M&A activity slowed in 2011 as uncertainty surrounding the European sovereign-debt crisis continued to vex the global economy. The growth that characterized the first seven months of the year came to an abrupt halt in August as the crisis heightened, accompanied by a sharp 17 percent drop in the S&P 500 and a surge in volatility.1 For the year, companies around the world announced 7,700 deals, valued at $2.7 trillion—a meager 3 percent increase from 2010.

Not surprisingly, activity among companies headquartered in Europe was most affected, falling by 26 percent between the first and second halves of 2011—compared with only an 18 and 9 percent drop among companies in the Americas and Asia, respectively. Overall, acquisitions by European companies constituted just 31 percent of M&A by volume, the lowest share for the region since 1998. Cross-border activity was also affected as Asian and US companies actively sought out deals in Europe. Although total activity for the year remained steady at the 2010 level, the amount of M&A into Europe by non-European acquirers increased to $220 billion because of a few large transactions and an increase in midsize and small acquisitions.

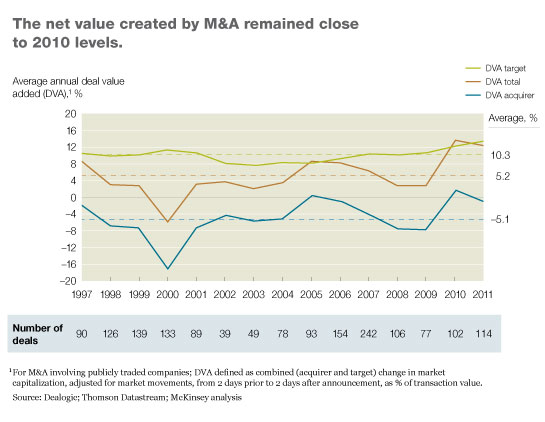

Despite the crisis and slowdown in activity, investors remain sanguine about deals. Our analyses showed that in 2011 they created almost as much value, measured as share price movements before and after the announcement,2 as they did in 2010—the highest in our 15 years of tracking. The net value, measured as deal value added (DVA), dropped to 12 percent, from 13 percent in 2010, but remained considerably higher than the 15-year average of around 5 percent (Exhibit 1).

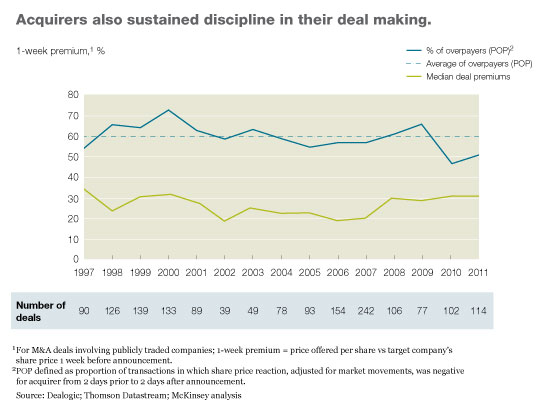

Acquirers also remained disciplined at capturing this value for their shareholders: the proportion of deals followed by a decline in the acquirer’s share price—the percentage of overpayers—remained low at 51 percent, significantly better than the historic average of 60 percent (Exhibit 2). This implies that investors expected that half of all deals in 2011 would destroy value for the acquirer’s shareholders, even as continued high premiums suggested that shareholders of the companies sold weren’t getting shortchanged.