Competitive advantage is the essential ingredient of any strategy. Yet for many companies, advantage is an elusive goal. The results of a recent McKinsey survey suggest one reason: just 53 percent of executives characterize their companies’ strategies as emphasizing the creation of relative advantage over competitors; the rest say their strategies are better described as matching industry best practices and delivering operational imperatives—in other words, just playing along.

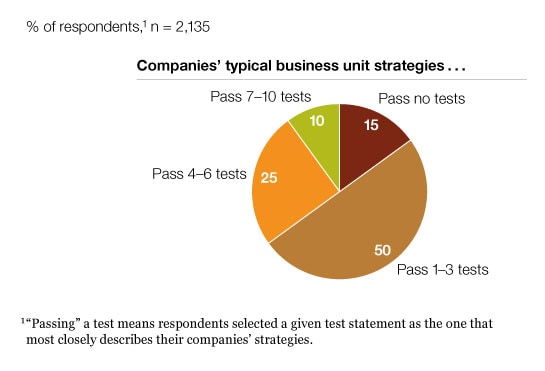

In this survey,1 executives around the world answered a series of questions that allowed us to test how fully their companies’ business unit strategies pass ten tests that we believe, based on years of work with clients and academic research, make for a good strategy.2 The first—whether the strategy will beat the market by creating competitive advantage—is comprehensive. The remaining nine tests disaggregate the picture of a market-beating strategy, assessing how the strategy positions the company in the market, what level of insight the strategy rests on, and what the implementation plan involves. Nearly two-thirds of respondents indicate that their companies pass three or fewer of the ten tests, meaning that our description of the test closely describes a particular element of their strategies (Exhibit 1). And only 2 percent of respondents say their companies pass nine or all ten tests.

Passing the 10 tests

While it’s certainly possible for a strategy to succeed at a company that fails all or even most of the tests, the results underscore that companies can do much more to pressure-test their strategies. The results also suggest some ways that companies can prioritize improvements in their approach to strategy based on the tests respondents say contribute most to financial performance and are most frequently used in their sectors.

Playing to win—or just playing along?

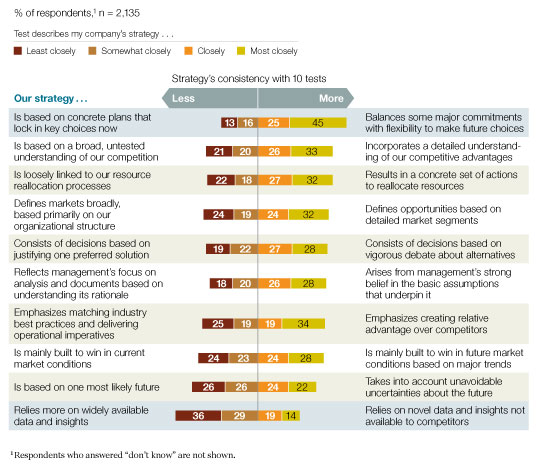

One striking result of this survey is the room for improvement in using these principles that, in our experience, generate competitive advantage—the average share of executives who say their companies passed an individual test is just 57 percent.

When we look at the specific tests, two stand out—one because it is widely used, the other because it is often neglected (Exhibit 2). Seventy percent of executives report that their strategies provide a mix of commitments and flexibility, as opposed to locking in key choices immediately. This suggests that these companies are comfortable building their strategies as a portfolio of different strategic actions: big bets aimed at gaining competitive advantage, no-regret moves that will pay off whatever happens, and real options that involve relatively low costs now but can be elevated to a higher level of commitment as conditions change.

What companies do best

In contrast, only 33 percent say their companies’ strategies rest on novel data and insights not available to competitors, rather than widely available data. One likely explanation: the widespread availability of information and adoption of sophisticated strategy frameworks creates an impression that “everyone knows what we know and is probably analyzing the data in the same ways we are.” Yet if strategists question their ability to see something that no one else does, they are less likely reach for the powerful insight that is most likely to differentiate them from competitors.

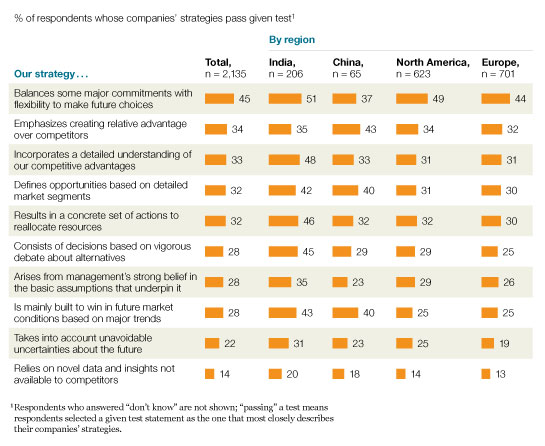

Some notable regional differences show up in the responses. Executives in India, for example, indicate that their companies pass more tests more frequently than do executives in China, Europe, or North America (Exhibit 3). China-based executives rate their companies’ strategies higher than their peers in the other three regions on the fundamental test of emphasizing relative advantage, but they trail on balancing commitments and flexibility to make choices in the future.

Regional variation

Taking the tests to the bottom line

Whether executives say their companies pass a given test is likely, of course, to be partly related to whether they think it matters. And indeed, there is a rough correlation between passing a test and executives saying a test is instrumental to financial performance. For example, when asked which three tests have the most positive effect on financial performance, more executives select flexibility to make choices in the future than any other test. And as Exhibit 2 shows, this is the test the most companies pass. Conversely, novel insight is the test rated least important to financial performance and passed least frequently.

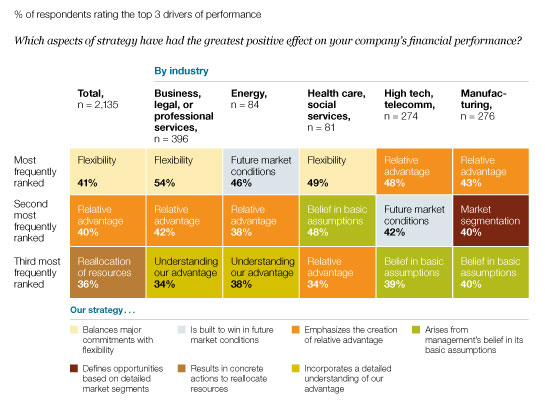

When executives assess the tests’ impact on financial performance, some interesting differences arise among industry sectors (Exhibit 4). Executives in the energy industry, for example, are likelier than all others to say a focus on trends has a good effect on their financial performance, with 46 percent saying so. Executives in the health care and high-tech sectors, meanwhile, stress the importance of management having a strong belief in the strategy’s underlying assumptions; nearly half of them cite that test.

Testing performance

The influence of process

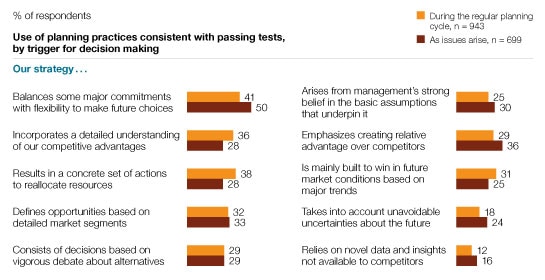

An intriguing finding is the possibility that the choice of tests and the forces that drive planning may be related. Besides gathering data on which tests respondents say their companies pass, we also asked what triggers companies to make decisions about strategy. Forty-four percent of respondents say their companies use a regular planning cycle; these executives are likelier to say their companies understand competitive advantage, incorporate trends, and allocate resources effectively (Exhibit 5). In contrast, 35 percent of respondents say their companies make decisions as they arise; they are more likely to say their companies manage uncertainty well, include flexibility to make choices down the road, and create relative advantage over competitors.3

The financial crisis of 2008 and the recession that followed revealed weaknesses in many strategies and forced many companies to confront choices and trade-offs they put off in boom years. Not surprisingly, a majority of respondents to this survey—56 percent—report that their companies are making strategic decisions more frequently than before. This increased speed may make it difficult for some companies to analyze each decision in detail. However, a shift toward shorter planning cycles only increases the need to focus on the timeless aspects of strategy that can drive competitive advantage, and to pressure-test strategies against them quickly.

When decisions are made

Looking ahead

-

More than half of the executives in this survey indicate their companies don’t pass even five of these ten tests. Although which tests matter most will vary from company to company, the results and our experience suggest that the companies that pay more attention to more of these tests early on will have a better chance of developing market-beating strategies later.

-

The finding that executives in different industries see different tests as affecting financial performance indicates that one size does not fit all. Undertaking a thorough review of the strengths and weaknesses of your company’s past strategies through these ten lenses, particularly the ones most relevant to your industry, will help you determine which are most relevant to your company’s situation.

-

In our experience, far too many companies don’t develop their strategies with a process that could include the assessments these tests offer. Companies that overtly include these tests in their strategic development process have a good chance of besting competitors that don’t.

Related Articles

Have you tested your strategy lately?