals. The most successful such companies will be those that overcome the barriers to communication and knowledge sharing.

How effective is your company at sharing its distinctive functional, geographic, product, and client knowledge across units and functions?

Successful mega-institutions reduce their complexity primarily in two ways. First, they have the discipline to divest businesses that don't benefit from large economies of scale or scope—that is, where they have little chance of leveraging tangible and intangible assets for competitive advantage—and continually explore opportunities to divest activities that are labor or capital intensive. Companies such as Citigroup, GE, and IBM thus balanced the large number of acquisitions they made over the past decade with numerous divestitures. In the past year, for instance, Citigroup sold its life insurance operations to MetLife for $11.5 billion so that it could focus on its higher-margin banking business. It also sold its transportation finance business to GE for $4.4 billion, since it couldn't generate enough cross-selling opportunities with its other product groups.

Second, successful mega-institutions use standards and protocols to reduce the unnecessary complexity that arises when employees work together across the enterprise. Common technology applications, consistent management processes, and standardized definitions of similar roles and responsibilities all promote effective, efficient coordination and decision making among professionals.

Consider the case of ExxonMobil, whose ability to execute core processes such as capital allocation and R&D consistently across the enterprise is among the key factors behind its success. For one thing, the company relies on a global functional organization, which instills a consistent approach to operations across geographies and makes it possible to develop technological innovations quickly and to adopt them throughout the world. It also maintains a particularly lean corporate center, with some 300 people working on critical business-shaping activities. (The company's new Dallas headquarters was designed with no more than 400 work spaces.)

GE deploys a central M&A team to structure and standardize the company's investment-scouting and -appraisal processes as well as a highly skilled "flying team," with legal and banking experts, to help the business units execute. Dell, which has far higher levels of net income per employee than any other computer maker, relies on the rigorous standardization of processes to offer tailored products and services while keeping complexity at a minimum. It also explicitly avoids segments (such as high-end servers and systems integration consulting services) that would require a significantly more complex business model to serve effectively.

New business models and value propositions

Besides dealing with the problems of complexity, successful mega-institutions are evolving their business models in two other critical ways. First, they are adapting the process of formulating strategy, by combining their tangible and intangible assets in unique ways to reveal new businesses and value propositions. Second, they are adopting far more integrated operating models to manage and deploy those assets and capabilities across the enterprise.

Discovering unique value propositions

The sheer scale and scope of the mega-institutions' intangible assets, combined effectively, can create unique value propositions. Often the best of them become apparent only through a process of staged discovery and experimentation.

Successful mega-institutions have therefore adapted their processes in order to facilitate the discovery of value propositions based on tangible and intangible assets that cross internal company boundaries. IBM's emerging-business-opportunity process, for example, stimulates and provides staged investments for ideas from customers, venture capitalists, and employees across organizational silos. Opportunities financed in this way now produce incremental revenues of $15 billion, including $2 billion from Linux consulting fees and $1.7 billion from digital-media businesses.

Another mega-institution—GE—built a financial-services business by acquiring business capabilities and "discovering" new knowledge over time. GE Capital originally worked with the GE units that make consumer products such as refrigerators and dishwashers. Eventually, it gained enough scale and expertise to offer finance services for GE's more sophisticated industrial products, including power plants and jet engines. Now financial services account for 46 percent of GE's revenue.

The discovery process shouldn't focus solely on developing new products or entering new markets; it should also include activities such as improving functional skills and core processes. ExxonMobil, for instance, invests 70 percent more money than the average of other large companies in the petroleum business to develop proprietary technologies that could raise its functional excellence in fields ranging from finance to exploration and production.

Managing and deploying intangible and tangible assets

Successful mega-institutions increasingly manage themselves as a single integrated entity instead of a collection of stand-alone businesses. In fact, these companies use much more integrated enterprise-wide operating models and go-to-market approaches than they did even a decade ago. The same forces that are creating larger, more integrated global markets help leading companies manage greater scale and scope at lower cost. Offshored, company-wide shared utilities, for instance, are taking over functions previously carried out by each individual business unit and pooling them in global service organizations. HSBC, one of the companies taking this approach, has more than 10,000 employees in eight "global operating centers of excellence" in Brazil, China, India, and Malaysia. They provide operational-support services to geographically led businesses and some specialized support, including business process services and IT application development, across the enterprise.6

Increasingly, companies are also creating shared utilities even for highly skilled knowledge work. Such "reservoirs" of intangibles can be tapped by all of a company's business units around the world. In addition to GE's traditional R&D center, in Niskayuna, New York, for instance, the company has established enterprise-wide R&D facilities in China, Germany, and India. (The latter employs 1,800 engineers and technologists, a quarter of whom hold PhDs.) People in these facilities undertake fundamental research for many GE divisions, often collaborating across countries on a single project, such as the development of a new 92-ton turbine.7

Meanwhile, winning financial mega-institutions such as Citigroup and Goldman Sachs are mastering relationship-management structures that coordinate sales, pricing, service delivery, and senior-client coverage across different product groups on a global scale. Citigroup, for example, developed a new relationship-management model that the investment- and corporate-banking divisions use to coordinate coverage of senior clients. Developing the new model took years, since it called for clear and consistent client-facing roles across units, extensive coordination by product- and client-development units, detailed information about relationship economics, and new incentives and responsibilities (to encourage collaboration). Such effective models for managing relationships give Citigroup and Goldman Sachs a real advantage because many of their best clients are mega-institutions (or emerging ones) that want a single point of contact and customized solutions encompassing a number of products in order to address specific problems.

To generate, share, and safeguard key intangibles effectively, leading mega-institutions often create new roles to integrate activities across organizational silos; Goldman Sachs, for instance, appointed a chief learning officer, and several other mega-institutions have influential chief risk officers. Historically, most such C-level positions were seen as pure staff support roles, but they are becoming more and more strategic, as they are directly tied to the creation of value; the quality of a company's risk-management practices, for instance, could be worth billions of dollars. In increasingly people-oriented businesses, a company's approach to talent and knowledge could have as great an impact on the creation of value as optimizing capital productivity does.

For mega-institutions, navigating a strategic landscape populated by other such companies will be one of the defining management challenges of the 21st century. With trillions of dollars of value at stake over the next decade, huge companies that unleash the potential of the many talented professionals they employ—by overcoming complexity and by discovering and mobilizing the distinctive capabilities of these employees across the enterprise—will stand to create value on a truly global scale.